Rio Tinto (RIO) stands as one of the world’s largest mining conglomerates, specializing in the extraction of key materials that fuel global industry and the energy transition. While it remains heavily anchored in its massive iron ore operations in the Pilbara, the company is actively executing a long-term strategy to diversify its portfolio into future-facing commodities such as copper and lithium. This deliberate diversification is the cornerstone of its resilience.

Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

The first half of 2025 demonstrated a “very resilient” financial performance despite significant external headwinds. Lower iron ore prices and the impact of early-season cyclones presented challenges. However, the growing contributions from the aluminium and copper businesses, coupled with improving operational performance across the portfolio, helped offset these external factors.

Underlying this resilience is a disciplined focus on operational improvement and best-in-class project execution. Rio Tinto is successfully ramping up key projects, such as the Oyu Tolgoi copper mine, and accelerating major developments, such as the Simandou iron ore project. These large-scale projects lay the groundwork for strong mid-term production growth, solidifying the company’s position in the global energy transition materials market.

Quickly value any stock with TIKR’s powerful new Valuation Model (It’s free!) >>>

Financial Story

Rio Tinto delivered Underlying EBITDA of $11.5 billion and operating cash flow of $6.9 billion for the first half of 2025. While both metrics saw slight year-over-year declines (5% and 2%, respectively), this resilience is highlighted by the 13% decline in iron ore prices during the same period. The strong performance of other segments effectively mitigated the primary headwind in its largest market.

This strong operational performance resulted in a cash conversion rate of 60%, an improvement over the prior half-year. However, an increase in capital expenditure to $4.7 billion (up 18% YoY) to fund major projects led to a 31% reduction in Free Cash Flow (FCF), settling at $2.0 billion. This movement demonstrates the company’s prioritization of disciplined investment in future growth over short-term cash maximization.

| Metric | H1 2025 Outcome | Comparison to H1 2024 | Notes |

| Underlying EBITDA | $11.5B | (5%) Decrease | Resilient despite a 13% decline in iron ore prices. |

| Operating Cash Flow | $6.9B | (2%) Decrease | Strong cash conversion of 60%. |

| Underlying Earnings | $4.8B | (16%) Decrease | Impacted by a higher tax rate and depreciation. |

| Free Cash Flow (FCF) | $2.0B | (31%) Decrease | Due to an 18% increase in capital expenditure. |

| Interim Dividend Payout | 50% | Unchanged | Consistent with long-term policy. |

The interim dividend reflects this balanced capital allocation strategy, with a $2.4 billion ordinary dividend declared, maintaining the established 50% payout ratio on underlying earnings. The company’s net debt rose significantly to $14.6 billion following the major acquisition of Arcadium Lithium, but the balance sheet remains strong, anchored by consistent cash generation and high-grade credit ratings.

Look up Rio Tinto’s full financial results & estimates (It’s free) >>>

Broader Market Context

The global mining market is shaped by two powerful forces: cyclical commodity prices and the irreversible demand created by the energy transition. While iron ore prices declined 13% year over year, copper and aluminum prices rose in the first half of 2025, underscoring the market’s complexity.

The long-term outlook is fundamentally bullish for materials like copper and lithium. Global demand for lithium carbonate equivalent (LCE) is growing significantly, driven primarily by Electric Vehicles (EVs) and Battery Energy Storage Systems (BESS). To meet this surging demand, the industry will require substantial greenfield investments, and new production will need to be incentivized, despite current low spot prices. Rio Tinto’s strategic pivots position it perfectly to capture this long-term demand.

1. Strategic Pivot to Future-Facing Commodities

Rio Tinto is aggressively executing its strategy to shift its portfolio towards energy transition materials. This was most evident with the early completion of the Arcadium Lithium acquisition in March 2025, a move that immediately established the company as a major lithium producer with one of the world’s largest resource bases. This adds greater diversification and financial resilience, allowing non-iron ore segments to pick up the slack during commodity price troughs.

The company didn’t stop there, signing agreements to form joint ventures with Chile’s Codelco and ENAMI for high-grade lithium projects in the Salar de Maricunga and Salares Altoandinos. These strategic partnerships secure future growth options and solidify the company’s push into the top tier of energy transition materials suppliers.

2. Accelerating High-Impact Projects

Rio Tinto is demonstrating best-in-class project execution, a key factor in future earnings predictability. The massive Simandou iron ore project in Guinea, one of Africa’s largest integrated mining and infrastructure investments, has accelerated its first shipment to around November 2025. This progress on a complex, multi-jurisdictional project underscores a commitment to delivery.

In the Copper segment, the flagship Oyu Tolgoi underground mine in Mongolia continued its successful ramp-up, achieving a 54% YoY increase in production in the first half. This project is on track to average ~500 ktpa of copper from 2028-2036, significantly boosting the company’s output of this critical metal.

Value stocks like Rio Tinto in less than 60 seconds with TIKR (It’s free) >>>

3. Operational Excellence and Cost Discipline

Even as it invests heavily in growth, Rio Tinto maintains a tight focus on operational efficiency through its Safe Production System (SPS), which has been rolled out across 36 sites. This initiative is driving tangible results, such as a record half-year bauxite production, as the Amrun operation consistently outperformed expectations.

The successful ramp-up of Oyu Tolgoi and higher grades at Escondida helped drive Copper’s unit costs down significantly, leading to an updated, lower guidance range for Copper C1 net unit costs. Furthermore, the company is focused on being Impeccable in ESG, including securing a new Power Purchase Agreement (PPA) for Boyne Aluminium and advancing the NeoSmelt steel decarbonization project.

The TIKR Takeaway

The TIKR platform provides the necessary framework to understand Rio Tinto’s complex narrative. The stock performance reflects a challenging year, with the price return over the last 11 months showing a significant decline of over 33%, demonstrating confidence in the forward strategy. The platform helps contextualize the slight drop in underlying EBITDA by highlighting the massive negative impact of iron ore price declines, which were nearly offset by underlying volume growth and diversification gains.

Using TIKR’s tools, investors can quickly dissect the underlying EBITDA by product group and observe the notable 50% and 69% EBITDA uplifts in the aluminium and copper segments, respectively. This visualization makes the diversification story immediate and clear.

For an investor building a forward-looking model, tracking RIO’s disciplined $10-$11 billion mid-term capital guidance against their accelerated project timelines for Simandou and Oyu Tolgoi offers unparalleled clarity into long-term value creation.

Should You Buy, Sell, or Hold Rio Tinto’s Stock in 2025?

Rio Tinto is currently in a phase of strategic transformation and heavy investment, aggressively positioning itself to dominate the next commodity super-cycle driven by the energy transition. The company’s fundamentals are sound, demonstrating impressive resilience despite pricing pressure in its main segment.

Those focused solely on traditional metrics, such as short-term free cash flow, may want to wait for the major projects to transition from capital-intensive development to high-margin production. However, investors with a long-term view who recognize the best-in-class execution on large, valuable, future-facing projects and the continued commitment to shareholder returns may find the current moment presents an encouraging opportunity.

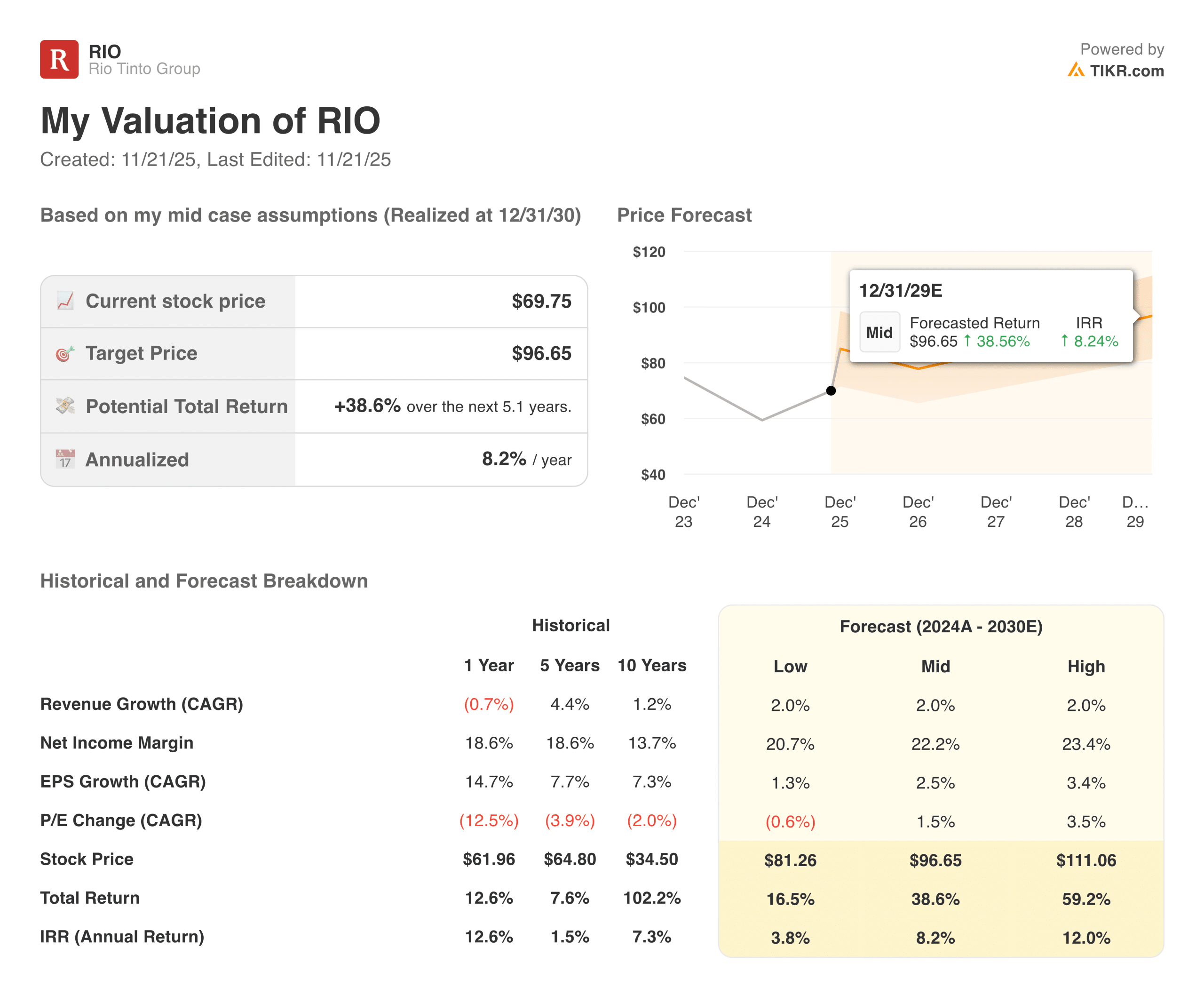

How Much Upside Does Rio Tinto Stock Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!