Agilent Technologies (A) has been showing gradual recovery through 2025 as demand across pharma, diagnostics, and industrial markets begins to stabilize. Shares trade near $151/share, supported by consistent margins and recurring consumables revenue that helps keep earnings steady even during softer spending conditions.

Recently, Agilent reported improving order trends in its biopharma and diagnostics segments and continued expanding its LC and mass spectrometry lineup with faster, higher throughput instruments designed to increase lab productivity. These developments signal that Agilent is still investing in innovation and positioning itself for a demand recovery as customer budgets improve.

This article explores where Wall Street analysts think Agilent could trade by 2027. We reviewed consensus targets and TIKR valuation models to outline the stock’s potential path. These figures reflect analyst expectations and are not TIKR’s own predictions.

Find out what a stock’s really worth in under 60 seconds with TIKR’s new Valuation Model (It’s free) >>>

Analyst Price Targets Suggest Upside Is Already Priced In

Agilent trades near $151/share today, and the latest average analyst price target is about $152/share, which indicates essentially 0% upside. Since the consensus sits almost exactly at today’s price, investors should expect the stock to remain stable unless growth trends improve meaningfully.

Street Targets (11/21/25):

- High estimate: $170/share

- Low estimate: $130/share

- Median target: $151/share

- Ratings: 8 Buys, 2 Outperforms, 8 Holds

The tight spread between the high and low estimates shows that analysts largely agree on Agilent’s steady outlook. This suggests the market already reflects both the strengths and the challenges in the company’s current trajectory, which limits the potential for near term upside.

Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

Agilent: Growth Outlook and Valuation

Agilent’s fundamentals appear stable, supported by steady demand across major end markets and a strong mix of recurring consumables revenue. Growth is moderate but reliable, which helps maintain consistent earnings momentum.

- Revenue is projected to grow 6% through 2027

- Operating margins are expected to hold near 26.7%

- Shares trade around 22x forward earnings

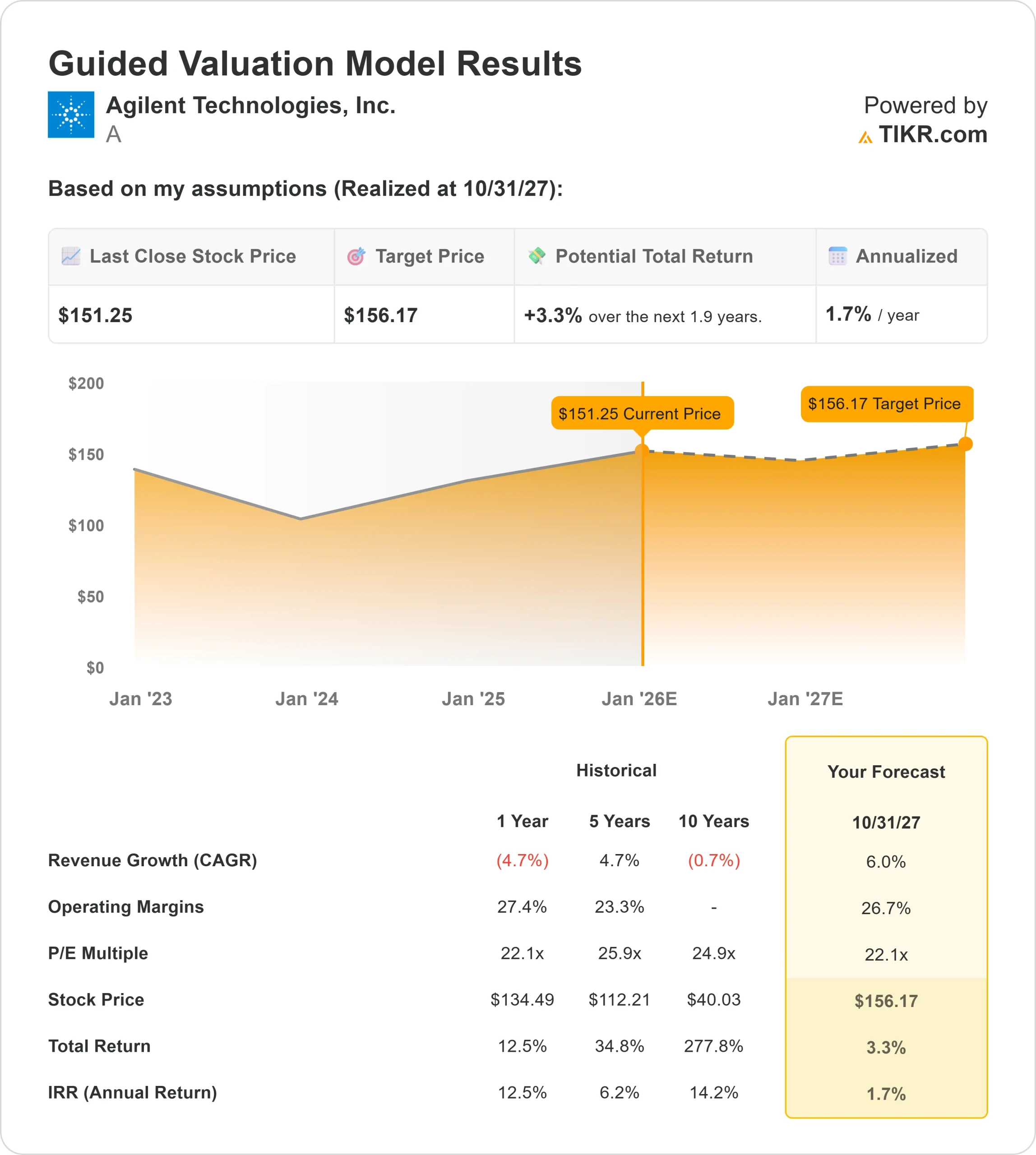

- Based on analysts’ average estimates, TIKR’s Guided Valuation Model using a 22x forward P E suggests about $156/share by 2027

- That implies roughly 3% total upside, or about 1.7% annualized returns

These numbers indicate slow but steady compounding. For investors, this valuation reflects a mature, high quality operator where expectations should remain measured unless revenue growth accelerates.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

What’s Driving the Optimism?

Agilent continues to benefit from a business mix that generates recurring revenue and supports stable margins. Its position in analytical instruments gives it durable exposure to long term growth areas such as pharmaceuticals, biotech, and diagnostics.

The company’s ongoing focus on product innovation and workflow efficiency helps deepen customer relationships and maintain competitive positioning. For investors, these strengths suggest Agilent is well equipped to sustain dependable earnings and protect its quality premium.

Bear Case: Growth Limits and Valuation Pressure

The main concern for Agilent is its moderate growth profile. While the company remains profitable and stable, revenue expansion has not shown meaningful acceleration, and competitive intensity remains elevated in several product categories.

If demand recovery stays uneven, the current valuation may act as a ceiling rather than a catalyst for higher returns. For investors, the risk is that Agilent continues to trade within a narrow range until clearer signs of stronger growth emerge.

Outlook for 2027: What Could Agilent Be Worth?

Based on analysts’ average estimates, TIKR’s Guided Valuation Model using a 22x forward P E suggests Agilent could trade near $156/share by 2027, which represents about 3% total upside, or roughly 1.7% annualized returns over the next 1.9 years.

While this outlook points to stability, it does not signal a major rerating unless growth improves beyond current expectations. For investors, Agilent looks most attractive as a steady compounder with predictable earnings rather than a high upside opportunity.

AI Compounders With Massive Upside That Wall Street Is Overlooking

Everyone wants to cash in on AI. But while the crowd chases the obvious names benefiting from AI like NVIDIA, AMD, or Taiwan Semiconductor, the real opportunity may lie on the AI application layer where a handful of compounders are quietly embedding AI into products people already use every day.

TIKR just released a new free report on 5 undervalued compounders that analysts believe could deliver years of outperformance as AI adoption accelerates.

Inside the report, you’ll find:

- Businesses already turning AI into revenue and earnings growth

- Stocks trading below fair value despite strong analyst forecasts

- Unique picks most investors haven’t even considered

If you want to catch the next wave of AI winners, this report is a must-read.

Find out what your favorite stocks are really worth (Free with TIKR) >>>