West Pharmaceutical Services (NYSE: WST) trades near $271/share after a volatile stretch. Growth has softened, margins have normalized, and the company continues to adjust to a slower post pandemic environment for pharmaceutical components. Even so, WST remains a high quality operator with strong returns and one of the cleanest balance sheets in the medical supplies industry.

Recently, WST has shown early signs of stabilization. Management highlighted improving demand for higher value components and a healthier product mix that supports stronger margins over time. Biologics related volumes, which had been a drag through 2024, are also beginning to recover. These developments suggest the business is regaining momentum in areas that matter most for long term earnings.

This article explores where Wall Street analysts believe WST could trade by 2027. We reviewed consensus targets and valuation models to outline the stock’s expected path. These figures reflect analyst expectations and are not TIKR’s own predictions.

Find out what a stock’s really worth in under 60 seconds with TIKR’s new Valuation Model (It’s free) >>>

Analyst Price Targets Suggest Meaningful Upside

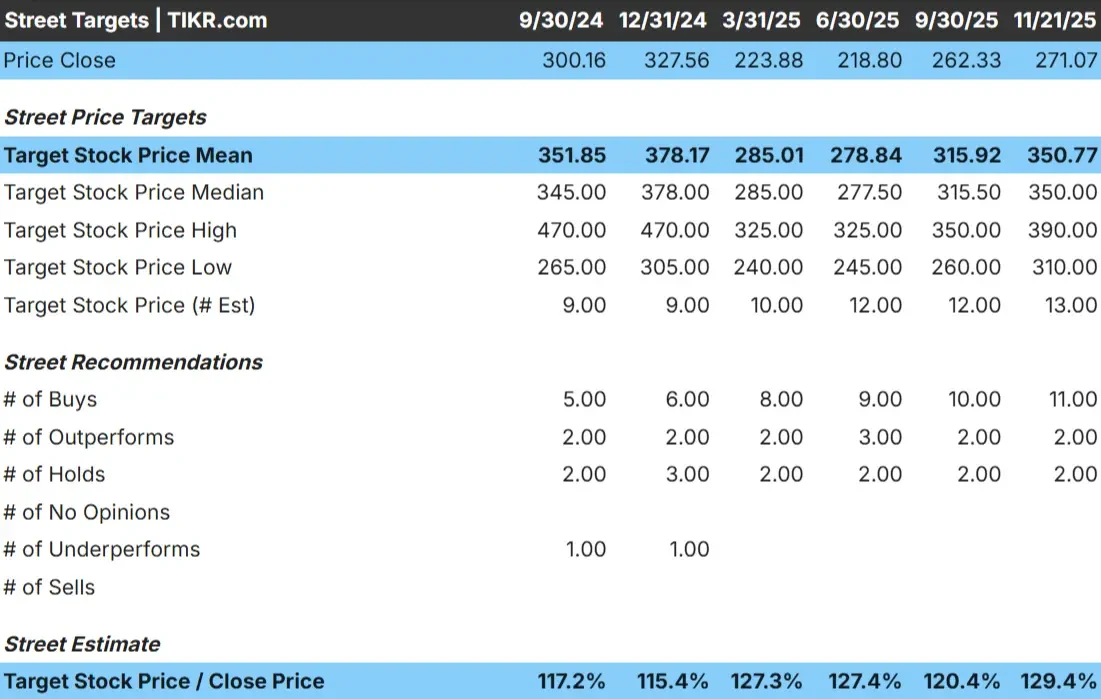

WST trades near $271/share today. The latest average analyst price target is $351/share, which implies about 30% upside, placing the stock in the meaningful upside category.

Here is the full target range:

- High estimate: $390/share

- Low estimate: $310/share

- Median target: $350/share

- Ratings: 11 Buys, 2 Outperforms, 2 Holds

The target range is relatively narrow, which shows analysts have a stable view of WST’s long term fundamentals. For investors, this reflects confidence that the business can steadily recover margins and sustain demand for its higher value components as pharmaceutical markets normalize.

Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

WST Growth Outlook and Valuation

The company’s long term fundamentals appear stable heading into 2027. Analysts expect WST to grow at a steady pace supported by durable demand for its containment and delivery components.

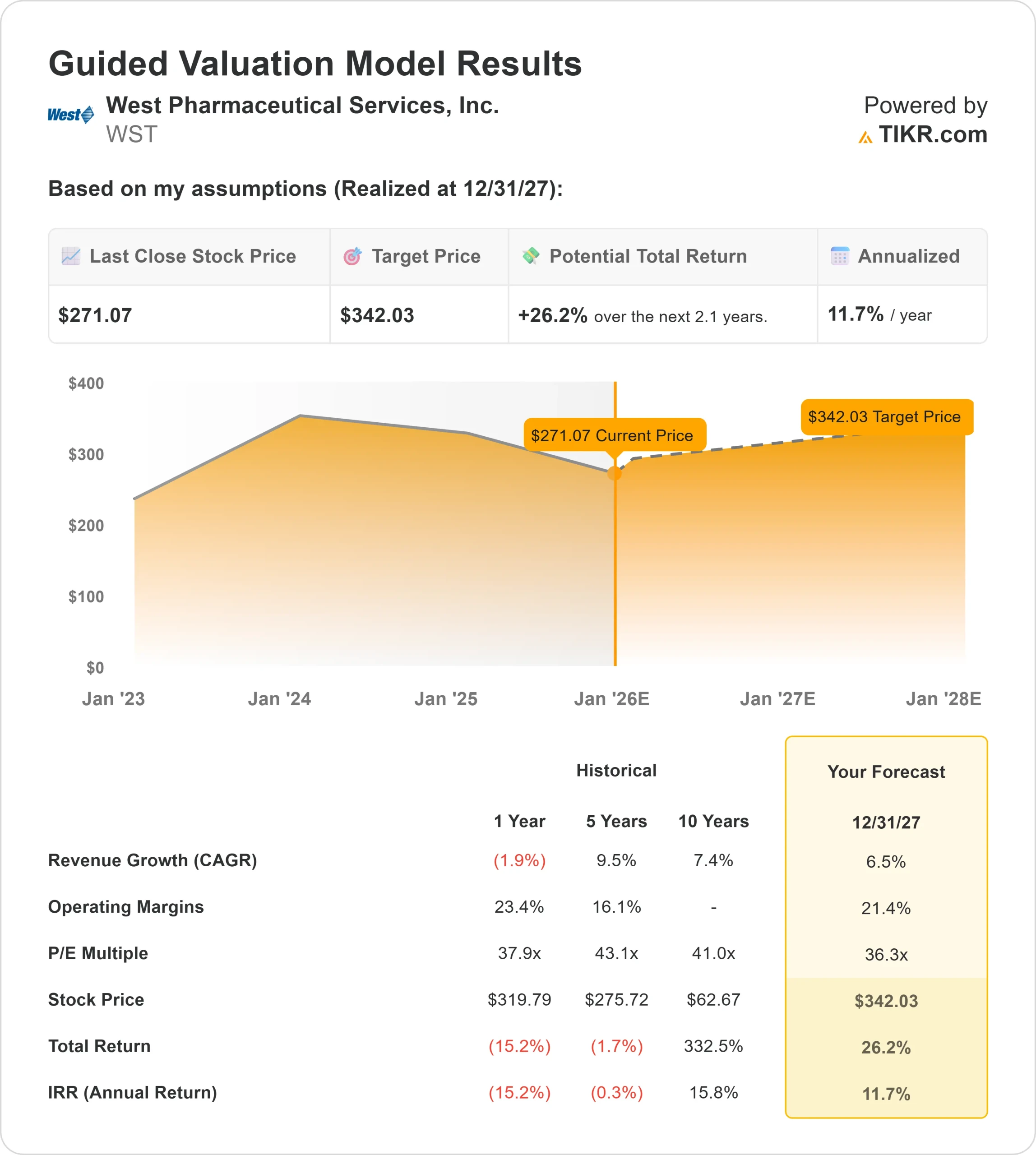

- Revenue is projected to grow 6.5%

- Operating margins are expected to hold near 21.4%

- Shares trade around 36.3x forward earnings

- Based on analysts average estimates, TIKR’s Guided Valuation Model using a 36.3x forward P E suggests about $342/share by 2027

- That implies roughly 26% upside, or about 12% annualized returns

These numbers suggest WST can compound steadily, although not at the pace seen during its strongest years. The valuation is elevated relative to mid single digit growth, which means upside depends on stable margins and continued strength in higher value components.

For investors, WST looks more like a dependable long term compounder than a fast growth story. The company’s premium pricing power, mission critical products, and high customer stickiness support a consistent earnings profile that can deliver solid returns over time.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

What’s Driving the Optimism?

WST plays a central role in the injectable drug supply chain, which gives its business long term stability. Demand is tied to pharmaceutical production trends rather than broader consumer cycles, allowing the company to operate with resilience even during economic uncertainty.

Management has also pointed to improving mix trends and better alignment with customer needs, especially in premium product categories where WST has stronger pricing power. The company maintains a net cash balance sheet, providing flexibility to invest in capacity and strategic improvements. For investors, these strengths support a gradual rebuild in earnings momentum.

Bear Case: Valuation and Slower End Markets

Despite its strengths, WST’s valuation remains elevated. Shares trade near 36x forward earnings, which is high given mid single digit growth expectations. This creates sensitivity to any slowdown in demand or margin softness.

WST also faces near term challenges across its end markets. Biotech funding cycles remain uneven, and pharmaceutical customers continue to manage inventory cautiously after the pandemic surge. Competitive pressure in elastomer components is also slowly increasing. For investors, the concern is that WST may not deliver enough acceleration to justify its premium valuation if growth remains below historical levels.

Outlook for 2027: What Could WST Be Worth?

Based on analysts average estimates, TIKR’s Guided Valuation Model using a 36.3x forward P E suggests WST could trade near $342/share by 2027. This represents about 26% total upside, or roughly 12% annualized returns.

While this is a solid return profile, it already assumes a steady recovery in demand and stable margins. To generate stronger upside, WST would need a more meaningful rebound in biologics activity or faster adoption of higher value components. Without those catalysts, investors should expect consistent but measured returns that reflect WST’s status as a high quality, slow and steady compounder.

For investors, WST remains a reliable long term business. The company’s competitive advantages are strong, but the path to outsized gains depends on management delivering above the expectations currently embedded in analyst forecasts.

AI Compounders With Massive Upside That Wall Street Is Overlooking

Everyone wants to cash in on AI. But while the crowd chases the obvious names benefiting from AI like NVIDIA, AMD, or Taiwan Semiconductor, the real opportunity may lie on the AI application layer where a handful of compounders are quietly embedding AI into products people already use every day.

TIKR just released a new free report on 5 undervalued compounders that analysts believe could deliver years of outperformance as AI adoption accelerates.

Inside the report, you’ll find:

- Businesses already turning AI into revenue and earnings growth

- Stocks trading below fair value despite strong analyst forecasts

- Unique picks most investors haven’t even considered

If you want to catch the next wave of AI winners, this report is a must-read.

Find out what your favorite stocks are really worth (Free with TIKR) >>>