Energy Transfer LP (NYSE: ET) has been trading near the lower end of its range at $17/share, weighed down by soft EPS trends, elevated leverage and a cautious backdrop across the midstream sector. Even with these challenges, the company continues to generate steady cash flow from its core natural gas and NGL network, which remains a critical part of U.S. energy infrastructure.

Recently, Energy Transfer completed its acquisition of Crestwood Equity Partners, adding more gathering and processing assets in the Williston and Delaware Basins. Management has also highlighted improving volume trends in its NGL segment, which has continued to be one of the strongest drivers of the business. These developments indicate that ET is positioning itself for stable long term performance despite near term uncertainty.

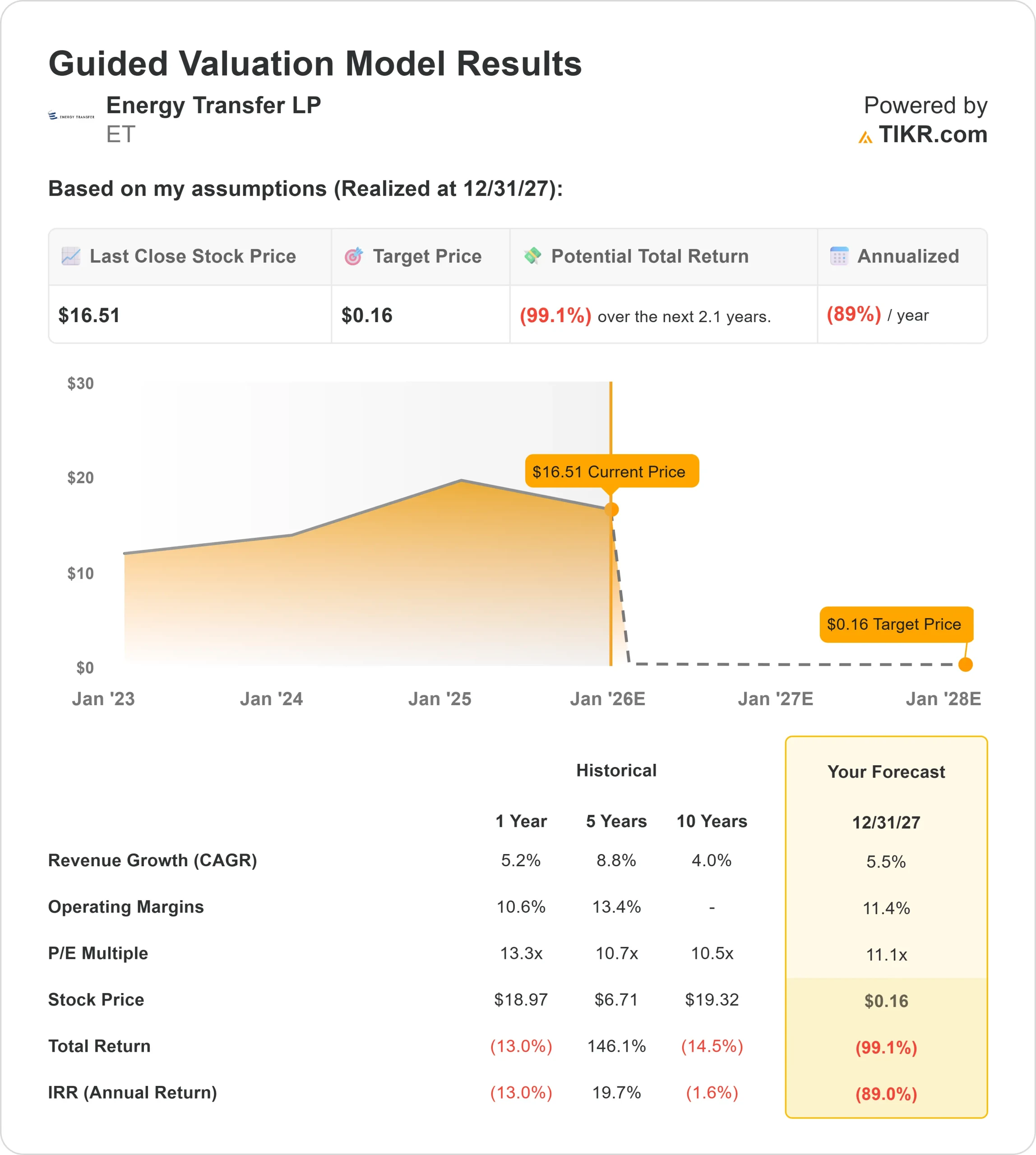

This article outlines where analysts expect the stock to trade by 2027 and how the valuation model interprets ET’s earnings profile. These figures reflect current analyst expectations and are not TIKR’s own predictions.

Find out what a stock’s really worth in under 60 seconds with TIKR’s new Valuation Model (It’s free) >>>

Analyst Price Targets Suggest Meaningful Upside

ET trades near $17/share, and analysts expect the stock to move toward $22/share, which represents about 30% upside from current levels.

Street breakdown:

- High estimate: $25/share

- Low estimate: $17/share

- Median target: $22/share

- Ratings: 12 Buys, 5 Outperforms, 2 Holds

The target range is fairly tight, which shows that analysts see room for gains but still expect a steady, income-driven profile rather than a major breakout. For investors, this points to meaningful upside supported by stable cash flow and predictable distributions, with most of the return driven by ET’s dependable operating base rather than aggressive growth.

Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

ET: Growth Outlook and Valuation

ET’s fundamentals appear steady, though the valuation model paints a very different picture under its specific assumptions.

- Revenue growth forecast: 5.5%

- Operating margin forecast: 11.4%

- Forward P E applied: 11.1x

- Based on analysts’ average estimates, TIKR’s Guided Valuation Model suggests a fair value of $0/share by 2027

- Implied total return: (99%)

- Implied annualized return: (89%)

These results look extreme because the model applies a traditional earnings multiple to a business where earnings do not reflect true economic performance. ET’s reported EPS tends to run much lower than its cash flow, which causes standard P E based valuation models to produce overly harsh outcomes.

For investors, the model should be viewed as a sensitivity test rather than a prediction. ET is best evaluated using cash flow stability, distribution coverage and long term volume trends, which provide a more accurate picture of its actual financial profile.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

What’s Driving the Optimism?

Analysts remain encouraged by improving operational trends across ET’s core systems. The Crestwood assets strengthen ET’s footprint in key producing regions, and improving NGL throughput continues to support margin stability. Management has also focused on enhancing utilization, improving efficiency and maintaining disciplined contract structures.

For investors, these factors suggest that the company has multiple levers to protect cash flow and sustain its distribution, even if overall growth remains moderate.

Bear Case: Leverage and Earnings Sensitivity

ET still carries leverage above what many investors prefer, which limits flexibility and can weigh on valuation. The company’s earnings profile is more volatile than its cash flow, which is why traditional valuation models tend to show severe downside during periods of low reported EPS.

Competition in key basins also remains steady, creating ongoing pricing and volume pressures. For investors, the risk is that ET’s cash flow may not grow quickly enough to meaningfully reduce leverage, which could cap the stock’s ability to re-rate higher over time.

Outlook for 2027: What Could ET Be Worth?

Based on analysts’ average estimates, TIKR’s Guided Valuation Model suggests $0/share under its current inputs. Analysts themselves expect ET to trade near $22/share, which implies approximately 30% upside from today’s $17/share price.

This expected upside is modest and already assumes stable operations, consistent volume trends and dependable cash generation. To unlock stronger returns, ET would need to deliver faster EBITDA growth, integrate Crestwood effectively and make measurable progress reducing leverage. Without these improvements, the distribution will continue to be the dominant driver of returns.

For investors, ET remains a stable income oriented holding with potential for slow and measured appreciation. The long term return outlook ultimately depends on the company’s ability to convert operational momentum into sustained financial gains.

AI Compounders With Massive Upside That Wall Street Is Overlooking

Everyone wants to cash in on AI. But while the crowd chases the obvious names benefiting from AI like NVIDIA, AMD, or Taiwan Semiconductor, the real opportunity may lie on the AI application layer where a handful of compounders are quietly embedding AI into products people already use every day.

TIKR just released a new free report on 5 undervalued compounders that analysts believe could deliver years of outperformance as AI adoption accelerates.

Inside the report, you’ll find:

- Businesses already turning AI into revenue and earnings growth

- Stocks trading below fair value despite strong analyst forecasts

- Unique picks most investors haven’t even considered

If you want to catch the next wave of AI winners, this report is a must-read.

Find out what your favorite stocks are really worth (Free with TIKR) >>>