Kinder Morgan, Inc. (NYSE: KMI) has traded steadily in recent months, sitting near $27/share as natural gas demand and pipeline volumes remain stable. The stock has held up well despite slower growth across the midstream industry, which speaks to its reputation as one of the most dependable pipeline operators in North America.

Recent trends have also been constructive. Revenue expectations are improving, and Kinder Morgan continues to show strong profitability supported by long-term, fee-based contracts. These factors indicate that the company remains well positioned even in a softer environment for commodity-linked businesses.

This article outlines where Wall Street analysts believe Kinder Morgan could trade by 2027. We combined consensus analyst targets with TIKR’s Guided Valuation Model to illustrate the stock’s potential return path. These figures reflect analyst expectations and are not TIKR’s own predictions.

Find out what a stock’s really worth in under 60 seconds with TIKR’s new Valuation Model (It’s free) >>>

Analyst Price Targets Suggest Modest Upside

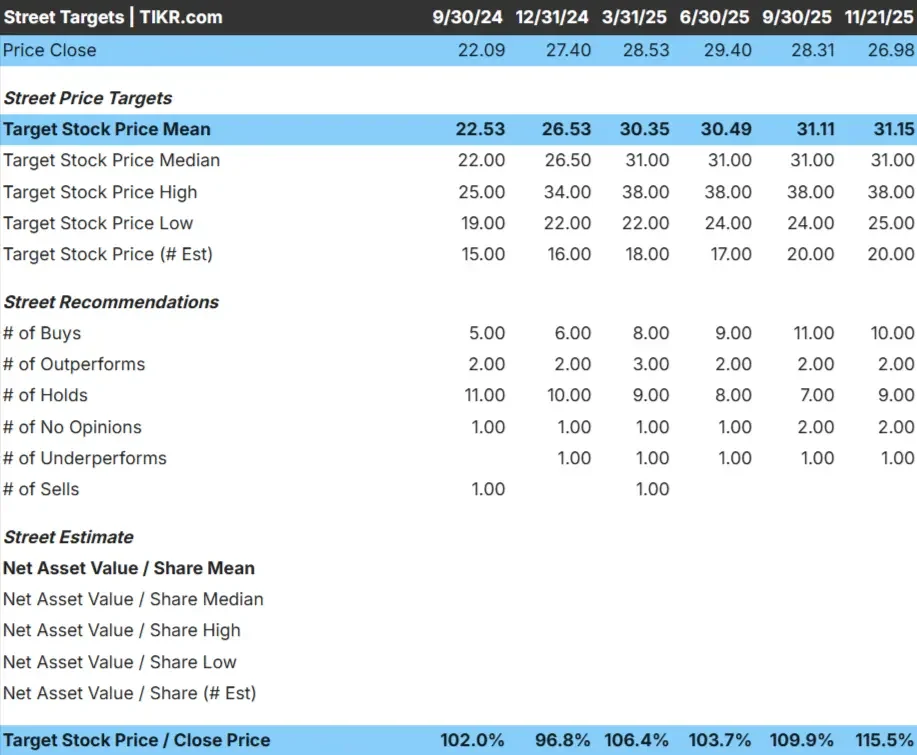

KMI trades near $27/share, and the latest average analyst target is $31/share, pointing to modest upside based on current Street estimates.

Key numbers from the 11/21/25 analyst grid:

- High estimate: $38/share

- Low estimate: $25/share

- Median target: $31/share

- Ratings: 10 Buys, 2 Outperforms, 9 Holds, 1 Underperform

This setup implies about 15% upside, which fits the modest category. Analysts expect gradual appreciation supported by stable earnings rather than a major move higher.

For investors, This reflects a stock that rewards patience rather than speed. KMI is a low-volatility, income-friendly operator that fits well in portfolios focused on consistency and steady returns.

Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

KMI: Growth Outlook and Valuation

The company’s fundamentals appear steady and supported by predictable revenue and solid profitability:

- Revenue is forecast to grow about 7% through 2027

- Operating margins are expected to remain near 28%

- Shares trade at roughly 18x forward earnings, which is reasonable for a mature pipeline operator

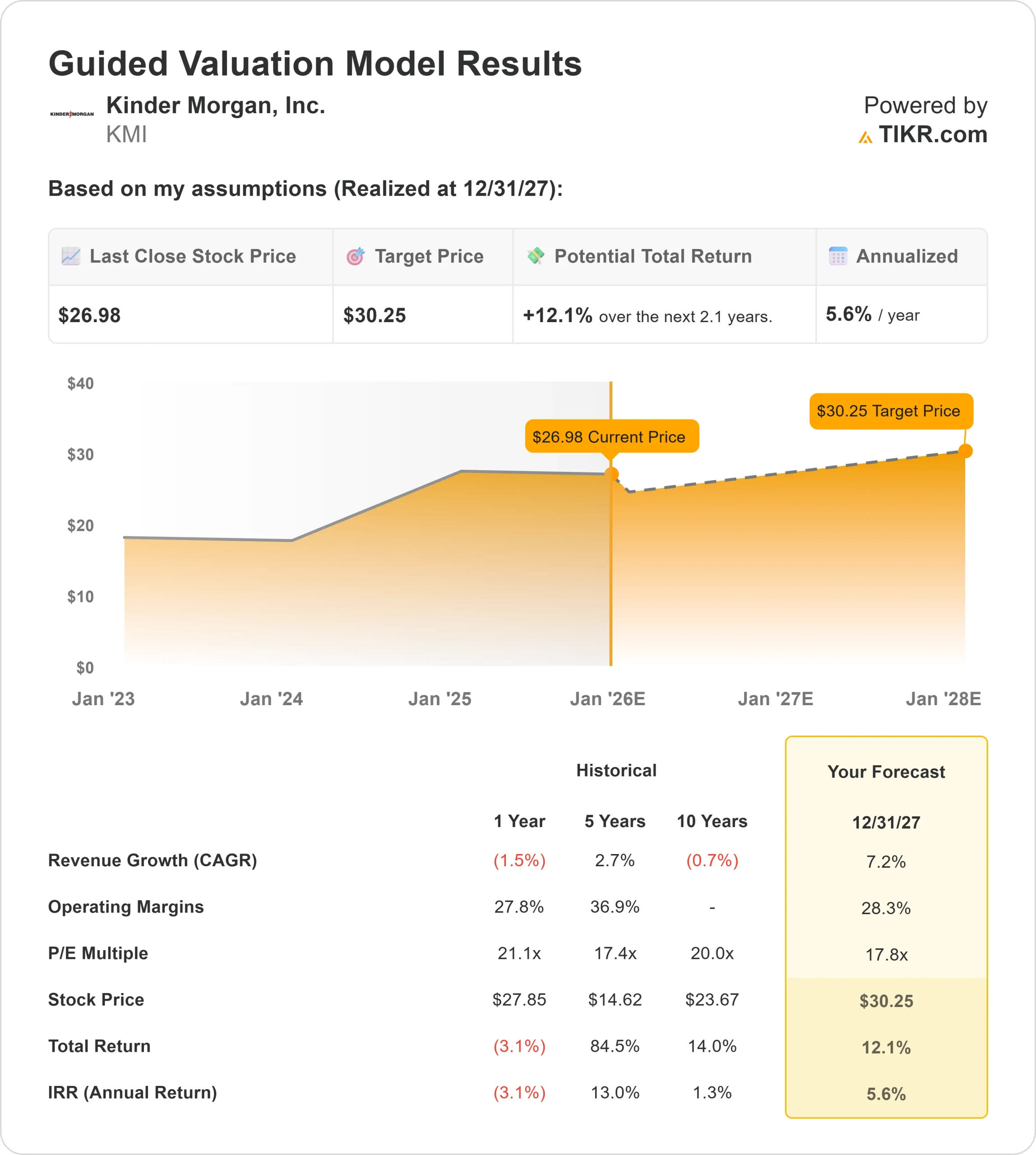

- Based on analysts’ average estimates, TIKR’s Guided Valuation Model using an 18x forward P E suggests about $30/share by 12/31/27

- That implies roughly 12% total upside, or about 6% annualized returns

These inputs point to gradual, steady compounding rather than rapid acceleration. The model reflects a business that relies on long-term contracts and fee-based revenue to deliver consistent earnings.

For investors, Kinder Morgan looks more like a stable, income-oriented compounder than a high-growth story. The return profile is built on visibility and reliability, with gains likely driven by predictable cash flows rather than valuation expansion.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

What’s Driving the Optimism?

Kinder Morgan’s business model is built on long-term, fee-based contracts that reduce exposure to commodity swings and create a stable revenue foundation. Its large natural gas pipeline network provides scale advantages, dependable volumes, and strong customer retention. These qualities support a consistent earnings profile and lower volatility.

For investors, This is the core reason optimism remains intact. KMI does not require rapid growth to generate steady returns. Its entrenched infrastructure footprint and essential role in U.S. energy logistics allow the company to deliver predictability even when the broader energy market is uneven.

Bear Case: Limited Growth and Valuation Cap

Despite its strengths, Kinder Morgan’s long-term growth trajectory is inherently limited. Pipeline expansion is a slow and highly regulated process, and the company’s high payout ratio restricts how much capital can be reinvested in new large-scale projects. This naturally caps how fast earnings and valuation can grow.

For investors, the bear case centers on capped upside rather than meaningful downside risk. If throughput growth stays modest and no major new projects materialize, KMI may continue to trade within a narrow band, delivering stable but unspectacular total returns.

Outlook for 2027: What Could KMI Be Worth?

Based on analysts’ average estimates, TIKR’s Guided Valuation Model using an 18x forward P E indicates that KMI could trade near $30/share by 12/31/27. This represents about 12% total upside, or approximately 6% annualized returns.

This forecast reflects a business built for gradual compounding. The stock’s return profile is shaped by steady earnings, predictable cash flows, and low volatility. To achieve stronger upside, Kinder Morgan would need higher throughput growth or new infrastructure projects that materially expand its earnings base.

For investors, Kinder Morgan remains a reliable choice for stability and income. While upside is capped, the consistency of the business makes it a solid fit for conservative investors who prioritize dependable returns over aggressive growth.

AI Compounders With Massive Upside That Wall Street Is Overlooking

Everyone wants to cash in on AI. But while the crowd chases the obvious names benefiting from AI like NVIDIA, AMD, or Taiwan Semiconductor, the real opportunity may lie on the AI application layer where a handful of compounders are quietly embedding AI into products people already use every day.

TIKR just released a new free report on 5 undervalued compounders that analysts believe could deliver years of outperformance as AI adoption accelerates.

Inside the report, you’ll find:

- Businesses already turning AI into revenue and earnings growth

- Stocks trading below fair value despite strong analyst forecasts

- Unique picks most investors haven’t even considered

If you want to catch the next wave of AI winners, this report is a must-read.

Find out what your favorite stocks are really worth (Free with TIKR) >>>