Key Stats for WMB Stock

- 6-Month Performance: 27%

- 52-Week Range: $52 to $73

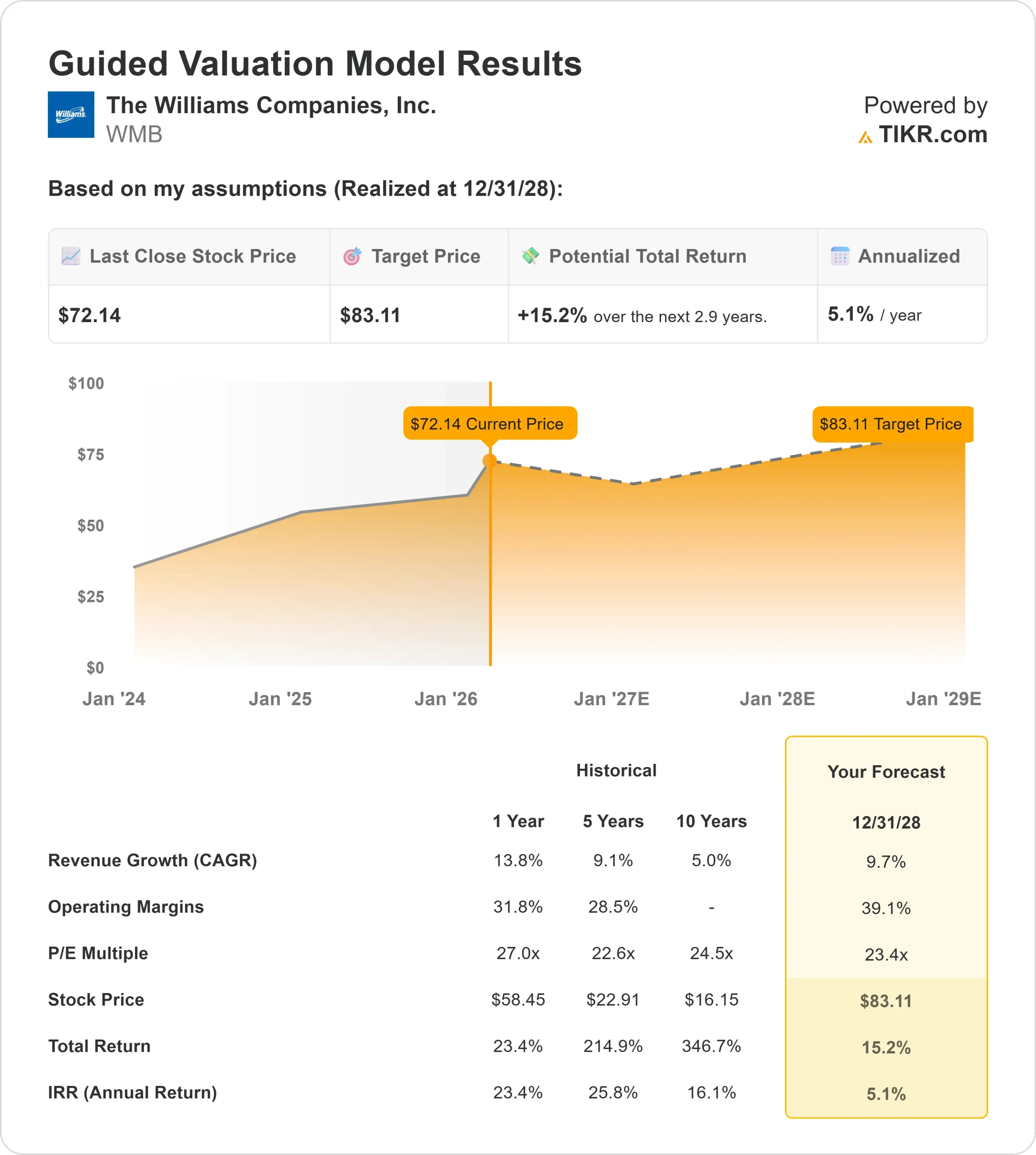

- Valuation Model Target Price: $83

- Implied Upside: 15%

Value your favorite stocks like The Williams Companies with 5 years of analysts’ forecasts using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

The Williams Companies stock shares have risen about 27% over the past six months, recently trading near $72 per share and approaching their 52-week high around $73. The steady advance reflects sustained institutional buying rather than a short-term spike.

The stock moved higher because Williams delivered record 2025 results and raised its long-term growth outlook, improving visibility into future earnings.

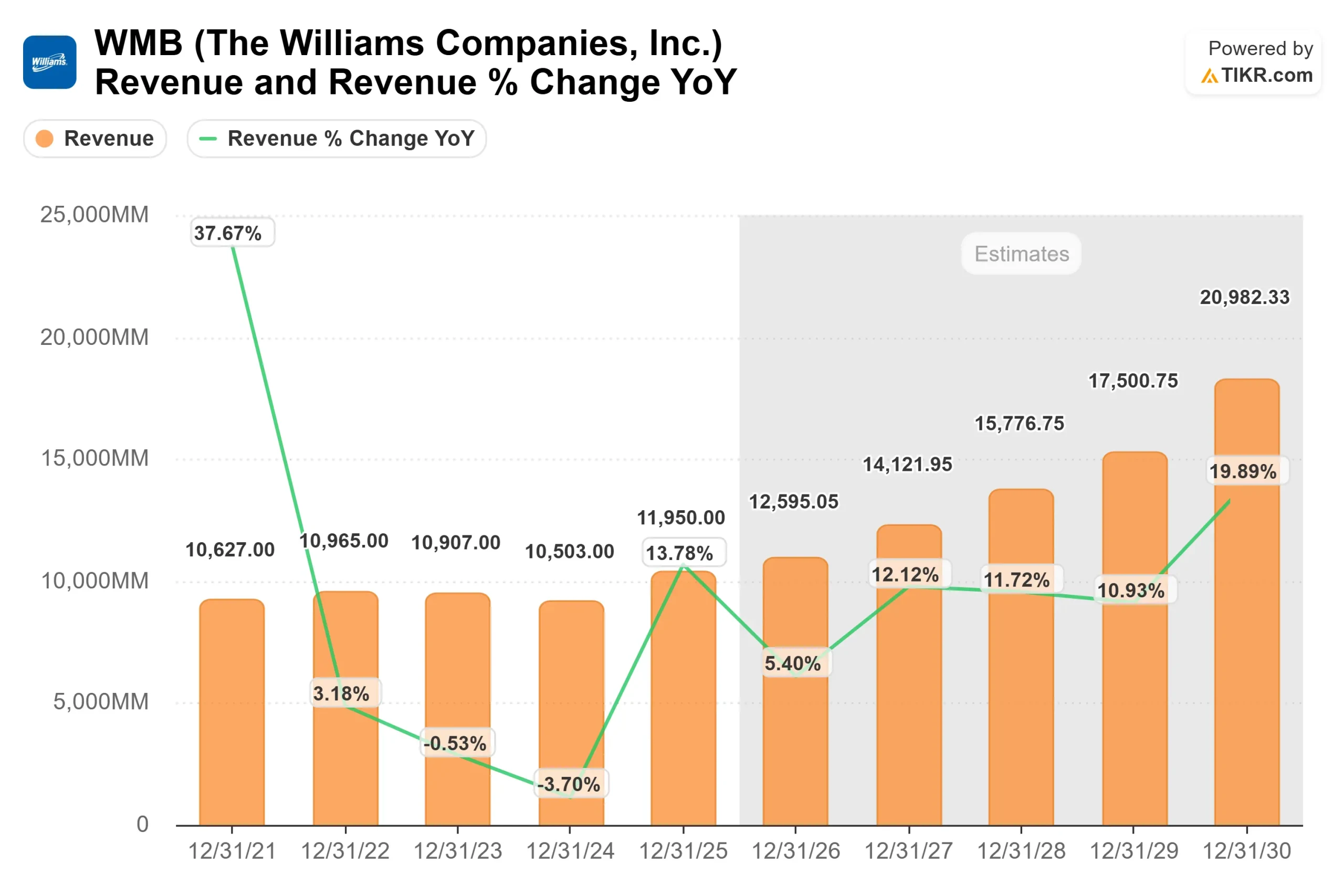

The company reported adjusted EBITDA of $7.75 billion for 2025, up 9% year over year and marking its 13th consecutive year of EBITDA growth.

Management also guided for $8.2 billion in 2026 adjusted EBITDA and introduced a new long-term target of at least 10% annual adjusted EBITDA growth through 2030, signaling confidence that contracted transmission and power projects will drive continued expansion.

At its recent Analyst Day, Williams detailed approximately $7.3 billion committed to its first four power innovation projects, which are expected to generate about $1.4 billion in annual EBITDA by 2029.

The company also has 13 transmission projects in execution that are projected to add roughly 7.1 billion cubic feet per day of new capacity by 2030.

CEO Chad Zamarin said the company is “excited to announce today our new growth target for the next 5 years of 10% compound annual growth in adjusted EBITDA from 2025 through 2030,” reinforcing confidence in the backlog.

Analyst and institutional updates further supported the rally. Stifel Nicolaus raised its price target to $78 from $69 and maintained a Buy rating.

Institutional ownership remains elevated at approximately 86%, with firms such as HighTower Advisors, Fifth Third Bancorp, Assetmark, and others increasing positions, even as select investors trimmed exposure.

The combination of record earnings, forward growth guidance, and strong ownership trends helped drive the six-month advance.

See analysts’ growth forecasts and price targets for The Williams Companies (It’s free) >>>

Is WMB Undervalued?

Under valuation assumptions, the stock is modeled using:

- Revenue Growth (CAGR): 9.7%

- Operating Margins: 39.1%

- Exit P/E Multiple: 23x

Revenue is projected to increase from approximately $12,595 million in 2026 to about $20,982 million by 2030, reflecting rising natural gas demand, incremental pipeline expansions, and the ramp-up of contracted power innovation projects already under construction.

Importantly, much of this expansion is supported by long-term take-or-pay contracts. Management expects more than 60% of EBITDA to come from long-term contracted revenue streams by 2030, reducing commodity exposure and strengthening earnings visibility.

Operating margins near 39% assume continued leverage from large-scale infrastructure already in place.

As major transmission and power projects enter service between 2026 and 2028, incremental EBITDA should flow through a largely fixed-cost base, supporting margin durability without requiring proportional increases in capital spending.

For 2026 specifically, investors will be watching execution on Southeast Supply Enhancement, progress on the Socrates power platform, and whether adjusted EBITDA tracks toward the $8.2 billion guidance.

Maintaining leverage within the 3.5x to 4x target range while funding growth will also remain a key focus.

Based on these inputs, the model estimates a target price of approximately $83 per share, implying about 15% total upside from current levels.

Because implied upside exceeds 6%, Williams screens as modestly undervalued under your framework.

However, with shares already up 27% in six months, future returns are likely to depend more on execution and earnings delivery than on multiple expansion alone.

At current levels near $72, Williams appears positioned for steady, fundamentals-driven performance into 2026.

Estimate a company’s fair value instantly (Free with TIKR) >>>

Value Any Stock in Under 60 Seconds (It’s Free)

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>