Key Stats for Nucor Stock

- 52-Week Range: $106 to $235

- Current Price: $227

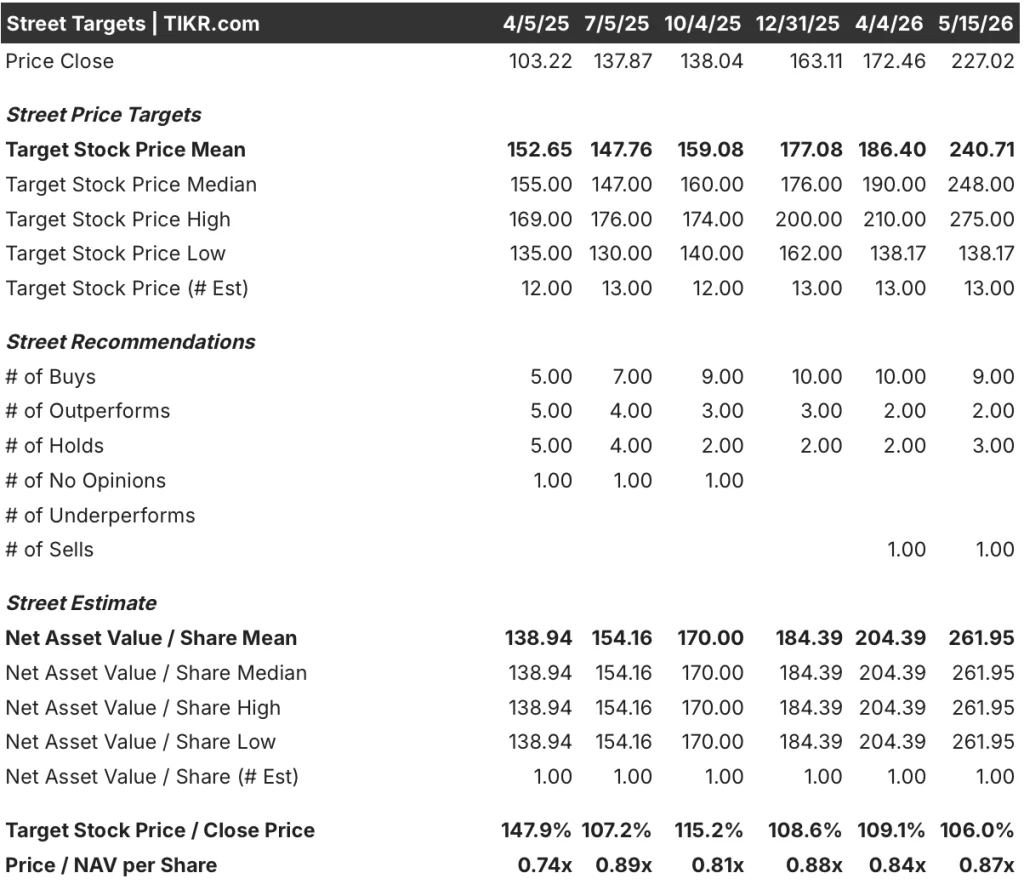

- Street Mean Target: $241

- Street High Target: $275

- Analyst Consensus: Buy (9 Buys, 2 Outperforms, 3 Holds, 1 Sell)

- TIKR Model Target (Dec. 2030): $255

What Happened?

Nucor Corporation (NUE), the largest steel producer in the United States, reported a first-quarter earnings beat so decisive it immediately reframed the company’s earnings trajectory for the rest of 2026.

First-quarter revenue came in at $9.50 billion, clearing the Wall Street consensus of $8.88 billion by $620 million — a 21.3% year-over-year increase driven by higher average selling prices and record shipment volumes across all three operating segments.

The record that stood out most: 7 million tons shipped in the quarter, the highest single-quarter volume in Nucor’s history, with a steel mills backlog of 4.7 million tons exiting March — up 20% from year-end and the highest backlog reading since the second quarter of 2021.

The trade policy environment provided the structural tailwind behind those numbers, with import share of the U.S. finished steel market falling from over 22% in the first quarter of 2025 to approximately 15% in the first quarter of 2026, cutting the supply available to international competitors and tightening domestic pricing conditions.

CEO Leon Topalian stated on the Q1 2026 earnings call that “the pent-up tsunami of earnings power that Nucor has invested is still yet to hit the balance sheet,” citing nearly $20 billion in capital deployment since 2020 and new facilities in West Virginia, Indiana, Utah, and South Carolina now entering commissioning phases.

The West Virginia sheet mill — Nucor’s flagship growth project targeting the automotive and consumer durable markets in the Midwest and Northeast — is roughly 85% complete, with commercial shipments targeted to begin ramping in early 2027 and utilization expected to reach around 50% of capacity by the end of that year.

Wall Street’s Take on NUE Stock

The Q1 earnings beat resets the earnings baseline for the full year upward, and with Q2 guidance calling for higher consolidated earnings across all three segments, the forward trajectory has more momentum than consensus estimates reflected entering the quarter.

NUE’s EBITDA surged to $1.51 billion in Q1, up 117.5% year-over-year, as metal spreads expanded across all product formats and steel mills pretax earnings more than doubled sequentially to $1.13 billion, driven by the structural steel and sheet businesses setting quarterly records.

Eleven of 13 analysts covering Nucor stock have a buy or outperform rating, with a mean price target of $241, implying around 6% upside from current levels — a consensus that has been moving higher as Jefferies raised its target to $225 and JP Morgan raised to $212 in recent weeks, both citing tightening supply conditions and improving trade enforcement.

The spread between the $275 high target and $138 low target reflects a real debate: bulls are pricing in accelerating returns from new capacity as West Virginia ramps, while bears are anchored to the historical cyclicality of steel EPS and the risk that tariff relief proves temporary.

Second-quarter 2026 earnings, expected to show higher consolidated results with sheet and plate named as the largest sequential contributors, will be the first confirmation that the pricing catch-up effect Jack Sullivan described is materializing in realized margins.

What Does the Valuation Model Say?

TIKR’s mid-case model targets $255 for Nucor stock, built on a revenue CAGR of around 2.5% through 2035 and a net income margin of around 9.2%, assumptions that embed the West Virginia ramp but not a second wave of major capital deployment — a conservative but defensible read given where CapEx is trending.

At $227, against a mid-case target of $255, Nucor stock is fairly valued: the 12% total return over the model’s 4.6-year horizon works out to roughly 2.5% annualized, a return profile that reflects an earnings recovery already well-recognized by the Street rather than a mispriced opportunity.

The central tension in the Nucor investment case is whether the structural shift in import share proves durable or reverts as trade policy uncertainty resolves.

What Has to Go Right

- Import share stays near 15%, sustaining domestic pricing power that drove the Q1 $9.50 billion revenue beat and the $1.51 billion EBITDA quarter

- West Virginia begins generating EBITDA-positive output in 2027, adding incremental tons in the Midwest and Northeast where Nucor is currently underweighted

- Steel products backlog growth of 9% from year-end continues as border fence demand (around 1 to 1.5 million tons across 2026 and 2027) extends well into next year

- FCF inflects sharply as CapEx moderates from the $2.5 billion 2026 peak toward a lower run rate, with consensus projecting $0.79 billion in FCF for Q2 2026 alone

What Could Go Wrong

- A USMCA resolution or tariff renegotiation reopens import channels, reversing the supply tightening that reduced import share by 7 percentage points year-over-year

- Pre-operating and start-up costs, which reached $108 million in Q1 and are guided higher through 2026, erode margins further than the earnings ramp offsets

- Scrap and energy cost increases outpace realized pricing in a lagged-contract book, compressing the metal spreads that made Q1 exceptional

- West Virginia commissioning delays push commercial ramp beyond early 2027, extending the window where capital investment costs earnings without yet generating offsetting returns

Should You Invest in Nucor Corporation?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Nucor Corporation stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Nucor Corporation alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze NUE stock on TIKR for Free →