Key Stats for V Stock

- Past week’s performance: around 4.9%

- 52-week range: $294 to $365

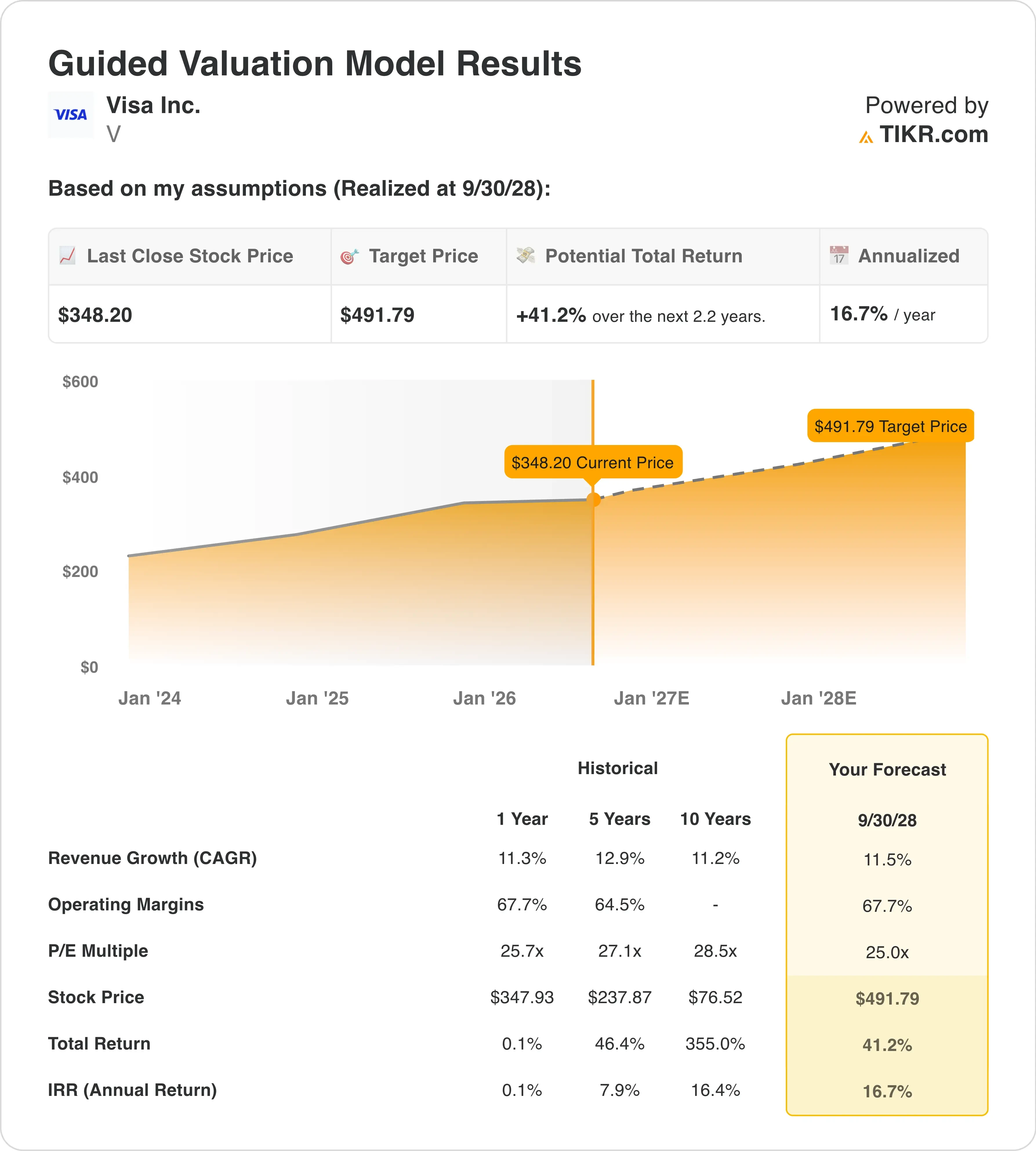

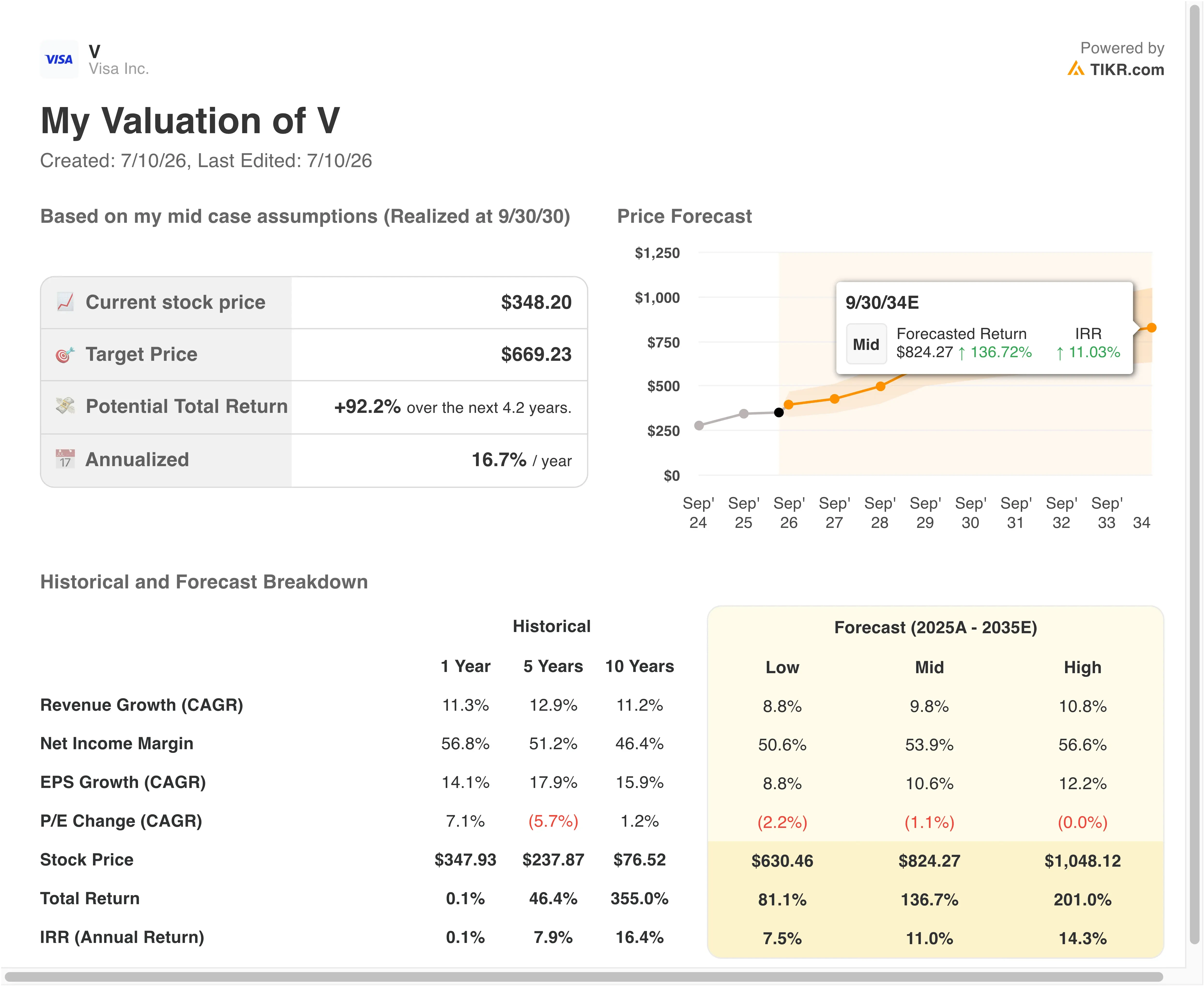

- Valuation model target price: $492

- Implied upside: 41.2% over 2.2 years

Model Visa’s next five years of growth with TIKR’s free Valuation Model (It’s free) >>>

Visa Pushes to a Fresh High

Visa (V) climbed almost 5% this week, closing at a new 52-week high after Baird raised its price target to $412 from $370. The move builds on a strong second-quarter fiscal performance and adds to a stretch in which Visa has quietly outrun the broader market.

Back in late April, Visa reported fiscal second-quarter adjusted earnings per share of $3.31, beating estimates of $3.10, while net revenue climbed 17% to $11.2 billion, the strongest revenue growth since 2013. Management raised its full-year forecast, citing resilient consumer spending across every region it tracks.

CEO Ryan McInerney said the quarter reflected “resilient consumer spending” and strength across payments, commercial solutions, and value-added services. Cross-border volume excluding Europe grew 11%, and processed transactions rose 9% to 66.1 billion. Visa also authorized a fresh $20 billion buyback on top of the $7.9 billion it already repurchased during the quarter.

Visa has also expanded its stablecoin and AI ambitions this month, launching the Visa Stablecoin Platform and investing in Replit to power agentic payments for developers. Going forward, investors will watch whether Visa’s premium valuation can hold as it heads into fiscal third-quarter results.

See analysts’ growth forecasts and price targets for V (It’s free) >>>

Is V Stock Undervalued?

Under valuation model assumptions realized through 12/31/28, the stock is modeled using:

- Revenue growth (CAGR): 11.5%

- Operating margins: 67.7%

- Exit P/E multiple: 25.0x

Based on these inputs, the model estimates a target price of $492, implying a 34.7% upside from the current price and a 14.5% annualized return over the next 2.2 years.

Energy Transfer’s Q1 results showed stronger cash generation and raised guidance, which suggests the rally may still have room to run. The stock’s move from its 52-week low reflects improving fundamentals, but investors should still watch pipeline volumes, distribution coverage, and the next quarterly update. An annualized return near 14.5% still sits close to the 15% threshold that typically signals an attractive setup, even for a stock trading at all-time highs.

Estimate a company’s fair value instantly (Free with TIKR) >>>

Visa Versus the Card Networks

Mastercard (MA) is Visa’s closest peer, and the two now trade at similar multiples. Mastercard trades at 24 times forward earnings, just below Visa’s 25 times. Last quarter, Mastercard posted 16% revenue growth and 23% adjusted EPS growth. Both figures slightly exceeded Visa’s recent 17% revenue growth and 20% EPS growth.

American Express (AXP) trades at roughly 18 to 20 times forward earnings, several turns cheaper than Visa or Mastercard, despite guiding for 9% to 10% revenue growth and EPS growth in the mid-teens for 2026. That discount exists because Amex lends directly to cardmembers and carries real credit risk, unlike Visa and Mastercard, which simply process transactions without holding loans on their balance sheets.

Visa and Mastercard get rewarded with premium multiples for their asset-light, toll-booth-style economics, while Amex gets a lower multiple despite comparable earnings growth because the market prices in credit cycle risk.

Read our full take on Visa’s earnings, margins, and valuation upside >>>

What’s Driving Visa Stock Going Forward?

Visa’s fiscal third-quarter report arrives July 28, and investors will be watching whether cross-border and commercial payment growth can sustain their current pace after such a strong prior quarter.

Stablecoin and agentic commerce initiatives represent a longer-term growth lever. Visa’s new Stablecoin Platform and its investment in Replit both point to the company positioning itself at the center of how payments evolve over the next decade, alongside its existing partnership with OpenAI.

Regulatory scrutiny in the UK and Europe remains the biggest wildcard, with proposed profitability reporting rules that could eventually pressure margins. For now, though, Visa’s combination of steady spending trends, buyback firepower, and fresh analyst upgrades continues to underpin the bull case.

Estimate a company’s fair value instantly (Free with TIKR) >>>

Should You Invest in Visa?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up V, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track V alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!