Key Stats for Diamondback Energy Stock

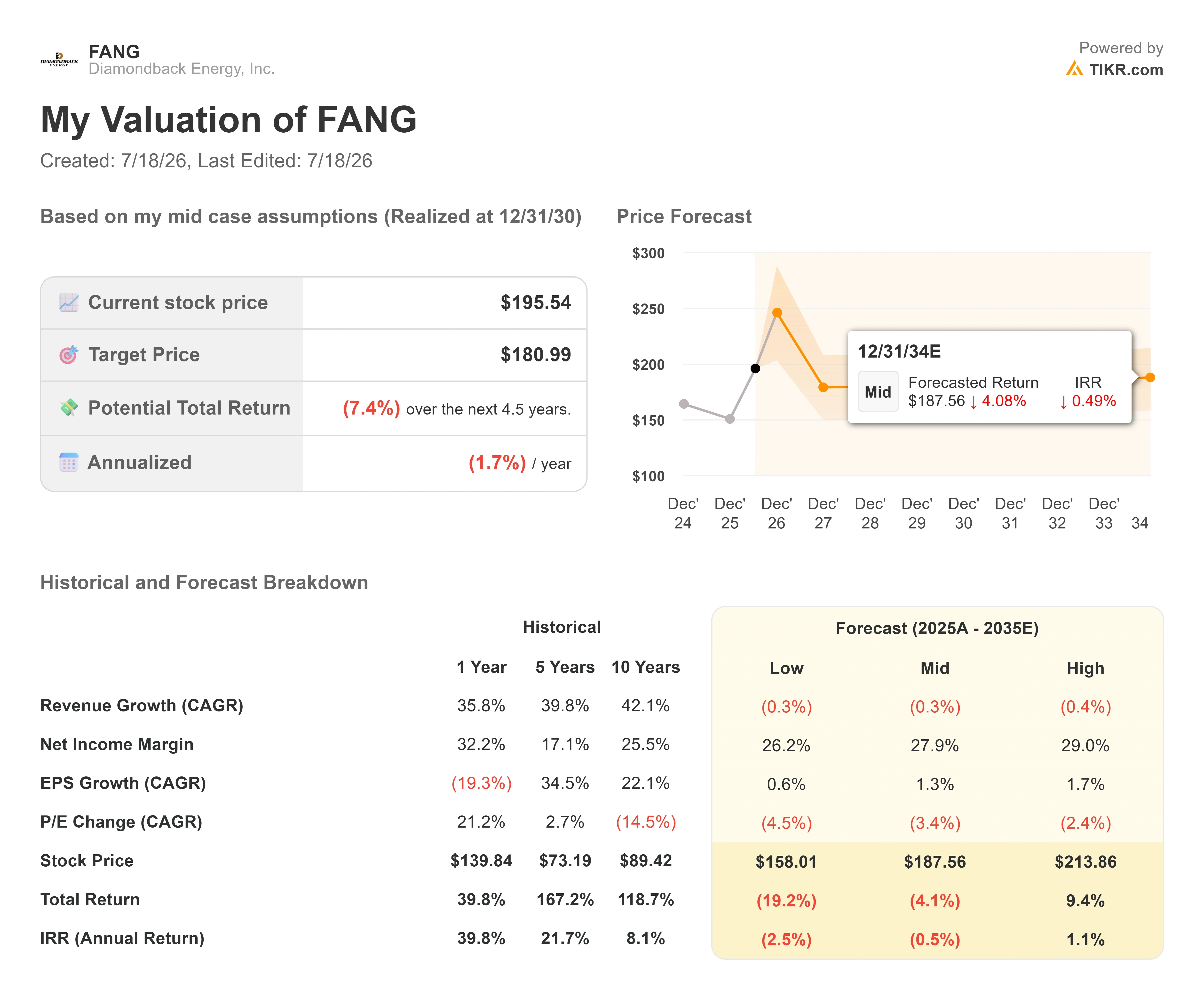

- Current Price: $195.54

- Target Price (Mid): ~$181

- Street Target: ~$229

- Potential Total Return: ~(7%) over 4.5 years

- Annualized IRR: ~(2%) / year

- Max Drawdown: 19.53% (July 1, 2026)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

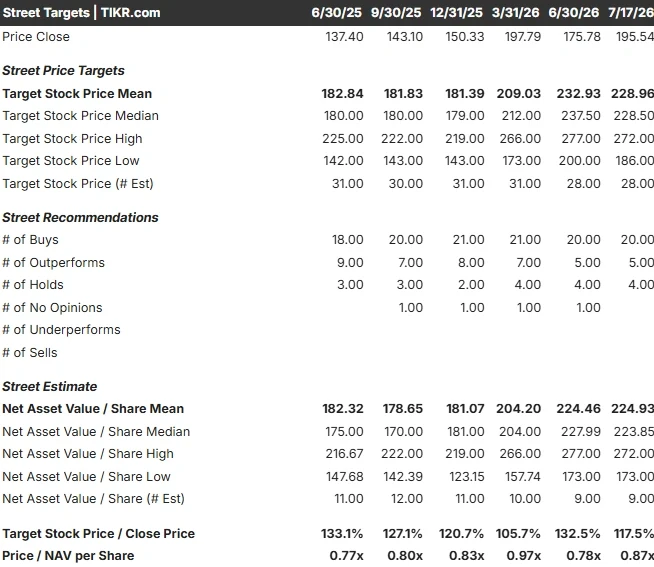

Diamondback Energy (FANG) closed at $195.54 on July 17, near the top of a 52-week range that runs from $134.30 to $214.51, carried by a crude rally that lifted the entire Permian complex. Over the same month, the analysts who cover it moved their price targets the other way. JPMorgan cut to $211 from $240. Truist went to $220 from $242. Both reductions kept their bullish ratings attached. The targets fell, the ratings held.

The detail that reframes the whole picture sits in the company’s own words. Asked on the Q1 call whether the oil shock had lifted its long-term price assumptions, management said no. That means the CEO of the most oil-levered large producer in the Permian is planning around roughly the same conservative crude deck the bears are using, and so is TIKR’s valuation model. The bulls buying the rally are the odd ones out. The question the market cannot yet answer is whether management is being too cautious or whether the rally is simply ahead of the fundamentals.

The Rally Was Made of Crude, Not Company News

The move that carried Diamondback back toward its highs did not come from Midland. The most likely driver came from the Strait of Hormuz. On July 13, crude jumped more than 4% as renewed friction between the United States and Iran raised fresh doubts about supply flows through the world’s most important oil chokepoint. Diamondback, a nearly pure-play Permian Basin producer (its business is drilling and producing oil and gas from West Texas rock), tracks the commodity closely, and shares rose about 4% that session. The stock added another 2.85% on July 17 as crude stayed firm.

This tells what is actually driving the tape. Diamondback did not announce a contract, a discovery, or a guidance raise last week. The bid was macro. That cuts both ways: the same crude sensitivity that pushed shares up can reverse just as fast if the geopolitical premium leaves oil, which is exactly what analysts began modeling when they trimmed targets.

See historical and forward estimates for Diamondback Energy stock (It’s free!) >>>

Management Will Not Raise Its Oil Deck, and That Is the Tell

Here is the passage that matters more than any headline. Asked directly whether the conflict had pushed up the mid-cycle oil price the company plans around, CEO Kaes Van’t Hof declined to move it: “It’s hard for us to move off our mid-cycle pricing environment, which is kind of a mid-$60s TI.” He added that it was “a little too early for us to go higher on mid-cycle pricing today.”

Read that against a stock trading as if triple-digit oil is permanent. The lowest-cost operator in the basin, sitting on the largest cash windfall in its history, is still underwriting its business at mid-$60s WTI. That single choice explains the analyst cuts better than any macro note: when the United States and Iran reached a memorandum of understanding in mid-June and crude drifted back toward pre-conflict levels, the banks that had modeled elevated oil marked their assumptions down toward the level management was already using. The ratings stayed bullish because, even at a lower target, the Street mean target near $229 still sits well above today’s $195.54, on an analyst board of 20 Buys, 5 Outperforms, 4 Holds, and zero Sells.

Van’t Hof is not bearish on his own company. He is disciplined about what he will capitalize. That discipline shows up in capital returns too: the company has bought back 42 million shares for $6 billion at an average of $148, and management signaled it will now lean toward paying down debt over repurchases while oil is high, precisely because it does not want to buy its own stock at a price the cycle might not defend.

What the Skeptical Deck Does to the Numbers

The operating results are strong on their own terms. First-quarter revenue was $4.24 billion, beating estimates by 7.9%, and adjusted earnings hit $4.23 per share, nearly 13% ahead of consensus. Free cash flow reached $1.71 billion, up 10% year over year, and management raised full-year oil guidance above 520,000 barrels per day. The company also raised its base dividend, reportedly by 5% to $1.10 per share. None of the operating strengths is in dispute.

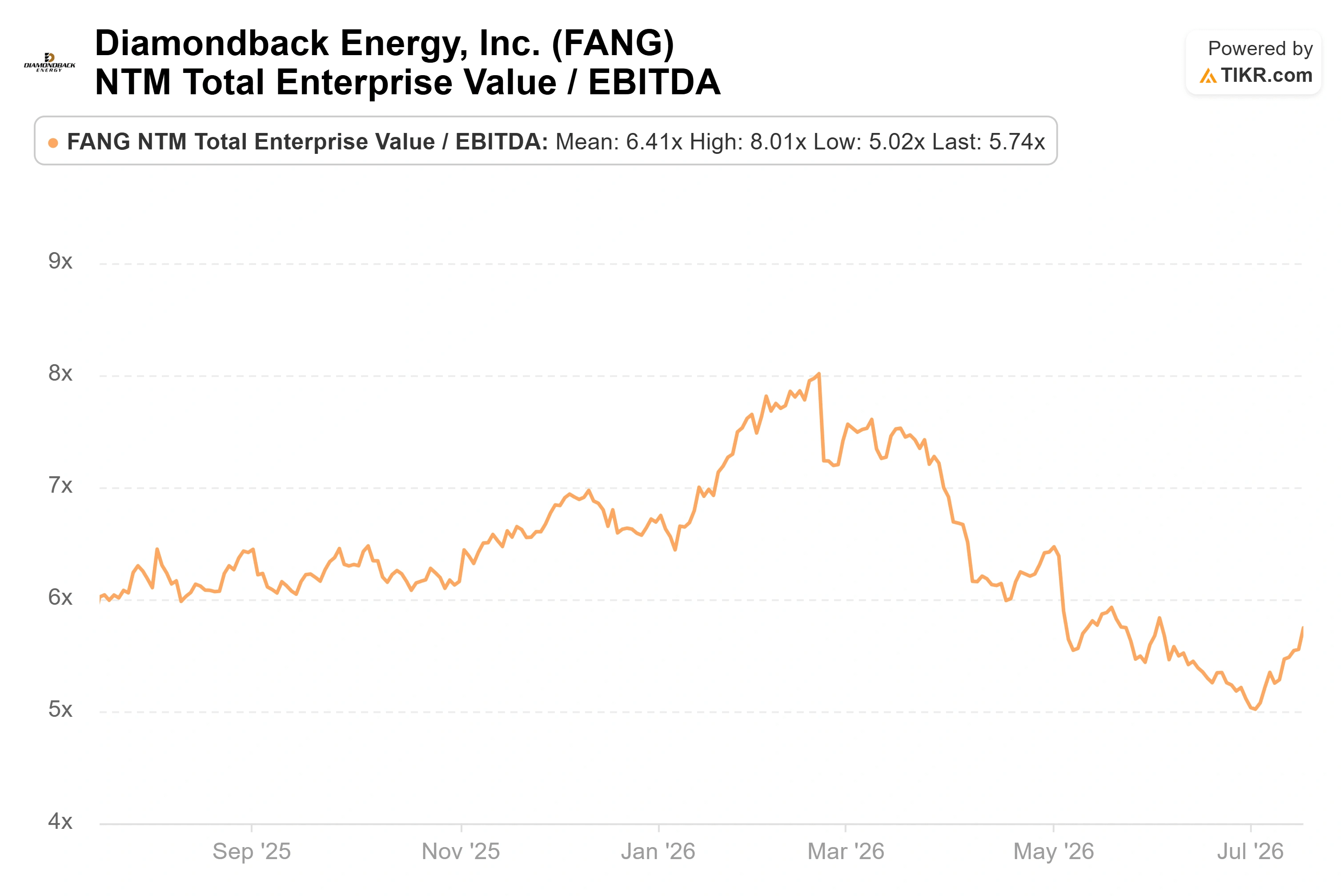

Diamondback trades at an NTM EV/EBITDA (enterprise value against next-twelve-months earnings before interest, taxes, depreciation, and amortization) of about 5.8x, a premium to Devon at 3.9x, EOG at 4.6x, Occidental at 4.8x, and ConocoPhillips at 5.2x, per TIKR’s Competitors page. The premium is defensible on inventory depth and cost structure. But a premium multiple resting on a crude price that the company itself refuses to underwrite is the exact spot where a stock gets fragile. If oil holds, the premium is cheap. If oil reverts to the mid-$60s in management’s own model, the premium is the first thing to compress.

See how Diamondback Energy performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $195.54

- Target Price (Mid): ~$181

- Potential Total Return: ~(7%) over 4.5 years

- Annualized IRR: ~(2%) / year

See analysts’ growth forecasts and price targets for Diamondback Energy stock (It’s free!) >>>

TIKR’s mid-case model reaches the same conclusion as management’s oil deck implies. From $195.54, it values the stock at around $181, a total return of roughly negative 7% over the next 4.5 years, or about negative 2% annualized. The two drivers doing the work are Permian production growth and net income margins near 28%, while the multiple compresses as oil normalizes. The single largest risk is also the only real swing factor: the oil price. If crude holds triple digits, the model is far too conservative, and the high case near $214 comes into view. If the geopolitical premium drains and WTI settles into the mid-$60s, the CEO named, this negative-return path is the honest base case.

The gap between TIKR’s ~$181 and the Street’s ~$229 is a $48 disagreement about what a barrel of oil is worth over five years, expressed as a stock price. What is unusual this month is that the company’s own management is standing closer to the model than to the Street.

Conclusion

Everything compresses into August 3, when Diamondback reports second-quarter results after the close, with the call the morning of August 4. Watch one thing above all: whether management moves its mid-cycle oil assumption off mid-$60s. That is the only signal that closes the gap to the Street’s $229, and Van’t Hof has now twice declined to move it. If the second-quarter commentary finally lifts the deck, the bulls are vindicated, and the target cuts were early. If management holds the line at mid-$60s while realized prices stay hot, then the CEO, the analysts trimming targets, and TIKR’s model are all telling the same thing the rally is ignoring. Come back on August 4 and see which way the deck moves.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Diamondback Energy?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Diamondback Energy, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Diamondback Energy alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Diamondback Energy on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!