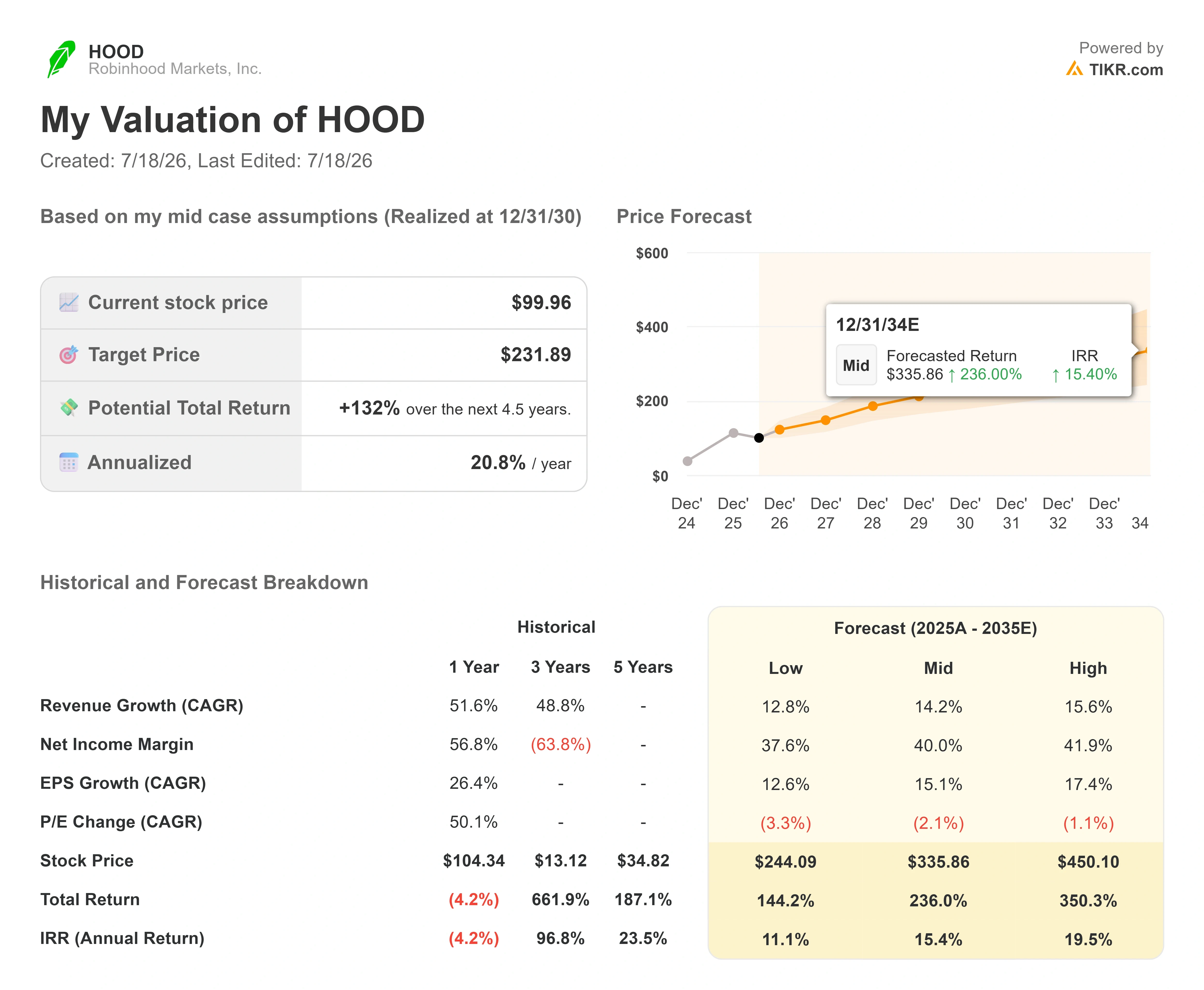

Key Stats for Robinhood Stock

- Current Price: $99.96

- Target Price (Mid): ~$230

- Street Target: ~$118

- Potential Total Return: ~132%

- Annualized IRR: ~21% / year

- Max Drawdown: 57.26% on 3/30/26

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Robinhood Markets (HOOD) has spent 2026 trying to convince investors it is no longer a bet on crypto trading volumes. In mid-July, the market started testing what it is becoming instead. Shares closed July 17 at $99.96, down 5.72% on the day and roughly 9% over the week, sliding back to the psychologically loaded $100 line after a summer rally had carried them above $120.

The July 17 drop was mostly a broad fintech and crypto selloff, with Cathie Wood’s ARK reportedly trimming its position adding pressure. But the story that defined the week was more specific to Robinhood. Bulls have spent months arguing that the company’s expansion beyond brokerage, into banking, credit cards, and wealth management, is exactly what de-risks the story. Bears now have a concrete piece of evidence to argue the opposite: the company is wading into capital-intensive lending, and it is funding that ambition with debt.

The Bond Sale That Gave Consumer-Finance Skeptics Something Real

On July 13, Bloomberg reported that Robinhood is gauging investor demand for its first-ever bond backed by credit-card receivables. The company is looking to sell at least $400 million, potentially up to $500 million, of asset-backed securities, meaning bonds repaid from the balances Robinhood’s cardholders owe. The deal is split into four tranches, with Wells Fargo and Barclays managing it, and Coastal Community Bank identified by Fitch as the originator of the underlying accounts.

This is a reported offering still gauging interest, not a closed transaction, and that distinction matters. A securitization is normal plumbing for any lender. The question investors are chewing on is whether Robinhood should be a lender at this scale at all. Packaging card debt into bonds ties a slice of the company’s future to credit performance, an area where trading platforms have no track record and where losses tend to surface precisely when retail customers are most stretched.

The timing sharpens it. Robinhood launched a $695 platinum-plated card in March to compete with American Express, and only closed a $2.2 billion convertible note offering in late June. A company that spent years selling itself as an asset-light software platform is now assembling the funding stack of a consumer bank. The selling pressure came even as Goldman Sachs was reported to have kept its Buy rating and lifted its target to $137, a reminder that Wall Street’s near-term read stayed bullish while the tape did not.

See historical and forward estimates for Robinhood stock (It’s free!) >>>

Why Management Thinks the Skeptics Are Reading It Backwards

Robinhood’s leadership frames this expansion as the payoff, not the risk. At the Piper Sandler conference on June 4, Chief Brokerage Officer Steve Quirk pointed to deposits as the tell on how the ecosystem is landing. He said the banking product had reached $2.5 billion in balances with 800,000 cardholders, then added a line that reframes the debate: “If you ever want to ask us how we’re doing as a company and how we’re doing with engaging with customers, just look at how we’re doing with deposits.”

That matters because it reveals what the card is actually for. In Robinhood’s telling, it is not a standalone lending gamble. It is the glue binding a customer to an ecosystem that already holds their trades, their cash, and increasingly their long-term wealth. Quirk noted that 40% of new banking customers set up direct deposit, the stickiest relationship a financial app can win. Seen that way, securitizing card balances is a lender funding a book it always intended to build.

The bulls and bears are not really arguing about the bond. They are arguing about whether Robinhood’s 27.5 million mostly young customers become a durable, cross-sold asset base, or whether the company is bolting credit risk onto a business still tethered to volatile trading revenue.

What the Multiple Is Actually Paying For

Robinhood reported first-quarter 2026 revenue of $1.067 billion and net income of $427.45 million. The three-year revenue growth rate sits near 49%. The stock trades at roughly 38 times forward earnings and about 30 times next-twelve-months free cash flow, rich on their face but not obviously so for a business compounding at this pace.

Against its capital-markets peers, the multiple looks stretched on some metrics and defensible on others. Coinbase trades near 62 times forward earnings and Interactive Brokers near 33 times, which places Robinhood’s P/E in the middle of a wide pack rather than at an obvious extreme. The premium the market assigns holds only if growth and margins do, and that is exactly what the bond news put in play. The summer recovery was never really about crypto. It was the market starting to price the ecosystem, and July 17 was the market pausing to ask whether consumer credit adds value or fragility to the free cash flow story.

See how Robinhood performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $99.96

- Target Price (Mid): ~$230

- Potential Total Return: ~132%

- Annualized IRR: ~21% / year

See analysts’ growth forecasts and price targets for Robinhood stock (It’s free!) >>>

The two revenue drivers are ecosystem monetization, meaning Gold subscriptions and banking deposits deepening revenue per customer, and product expansion into prediction markets, retirement accounts, and international launches. The margin driver is operating leverage, with the mid case assuming net income margins near 40% as the revenue base scales, helped by June’s workforce reduction. The primary risk is native to this article’s whole subject: credit performance on the card book. If charge-offs climb as the receivables portfolio grows, the securitization that looks like smart funding today becomes a drag on the free cash flow the model leans on. The upside is a durable, cross-sold financial super-app that earns a premium multiple. The downside is a high-beta broker carrying a new layer of consumer-credit risk at a valuation that leaves little room for a stumble.

The gap between this ~$230 model target and the ~$118 Street mean is a horizon gap, not a contradiction. The Street is pricing the next year; the TIKR mid case is pricing roughly four and a half years of compounding. Both can be right.

Conclusion

The number to watch is not the bond. It is July 29, when Robinhood reports second-quarter results after the close. Watch two lines: net deposit growth and the direction of transaction revenue. Deposits comfortably above the roughly $18 billion pace investors have anchored to would validate Quirk’s ecosystem argument and make the credit-card build look like a lender funding real loyalty. A second straight quarter of soft trading revenue would hand the bears their proof that the growth engine still runs on market volatility. The bond only matters because of which of those two stories it ends up attached to, and July 29 is when the market starts to find out.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Robinhood?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Robinhood, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Robinhood alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Robinhood on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!