Key Stats for Tesla Stock

- Current Price: $380.84

- Target Price (Mid): ~$454

- Street Target: ~$425

- Potential Total Return: ~19%

- Annualized IRR: ~4% / year

- Max Drawdown: 29.93% (April 8, 2026)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

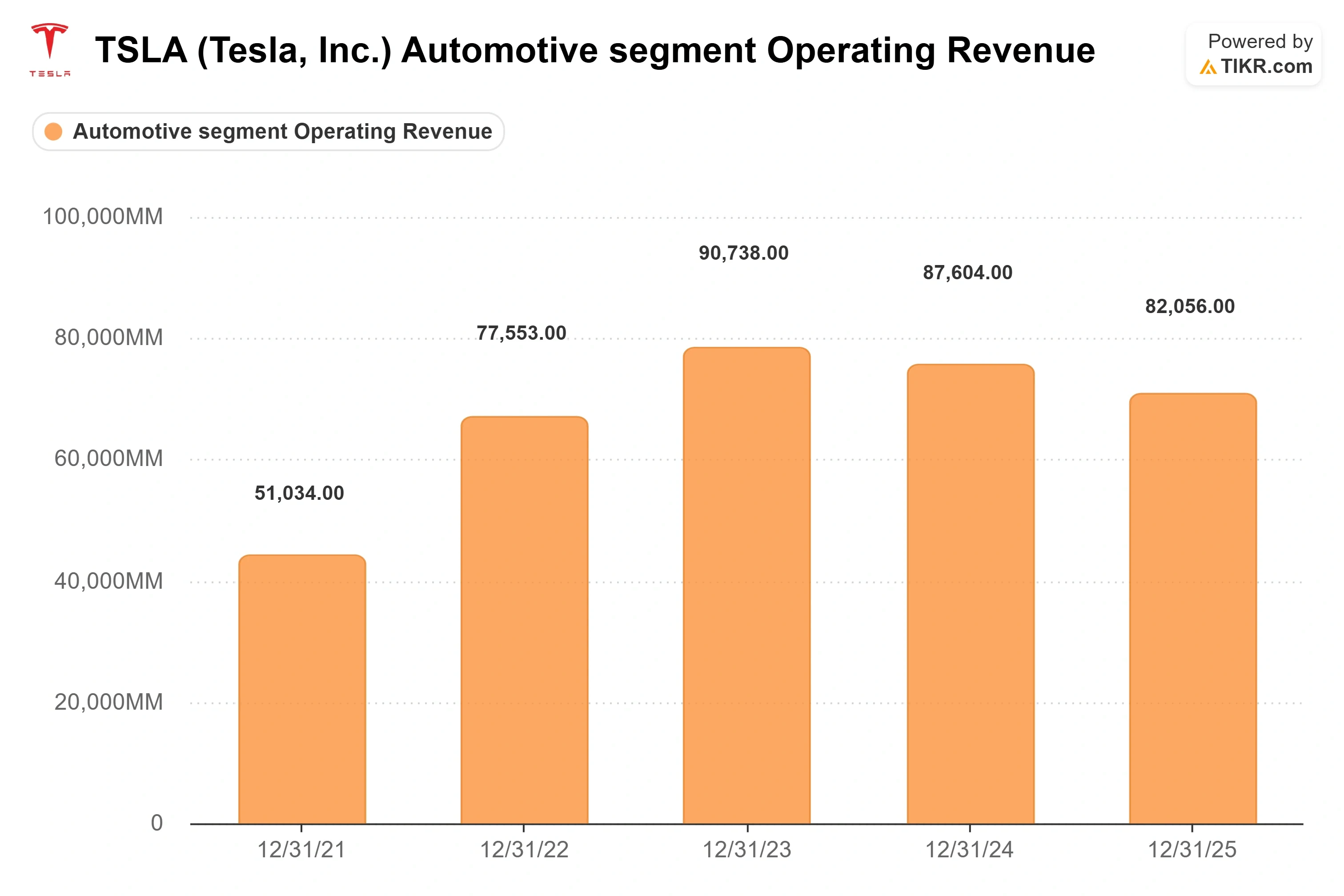

Tesla (TSLA) spent two weeks proving that its biggest number no longer moves its stock. The company delivered a record 480,126 vehicles in the second quarter, beat Wall Street’s estimate by more than 74,000 cars, ended a two-year slide in sales, and watched shares fall about 7.5% on the July 2 delivery release. Four sessions later, the stock rallied back near $420, then drifted lower to close at $380.84 on July 17. If that path looks like a market that cannot make up its mind, you are reading it correctly.

The reason is simple. Investors already know how many cars Tesla built. What they do not know, and will not know until the full results land after the close on July 22, is whether those cars made any money. That is the entire debate now. Bulls point to a demand recovery, and the autonomy story management keeps selling. Bears counter that the last margin print was flattered by benefits that will not repeat.

Wall Street Has Already Set the Bar at 18%

The fresh signal this week is how sharply analysts disagree on the one figure that matters. That figure is automotive gross margin excluding regulatory credits, which strips out the emissions credits Tesla sells to other carmakers and shows what building cars actually earns. Consensus expects around 18.2% for the quarter. Wells Fargo’s Colin Langan, who reaffirmed a Sell, models just 16.8%, per TipRanks. That gap is the whole story: a print at or above 18% says the recovery is structural, and a print in the mid-teens says the record quarter came by giving margin away.

The catch is what propped up the last number. That margin climbed for four straight quarters, reaching 19.2% in the first quarter of 2026, per Tesla’s shareholder deck. Management admitted the Q1 figure was helped by one-time items, specifically warranty true-downs of around $230 million and some tariff relief. Deutsche Bank estimates the warranty benefit alone was closer to $150 million and expects its unwind to be a sequential headwind this quarter, with no offsetting benefit yet realized from the Supreme Court’s IEEPA tariff ruling. So the real test is not whether the margin holds. It is whether it holds without the crutch.

The headline earnings line carries the same tension. Consensus points to adjusted earnings per share near $0.52, up roughly 30% year over year, on revenue of about $26 billion, though published estimates range widely, with some Street models sitting in the mid-$0.40s. A clean margin beat without one-time help changes the story. A miss revives every valuation worry the stock has carried all year.

See historical and forward estimates for Tesla stock (It’s free!) >>>

Why the Market Stopped Caring About Car Sales

The deeper reason a record quarter got a shrug is that Tesla is no longer priced as a car company. It trades at roughly 168 times forward earnings and about 81 times forward EBITDA, per TIKR data as of July 17. Those are not automotive multiples. They exist because the market is paying for Robotaxi, Full Self-Driving (the driver-assistance software Tesla sells as a subscription), Optimus (its humanoid robot), and AI infrastructure, none of which generate material revenue today.

That gap between valuation and current earnings is why the delivery beat could not lift the stock for long. The car business is the thing funding the bets, and in the first quarter, it ran a slim automotive-side operating margin, roughly 4% at the group level, even as its trailing profitability across all segments sits higher. Management has reframed the whole company around closing that gap. As CFO Vaibhav Taneja put it on the last call, describing a shift in how Tesla sells: “We now emphasize FSD as a product and vehicle as only the delivery mechanism.” That line matters because it tells you where management thinks the next margin comes from: software, not sheet metal.

The autonomy programs are real and progressing. Robotaxi runs in Austin, Dallas, and Houston with zero reported incidents, and the service expanded to Miami in early July without a human safety monitor on board, a first for the program. FSD reached nearly 1.3 million paid customers globally at the end of the first quarter. But none of it pays the bills this year.

The $25 Billion That Hangs Over the Print

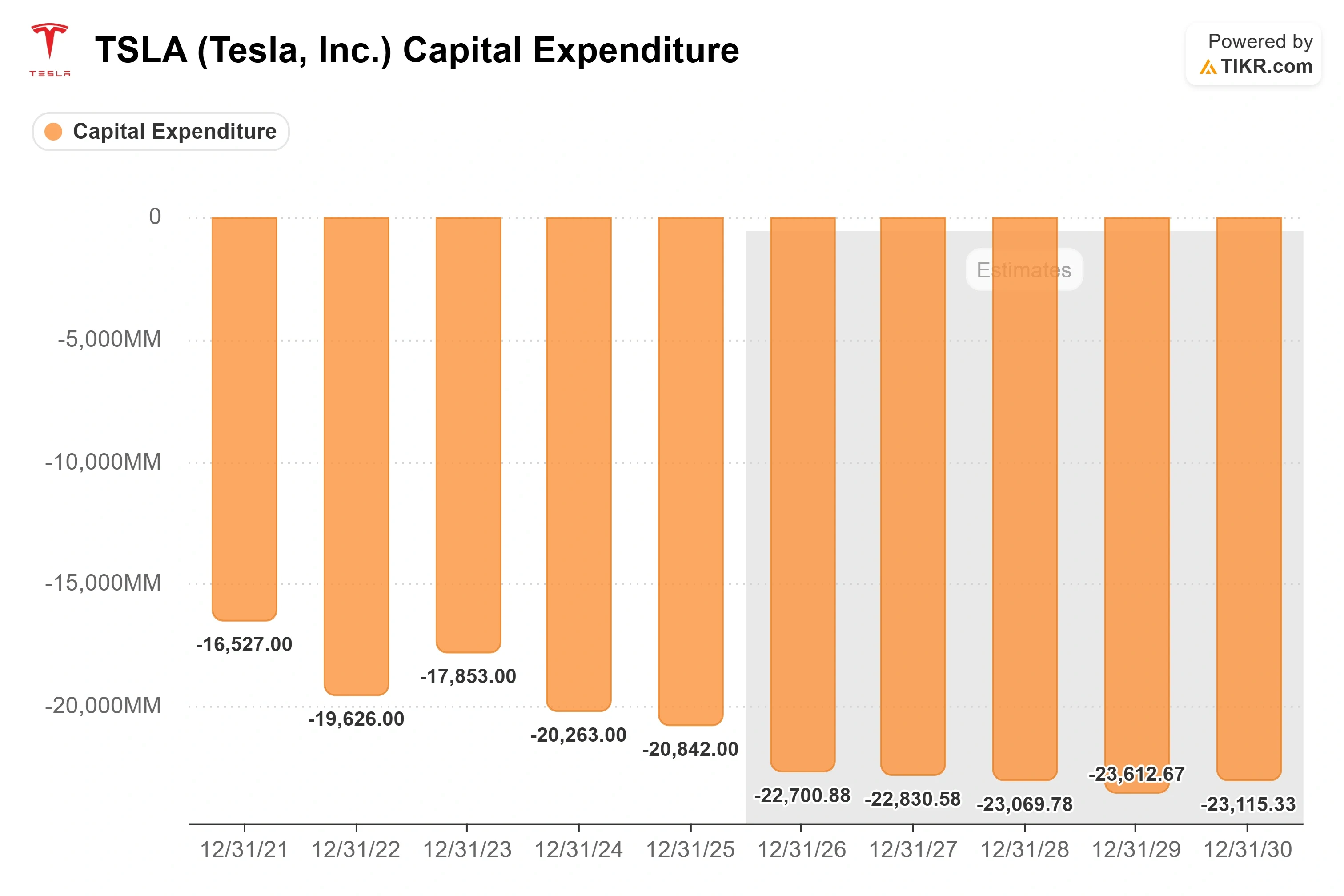

The spending behind those bets is the number bears cite most. On the Q1 call, Taneja guided full-year 2026 capital expenditure above $25 billion and said free cash flow would be negative for the remaining quarters of the year as six factories, an AI5 inference chip, and a research semiconductor fab come online. That is management’s own guidance, not a model output, and it is why the cash flow trajectory hangs over the valuation. A delivery record alone cannot re-rate the shares while the company is telling investors it will spend through its own cash generation to fund products that do not yet sell at scale. That is why July 22 rests on the margin line: it is the one place the market can check whether the business funding all of this is getting stronger or weaker as it scales.

See how Tesla performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $380.84

- Target Price (Mid): ~$454

- Potential Total Return: ~19%

- Annualized IRR: ~4% / year

See analysts’ growth forecasts and price targets for Tesla stock (It’s free!) >>>

Using TIKR’s mid-case, the model lands at approximately $454 by the end of 2030, about 19% total return from here, or roughly 4% annualized. That case is built on a revenue CAGR of around 3% and EPS growth of about 9% a year, with net income margin holding near 13%. The two revenue drivers are a stabilizing automotive line lifted by higher-margin FSD subscriptions and services, and energy storage, where deployments reached 13.5 GWh in the second quarter. The margin driver is mix, as software and services carry far higher margins than vehicles. The primary risk is the capex burn: if Robotaxi and Optimus revenue arrives later than management promises, that modest return compresses fast.

The upside is that autonomy scales on schedule and Tesla re-rates on a proven software business rather than a promised one. The downside is that the multiple stays demanding while the new products slip, leaving a carmaker priced at more than 300 times trailing earnings.

Conclusion

Watch one line when results drop after the close on July 22: automotive gross margin excluding regulatory credits. Consensus wants 18.2%; the bears model 16.8%. A number at or above 18% without a one-time warranty or tariff helps confirm core car profitability is genuinely improving, and the record quarter becomes a real earnings catalyst instead of a volume story. A number sliding toward the mid-teens tells you deliveries came by surrendering margin, and every valuation fear the stock carried in 2026 comes straight back. The deliveries are already in the price. Whether they made money is the only thing left to find out.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Tesla?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Tesla, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Tesla alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!