Key Stats for Vertex Pharmaceuticals Stock

- Past-Week Performance: +4%

- 52-Week Range: $362.5 to $619.7

- Current Price: $474.3

What Happened?

Vertex Pharmaceuticals stock (VRTX) trades at $474.27 after a 2.4% pullback, yet 77,000 CF patients on therapy and $12.3 billion in cash signal a company running far ahead of its stock price.

Multiple Vertex executives, including EVP and Chief Commercial Officer Duncan McKechnie and Chief Legal Officer Jonathan Biller, disposed of common shares between February 18 and March 2, while the stock sits 8.8% below its 52-week high of $519.68.

Vertex posted $12 billion in full-year 2025 revenue, grew Q4 earnings 24% year-over-year to $1.3 billion, and guided 2026 revenue to $12.95 billion to $13.1 billion, with non-CF products alone targeting $500 million or more.

Meanwhile, the pending pove IgAN interim analysis from the RAINIER trial, confirmed for H1 2026, carried additional weight after Reshma Kewalramani, CEO, stated on the Q4 earnings call that “pove is administered as a once-monthly small volume subcutaneous dose delivered via an auto-injector,” a profile nephrologists have already flagged as their preferred administration format across 74 payer engagements covering 210 million lives.

With TRIKAFTA patents intact until 2037, ALYFTREK protected beyond that, and four commercial verticals converging alongside five pivotal-stage programs, Vertex enters a multi-year window where renal alone, anchored by pove across IgAN, membranous nephropathy, and myasthenia gravis, could rival the scale of its CF franchise.

Wall Street’s Take on VRTX Stock

Vertex’s confirmed H1 pove IgAN interim readout from the RAINIER trial directly determines whether management completes its BLA submission and unlocks a renal franchise analysts expect to rival CF in scale.

The fundamental case holds firm: revenue grows from $12 billion in 2025 to an estimated $13 billion in 2026, while normalized EPS climbs from $18.40 to $19.17, sustaining a business that has compounded revenue at 14.1% annually over five years.

As of March 3, Wall Street carries 21 buys, 4 outperforms, 5 holds, and 1 sell, with a mean price target of $535.56 representing 12.9% upside from $474.27, reflecting analysts upgrading conviction into a post-earnings pullback rather than fading the story.

The analyst target range spans $330 to $625, where the low assumes pove disappoints and JOURNAVX gross-to-net normalization stalls, while the high requires a clean RAINIER interim and JOURNAVX prescriptions tripling as management guided for 2026.

What Does the Valuation Model Say?

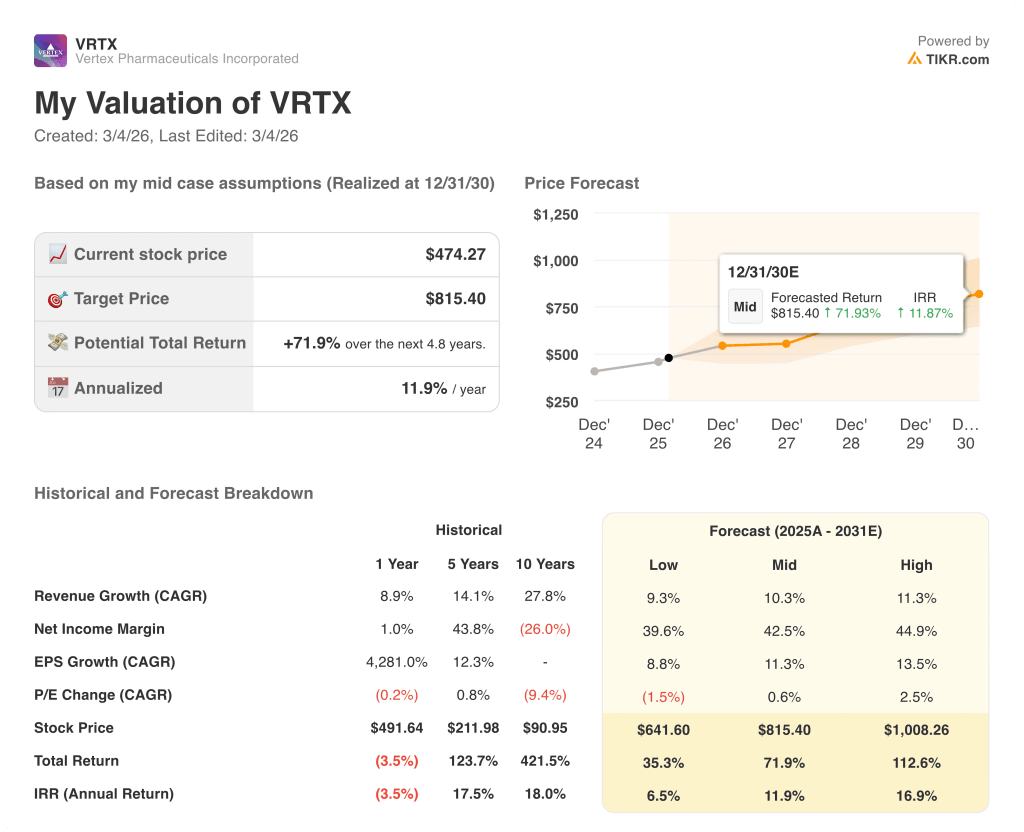

The valuation model prices VRTX at $815.40 by December 2030, implying 71.9% total return and an 11.9% annualized IRR from current levels, a gap the market has not yet closed despite five consecutive years of double-digit revenue growth.

Regardless, the market prices VRTX as a maturing CF company, yet non-CF revenue targets $500 million or more in 2026 alone. Normalized net income margins expand toward 42.5% at mid-case through 2031, compressing the perceived risk of CF concentration. Management’s 74 payer engagements covering 210 million lives signals a commercial infrastructure already built ahead of pove’s approval, not after.

The RAINIER interim data arriving in H1 represents the single event most likely to force a sentiment re-rating from “CF incumbent” to “multi-franchise compounder.”

The thesis breaks if pove’s RAINIER interim misses the investor-expected 47% UPCR reduction, stalling the BLA and eliminating the renal growth narrative that justifies the $535.56 mean target.

The pove IgAN interim analysis, confirmed for H1, will either validate or reset the entire renal franchise thesis that underpins the $815.40 model target.

Therefore, VRTX stock seems to be undervalued at $474.27, with a model-implied 71.9% total return and a binary H1 catalyst that could close the gap fast.

Should You Invest in Vertex Pharmaceuticals Incorporated?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up VRTX stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Vertex Pharmaceuticals Incorporated alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze VRTX stock on TIKR for Free →