Key Stats for United Parcel Service Stock

- 6-Month Performance: 35%

- 52-Week Range: $82 to $124

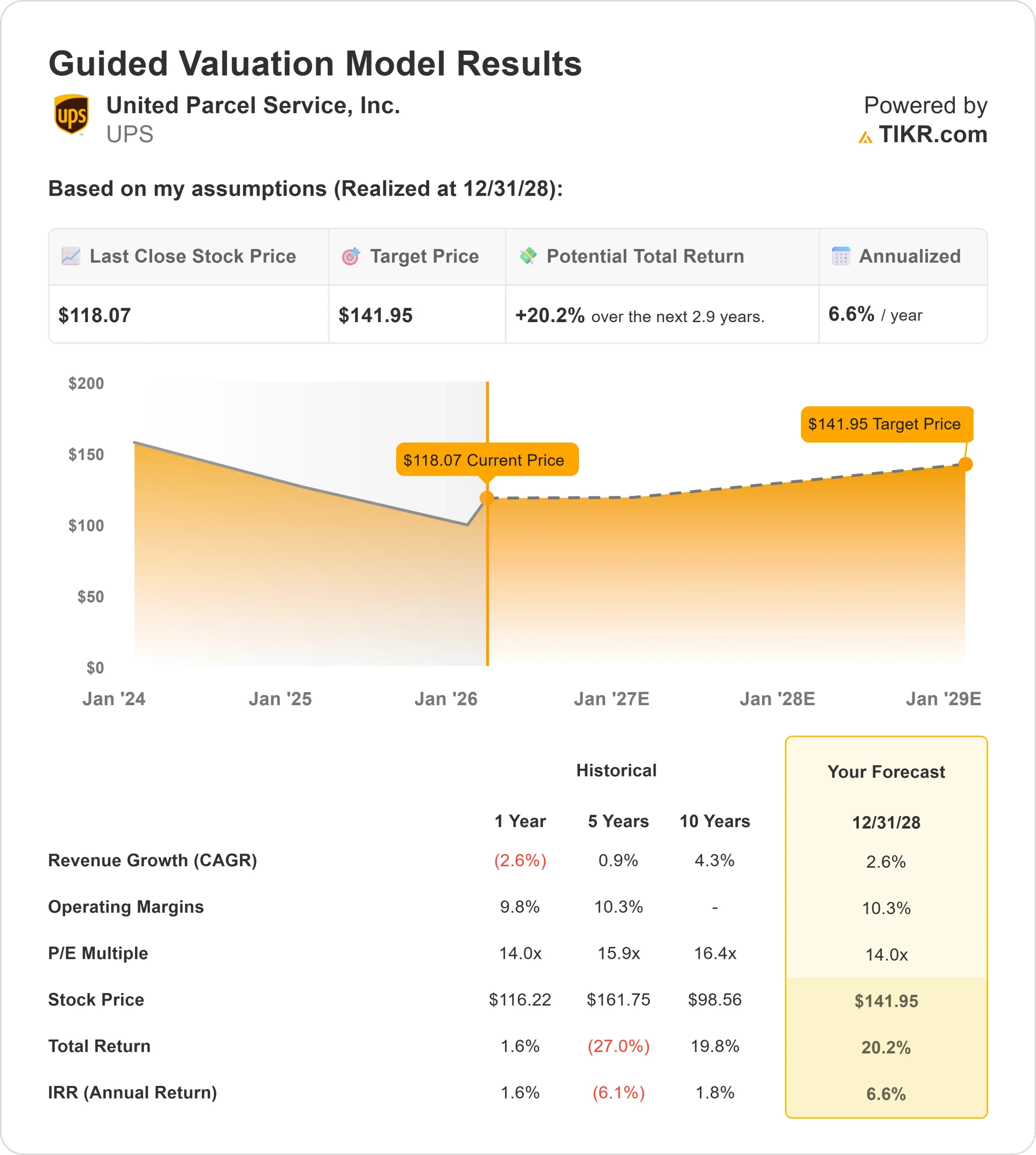

- Valuation Model Target Price: $142

- Implied Upside: 20%

Value your favorite stocks like United Parcel Service with 5 years of analysts’ forecasts using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

United Parcel Service stock has surged about 35% over the past six months, recently trading near $118 per share as investors responded to improving revenue quality, aggressive cost restructuring, and clearer visibility into 2026 margins.

Shares remain below the 52-week high of $124 but well above the $82 low, reflecting a meaningful recovery in sentiment.

The rally accelerated as management outlined the final phase of its Amazon glide-down strategy while maintaining pricing discipline and improving mix.

Fourth-quarter results exceeded expectations, and investors gained confidence that the company can stabilize margins despite near-term transition costs tied to the USPS Ground Saver shift and fleet modernization.

This quarter, UPS reported revenue of $24.5 billion, operating profit of $2.9 billion, operating margin of 11.8%, and adjusted EPS of $2.38.

CEO Carol Tomé stated results “exceeded our expectations,” while the company delivered $3.5 billion in savings in 2025 and reduced Amazon volume by roughly 1 million pieces per day.

Management guided 2026 revenue to approximately $89.7 billion with a consolidated operating margin of about 9.6%, setting clearer expectations for the year ahead.

Institutional positioning also showed continued engagement. Wealthfront Advisers increased its stake by 18.6% to 98,676 shares worth about $8.24 million, Oppenheimer & Co. raised its position 14.7% to 79,078 shares valued at $6.605 million, and Advisors Asset Management grew its holdings 11.1% to 293,909 shares worth about $24.55 million.

Institutional investors now own 60.26% of UPS, reinforcing strong institutional participation in the stock’s rebound.

See analysts’ growth forecasts and price targets for United Parcel Service (It’s free) >>>

Is United Parcel Service Undervalued?

Under valuation assumptions, the stock is modeled using:

- Revenue Growth (CAGR): 2.6%

- Operating Margins: 10.3%

- Exit P/E Multiple: 14x

Revenue growth reflects a mature logistics network transitioning from volume reset to margin recovery rather than pursuing rapid expansion.

After generating $88.7 billion in revenue in 2025, estimates point to gradual rebuilding as enterprise, SMB, healthcare, and international mix improve.

This supports the view that future returns depend more on revenue quality, pricing power, and operational efficiency than aggressive shipment growth.

Margin expansion remains the key driver. UPS currently operates near 9% EBIT margins, while the valuation framework assumes improvement toward 10.3% as automation scales, Amazon volume exits the network, and USPS outsourcing lowers structural delivery costs.

Automation provides a structural advantage. More than 120 facilities are automated, with cost per piece in those facilities running about 28% lower than conventional buildings.

Continued automation deployment and building closures can improve productivity even if overall volumes remain modest.

Healthcare logistics also supports higher-margin mix. The global healthcare portfolio generated $11.2 billion in 2025 revenue, and continued cold-chain and complex logistics expansion positions UPS in a structurally attractive segment.

Revenue per piece growth reinforces the thesis. In the fourth quarter, U.S. revenue per piece increased 8.3% year over year, demonstrating sustained pricing discipline and mix improvement.

Based on these inputs, the valuation model estimates a target price of $142, implying about 20% total upside and roughly 6.6% annualized returns, indicating the stock appears undervalued at current levels.

Results into 2026 will likely reflect stabilization of domestic volumes, improved cost alignment following the Amazon glide-down, continued automation rollout, and expanding healthcare mix. If revenue per piece continues to outpace cost per piece, operating leverage could strengthen further.

At current levels, UPS appears undervalued, with future performance driven by margin recovery, revenue quality, and network efficiency rather than high-volume growth.

Estimate a company’s fair value instantly (Free with TIKR) >>>

Value Any Stock in Under 60 Seconds (It’s Free)

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>