Key Takeaways for Truist Financial Stock as of July 2026

- Q2 EPS hit $1.23, up 37% year over year, lifting ROTCE to 15%.

- With NII guidance cut to 1% to 2% growth for 2026, management offset the drag by raising its fee income outlook to 10% and keeping the full-year ROTCE target above 14%.

- Up 72% year over year, investment banking and trading revenue pushed fee growth well ahead of balance sheet expansion across the wholesale franchise.

- Truist exited marine and RV lending and slashed production across several consumer portfolios by 40%, pulling $7 billion to $8 billion of annual volume that CFO Mike Maguire called “significantly dilutive to our long-term ROTCE objectives.”

Truist cut NII guidance and still held its return target. See the full Q2 breakdown on TIKR for free

Truist Grew Q2 EPS 37% by Deliberately Shrinking Its Consumer Loan Book

Truist Financial (TFC) delivered Q2 2026 net income of $1,519 million, up 25% year over year, by pulling billions of dollars out of its own lending pipeline. Revenue rose 5.5% to $5,311 million, and Truist stock trades near $53 after the July 17 earnings report.

That earnings surge came from efficiency, not size. ROTCE reached 15%, a 310-basis-point improvement from Q2 2025, as EBIT margins expanded to 41.61% from 39.74% a year ago. Noninterest expense grew just 2.3% year over year, well below revenue growth, producing 320 basis points of positive operating leverage.

The mechanism: deliberate portfolio pruning. During the quarter, Truist exited marine and recreational vehicle lending entirely and slashed prime and non-prime auto originations, cutting production across these less strategic consumer portfolios by 40% versus 2025 levels. That amounts to $7 billion to $8 billion of annual volume exiting the book. CFO Mike Maguire framed the calculus on the Q2 earnings call: “Many of these portfolios are accretive to net interest income and net interest margin, but significantly dilutive to our long-term ROTCE objectives and less strategic to our client-focused business model.” The resulting drag forced a full-year NII guidance cut to 1% to 2% growth, down from 2% to 3%.

Fee income filled the gap. Noninterest income jumped 17% year over year, powered by a 72% surge in investment banking and trading revenue and 8% growth in wealth management. Management raised its full-year fee income guide to 10%, up from high single digits, and kept the full-year ROTCE target above 14%.

On the capital side, Truist repurchased $1.2 billion of stock in Q2 and confirmed $5 billion for the full year, pushing CET1 up 10 basis points to 10.9% even after returning more than 100% of earnings. CEO Bill Rogers, in his final earnings call before transitioning to Executive Chair in September as incoming CEO Mike Lyons takes over, pointed to the balance sheet repositioning as the foundation for a long-term path toward 16% to 18% ROTCE.

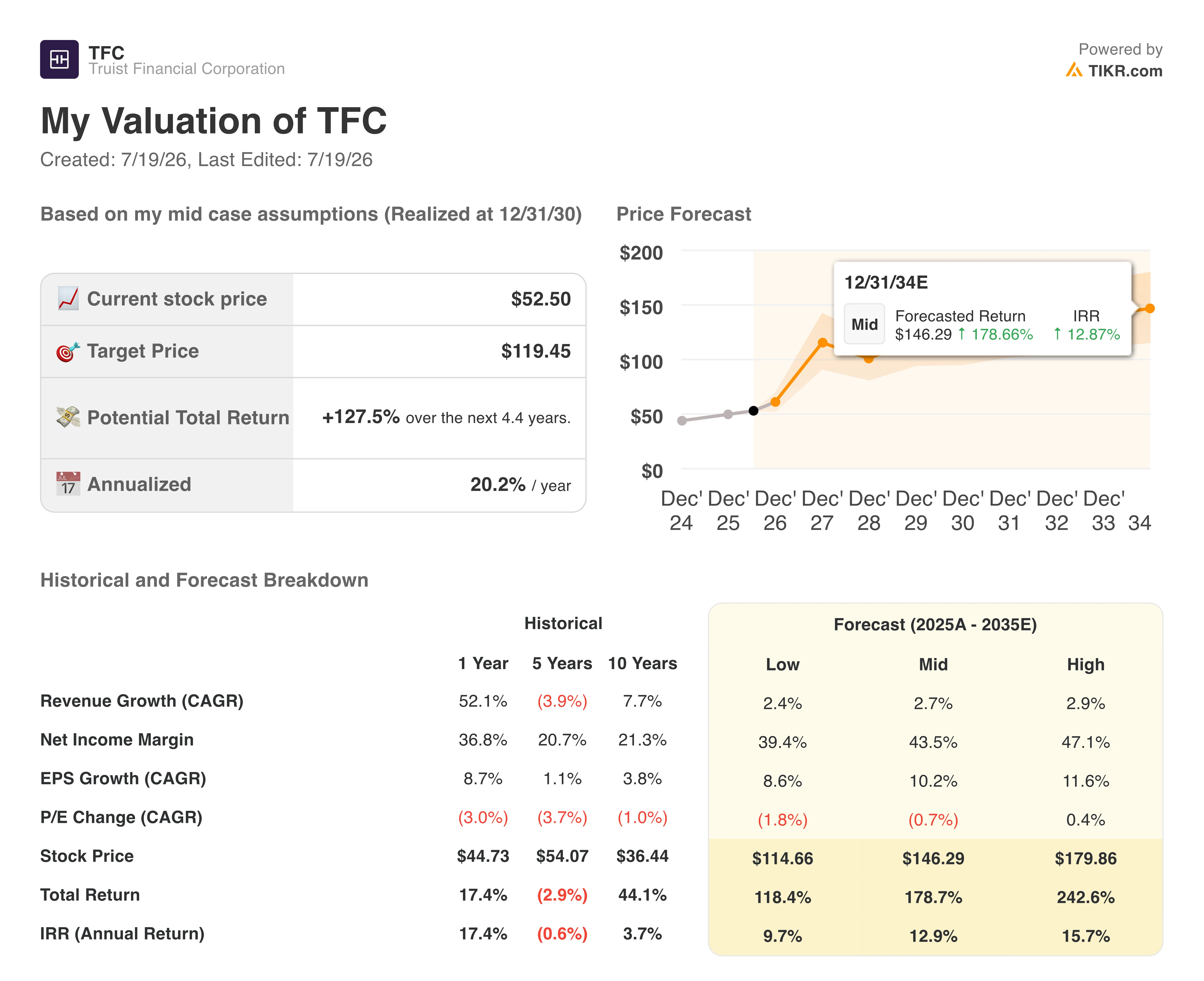

TIKR’s $119 Target Values Truist Stock at More Than Double Today’s Price

TIKR’s mid-case model values Truist Financial at $119 by December 2030, implying 128% total return from the current price of $53, or 20% annualized over 4.4 years.

A 20% annualized return would place Truist stock well above typical regional bank appreciation, pricing in a sustained inflection in the company’s earnings power rather than a one-quarter bounce.

The Q2 print supports that thesis directly: Truist already hit 15.4% ROTCE while actively shrinking its loan book, and the fee income engine that replaced those consumer assets grew 17% year over year with room to compound as investment banking and wealth management activity deepens.

Should You Invest in Truist Financial Corporation?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Truist Financial Corporation stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Truist Financial Corporation alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze TFC stock on TIKR for Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!