Key Stats for Super Micro Computer Stock

- Current Price: $28.56

- Target Price (Mid): ~$56

- Street Target: ~$33

- Potential Total Return: ~95%

- Annualized IRR: ~17% / year

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

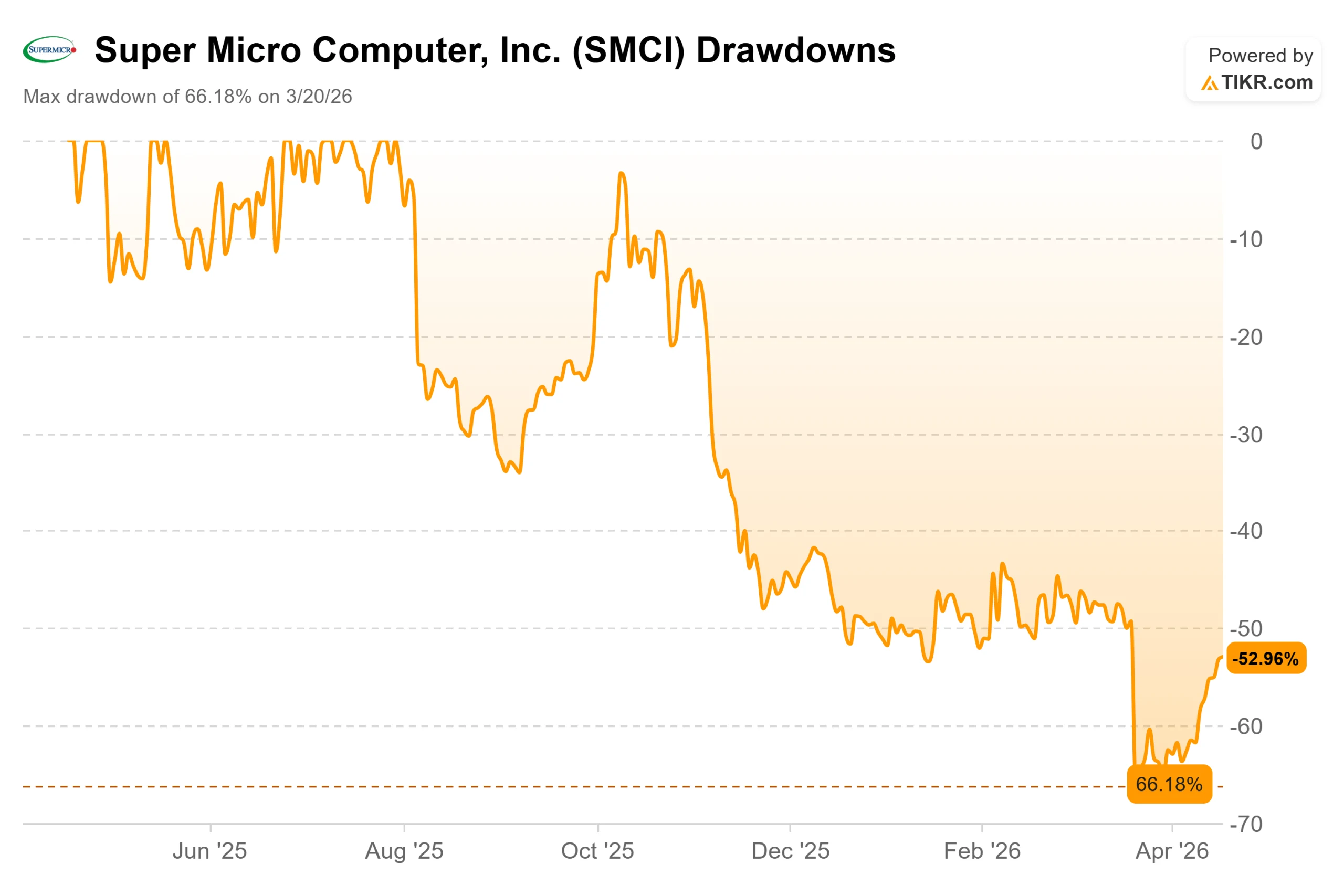

Super Micro Computer (SMCI) has fallen over 54% from its 52-week high of $62.36 to $28.56 today, and the market is split between investors who see a heavily discounted AI infrastructure leader and those who believe the governance damage is still not fully priced in.

The most dramatic single event came on March 19, 2026, when the DOJ unsealed an indictment charging co-founder Yih-Shyan “Wally” Liaw with conspiring to divert approximately $2.5 billion worth of servers containing restricted Nvidia GPUs to Chinese buyers in violation of U.S. export control laws. Liaw resigned from the board the next day.

The stock fell 33% in a single session, erasing over $6 billion in market value. He has since pleaded not guilty. Super Micro is not named as a defendant and stated that the alleged conduct “is a contravention of the Company’s policies and compliance controls.” Multiple securities fraud class-action lawsuits have since been filed.

That collapse came just six weeks after the strongest quarter in the company’s history.

On February 3, 2026, Super Micro reported Q2 FY2026 revenue of $12.68 billion, up 123% year-over-year, crushing the $10.34 billion consensus by over $2.3 billion. Non-GAAP EPS of $0.69 beat the $0.49 estimate by 41%. The stock jumped 13.78% that day. Management raised full-year FY2026 revenue guidance to at least $40 billion, calling it a “conservative estimate” on the earnings call.

Then on April 9, 2026, Supermicro launched its Gold Series enterprise server lineup, over 25 pre-configured systems for AI, compute, storage, and edge workloads shipping from U.S. warehouses within three business days. Shares surged 9.4% on the announcement.

“By shipping our Gold Series offerings directly to our customers with everything they need to run their enterprise workloads, we make our industry-leading server portfolio available to our customers even faster,” said Charles Liang, Founder, President, and CEO.

The product line targets enterprise and mid-market buyers who, unlike hyperscale data center operators, don’t have the same pricing leverage, which matters directly to the margin recovery story.

See historical and forward estimates for Super Micro Computer stock (It’s free!) >>>

Is Super Micro Computer Undervalued Today?

The numbers suggest it is cheap, but cheap for a reason.

SMCI trades at 11.56x forward earnings and 8.44x forward EV/EBITDA. For context, Dell Technologies (DELL) trades at 10.02x NTM EV/EBITDA and Hewlett Packard Enterprise (HPE) at 7.55x, per TIKR competitor data.

SMCI’s multiple is not dramatically below those of its peers. The real gap is in the revenue growth rate. Consensus on TIKR estimates SMCI revenue reaching roughly $41.5 billion in FY2026 and around $50.3 billion in FY2027, far above what either Dell or HPE is expected to deliver.

The Street’s mean price target of $33.20 implies only around 16% upside from here, reflecting the uncertainty analysts are pricing into the legal situation, not a view that the revenue story is broken.

The honest complication is gross margin. Per the Q2 FY2026 earnings report, gross margin fell to 6.3% in the December quarter, down from 11.2% a year earlier, as hyperscale customers with significant pricing leverage dominated the revenue mix. LTM gross margin sits at 8.0% per TIKR.

Management has guided toward a 14%-17% recovery range as its DCBBS product line scales. DCBBS, or Data Center Building Block Solutions, are pre-validated infrastructure packages that let customers deploy AI data centers faster and at lower cost.

On the Q2 call, CEO Liang said DCBBS contributed 4% of profits in the first half of FY2026 and is expected to reach double-digit profit contribution by the end of calendar 2026. The Gold Series launch is the first product-level move designed to prove that thesis.

The legal overlay is the wildcard. Super Micro is not a defendant in the Liaw case.

The company launched an independent investigation and appointed a new Chief Compliance Officer. But ongoing securities lawsuits and an unresolved DOJ investigation keep institutional buyers cautious and the multiple compressed.

See how Super Micro Computer performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $28.56

- Target Price (Mid): ~$56

- Potential Total Return: ~95%

- Annualized IRR: ~17% / year

See analysts’ growth forecasts and price targets for Super Micro Computer stock (It’s free!) >>>

The mid-case model uses a ~16% forward revenue CAGR through fiscal 2030, with two primary drivers: continued Blackwell-cycle server demand and DCBBS scaling as a higher-margin product category. Given SMCI’s 10-year historical revenue CAGR of 27.1%, this is a deliberately conservative assumption. The margin driver is net income recovering toward around 4%, anchored by enterprise mix improvement but kept in check by competitive pricing pressure on large infrastructure deals.

The high case reaches roughly $87, implying around 205% total return, and requires gross margins to actually hit the 14–17% management target with the legal overhang resolved at the company level. The low case at roughly $48, around 70% total return, reflects stagnant margins and a multiple that stays compressed by legal risk. The forecast period runs through 6/30/30.

Analyst sentiment on TIKR currently stands at 3 Buys, 2 Outperforms, 9 Holds, 2 Underperforms, and 2 Sells, with a mean Street target of $33.20. The TIKR model’s mid-case sits well above that, reflecting what the business could be worth if execution holds and governance risk fades.

Conclusion

Watch gross margin at Q3 FY2026 earnings on May 5, 2026. If it moves meaningfully above the 6.3% Q2 floor toward double digits, the recovery thesis has its first real data point. If it holds flat or falls further, the revenue story stops mattering as much as the profitability one.

At 11.56x forward earnings with LTM revenue of $28.1 billion and consensus expecting roughly $50 billion by FY2027, SMCI is priced for a lot of things to go wrong. Whether they actually do is what Q3 will begin to answer.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Super Micro Computer?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Super Micro Computer, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Super Micro Computer alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Super Micro Computer on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!