SoundHound AI (NASDAQ: SOUN), a player in the voice AI space, has been one of the more volatile yet compelling stocks tied to artificial intelligence. While the company’s stock is in a 50% drawdown from its late 2024 highs, shares are still up over 100% over the last 12 months. Interest in the company has spiked as investors eagerly hunt for ways to gain exposure to AI. Additionally, Soundhound has continued to capture attention through announcements about partnerships, acquisitions, and the rollout of its new Agentic AI platform.

This article dives into Wall Street analysts’ consensus for SoundHound AI between now and 2027, using financial models, Wall Street targets, and company guidance to understand where the stock might be headed. These are not predictions from TIKR, but rather a summary of analyst expectations currently available.

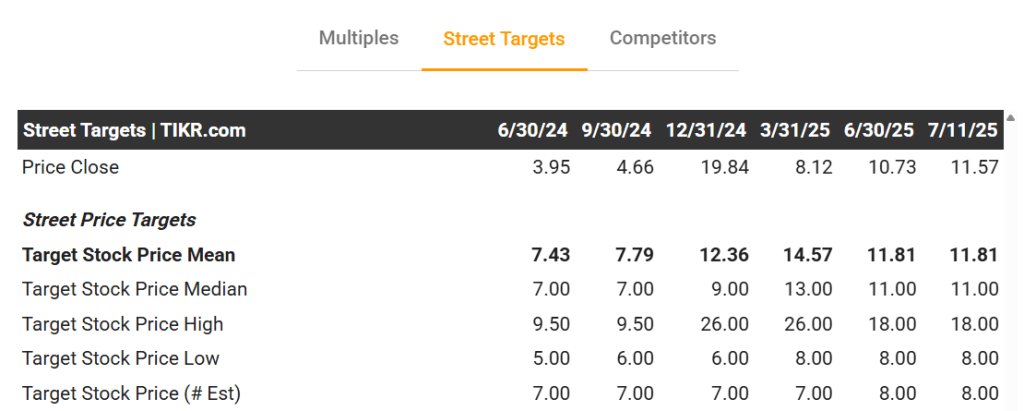

Analyst Price Targets: A Wide Range of Views

According to sell-side data tracked on TIKR, analysts expect the stock to reach an average of $12 by the end of 2024, with a high target of $26 and a low of $6. As of mid-July 2025, SoundHound AI trades around $12. The implied upside (or downside) is now minimal compared to earlier in the year when the stock was trading below $4. Back then, analyst targets suggested a 188% potential upside. As the stock rose sharply, upside potential based on target prices has narrowed.

Notably, analysts’ average price target for the end of 2025 is $14, and by mid-2026 they peg it at around $12 again. There’s little agreement beyond that, with only a single firm offering a 2027 estimate.

Revenue and Growth Outlook

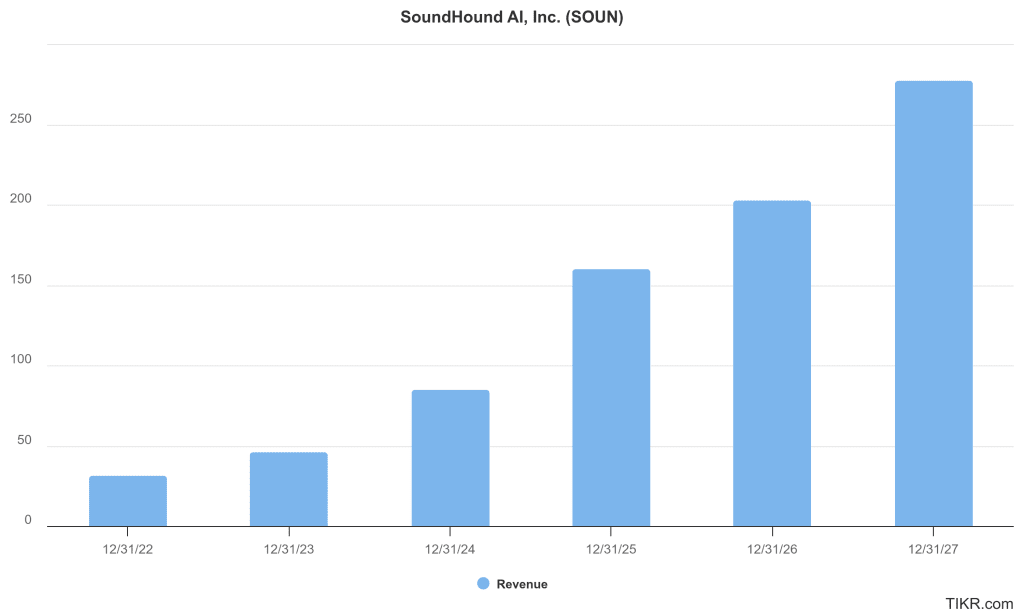

Analysts expect SoundHound AI’s revenue to rise dramatically over the next few years. After generating $102 million in the last twelve months, forecasts call for $160 million in revenue for 2025, a growth rate of roughly 88%. In 2026, revenue is projected to grow another 27% to $203 million. By 2027, consensus pegs revenue at $277 million, up 37% from the prior year.

This translates to a compound annual growth rate (CAGR) of around 36% between now and 2027, evidence of the strong secular tailwinds in AI voice technology and enterprise adoption.

However, it’s worth noting again that only one analyst has estimates for 2027, so that $277 million number might be optimistic.

Valuation Multiples Still Stretched

Despite the bullish topline growth, profitability remains elusive. In 2025, analysts expect an adjusted EBITDA loss of $25 million and an operating loss of $42 million. On a GAAP basis, EPS is projected to fall to a loss of $0.10 per share in 2025 and swing even lower in 2026.

The company currently trades at about 25x NTM revenue and over 40x TTM sales. Even by 2027, with only one analyst modeling a positive EBITDA figure, the estimated EV/EBITDA ratio balloons to over 880x, reflecting either overly optimistic projections or uncertainty about when operating leverage will kick in.

What’s Driving the Optimism?

The bull case for SoundHound AI revolves around its technological edge and accelerating commercial momentum. In Q1 2025, the company posted 151% revenue growth year-over-year, signed new partnerships with major auto OEMs and global restaurant chains, and announced new deployments of its Amelia Agentic AI platform.

CEO Keyvan Mohajer emphasized SoundHound’s strength in real-time, multi-language voice AI for noisy environments, positioning it as a differentiated player in a space where precision and latency matter. Additionally, the acquisition of Synq3 and Allset helped broaden SoundHound’s reach into restaurants and voice commerce. As of Q1 2025, the company had more than 13,000 active restaurant locations using its voice AI solutions and over 2 billion voice queries processed in a single quarter.

Queries into our voice AI engine overall continued to accelerate. We now have over 2 billion queries in less than a quarter, not much more than 2 years ago that was an annual run rate for us. All of this simply demonstrates the continued traction and momentum. And to be clear, we know we are just scratching the surface of the massive opportunity in front of us.

- Nitesh Sharan, CFO, Q1 2025 Earnings Call, May 08, 2025

The company is also debt-free and ended Q1 with $246 million in cash, which gives it a healthy financial cushion as it scales operations.

Bear Case: Profitability, Competition, and Valuation

Despite impressive growth, SoundHound remains unprofitable and burns cash. Its gross margins have dipped due to the mix of low-margin acquired contracts, and integration challenges could continue to weigh on margins for several quarters. As we already covered, analysts estimate operating losses to persist through at least 2026.

There’s also fierce competition. Industry giants like Amazon, Alphabet, and Apple are pushing forward with their own voice AI ecosystems. Smaller startups are also entering the space. And while SoundHound is clearly an innovator, its valuation suggests a high bar for execution.

Macroeconomic uncertainty is another risk. A slowdown in enterprise or auto industry spending could delay deals or force customers to cut AI investments. That said, some analysts argue that automation and AI adoption could actually accelerate during recessions as companies look for cost savings.

Outlook for 2027: What Could SoundHound Be Worth?

Looking ahead to 2027, SoundHound AI’s potential valuation hinges on whether it can convert strong revenue growth into sustainable profitability.

In a bull case, if the company reaches its projected revenue of $277 million and trades at a 20x price-to-sales multiple, its market cap would approach $5.5 billion. With approximately 380 million shares outstanding, that implies a stock price of around $14. This assumes the market still rewards SoundHound with a premium multiple, even though it would be a step down from the roughly 25x sales multiple the stock trades at today. A 20x multiple is still aggressive, especially given the company is expected to remain unprofitable through at least 2026.

In a bear case, if revenue growth disappoints or investor enthusiasm fades, a more modest 8x sales multiple could apply. That would value the company at roughly $2.2 billion, implying a stock price closer to $6 or lower.

Bottom line: Even the bullish scenario assumes continued investor optimism and significant execution from management. The stock is already pricing in a lot of future success, which leaves limited room for error.