Key Takeaways:

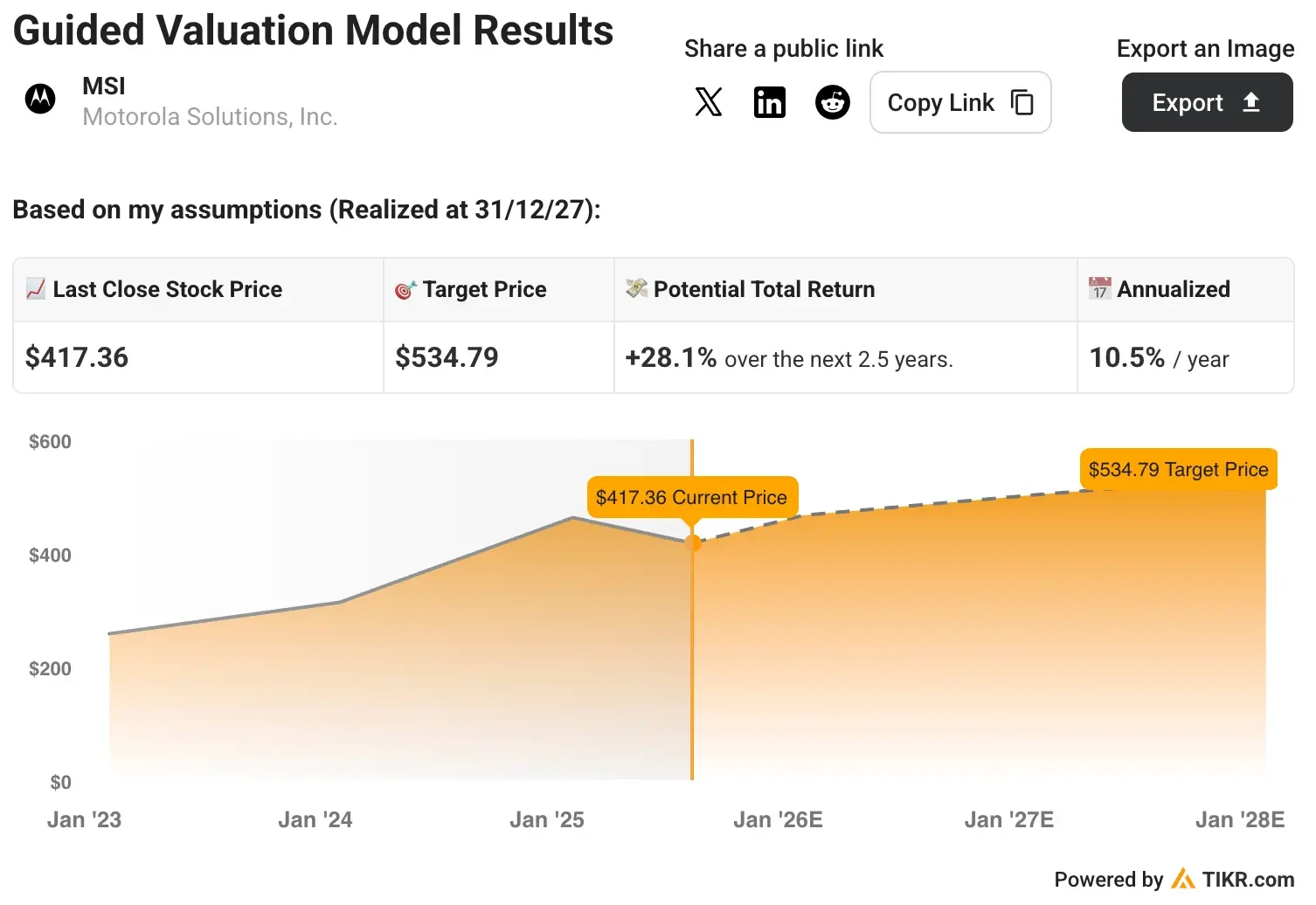

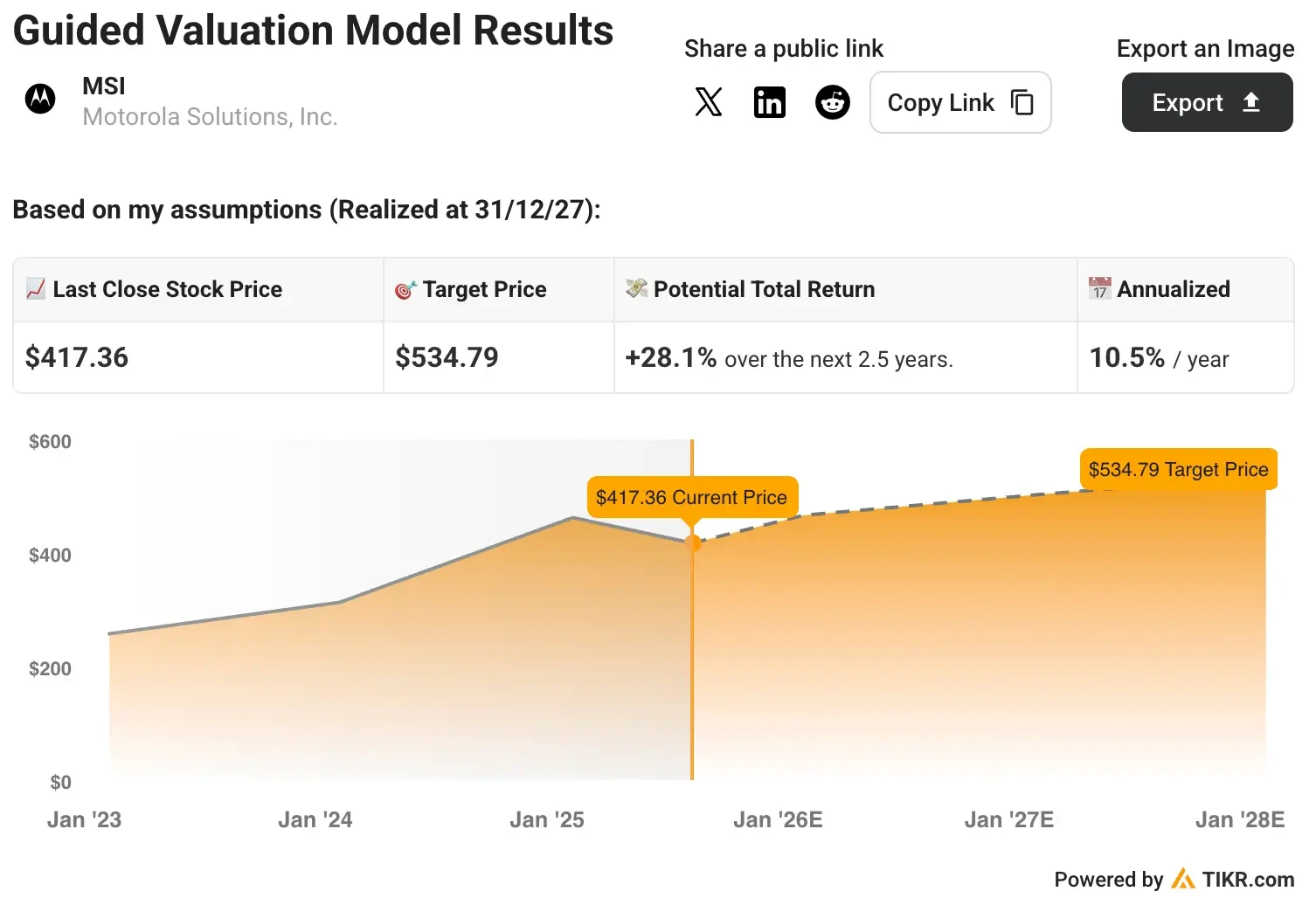

- Motorola Solutions stock could conservatively reach $535 per share by the end of 2027.

- That represents potential 28% upside from today’s price of approximately $417 per share.

- The public safety technology leader is expanding beyond traditional LMR with AI-powered solutions and strategic acquisitions.

- Unlock our Free Report: 5 undervalued compounders with upside based on Wall Street’s growth estimates that could deliver market-beating returns (Sign up for TIKR, it’s free) >>>

Motorola Solutions (MSI) stands as the global leader in mission-critical communications and public safety technology, serving over 100,000 public safety agencies and enterprises worldwide.

Over the past decade, MSI stock has returned over 550% to shareholders, outpacing the broader market returns by a significant margin.

The company has evolved from its traditional land mobile radio (LMR) roots into a comprehensive safety and security ecosystem that addresses the full spectrum of public safety needs.

With recent innovations including the converged SVX body-worn camera and speaker microphone, AI-powered Assist platform, and the pending $4.4 billion acquisition of Silvus Technologies, Motorola Solutions is positioning itself at the forefront of next-generation public safety technology while maintaining its leadership in mission-critical voice communications.

We conducted a comprehensive valuation analysis on Motorola Solutions stock to assess its investment potential through 2027.

Using reasonable assumptions based on its innovation trajectory and market expansion strategy, our model suggests MSI stock could reach $535 per share by late 2027, representing 28% upside potential.

Try TIKR’s Valuation Model today for FREE (It’s the easiest way to find undervalued stocks) >>>

What Motorola Solutions Does

Motorola Solutions operates as a leading provider of mission-critical communications and public safety technology solutions.

Its core LMR business provides secure, reliable voice communications for first responders, with approximately 70% of revenue coming from government and public safety customers and 30% from enterprise clients in healthcare, education, and critical infrastructure.

Beyond traditional radio systems, Motorola Solutions has built a comprehensive safety and security ecosystem.

The Video Security segment provides surveillance cameras, analytics, and access control solutions through the Avigilon brand. The Command Center software business provides 911 call handling, dispatch, records management, and critical incident response solutions, serving as the nerve center for public safety operations.

MSI’s recent product innovations demonstrate its evolution toward an integrated platform approach. The APX NEXT radio family represents the most significant product launch in the company’s history, combining traditional P25 secure voice with LTE broadband capabilities and generating $300 in recurring software revenue per device annually.

The newly announced SVX device combines body-worn camera and speaker microphone functionality, powered by the AI-driven Assist platform, which provides real-time translation, transcription, and intelligent video analytics.

Our Valuation Assumptions for MSI Stock

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

In our valuation, we’ll simply use analysts’ consensus estimates and break down what analysts think the stock is worth today.

Here’s what we used for MSI stock:

1. Revenue Growth: 5.7% CAGR

Motorola Solutions has demonstrated solid growth with revenue increasing 8.4% over the past year and 6.5% annually over the last five years.

Its expansion into higher-growth segments, such as video security (10-12% growth) and command center software (12% growth), as well as the pending Silvus acquisition, supports continued revenue acceleration.

2. Operating Margins: 30.1%

The company’s EBIT margins currently stand at 29.0% over the last twelve months, reflecting strong operational efficiency and pricing discipline.

The shift toward higher-margin software and services, which accounts for approximately 40% of revenue, combined with a focus on recurring revenue streams, should support margin expansion.

3. Exit P/E Multiple: 29x

Motorola Solutions currently trades at a P/E multiple of 28.3x, reflecting its premium positioning as a technology leader in a defensive end market.

Given the company’s recurring revenue model, innovation pipeline, and expansion into high-growth adjacencies, we believe this premium valuation is sustainable.

Build your own Valuation Model to value any stock (It’s free!) >>>

What the Model Says for MSI Stock

With these inputs, our valuation model estimates MSI stock could reach approximately $535 per share by the end of 2027, representing a potential 28% gain from current levels around $417.

This translates to an annualized return of approximately 10.5% over the next 2.5 years. The forecast assumes successful execution of its product innovation strategy, integration of strategic acquisitions, and continued expansion of recurring revenue streams.

The model reflects Motorola Solutions’ ability to leverage its dominant market position in mission-critical communications while expanding into adjacent high-growth markets through organic innovation and strategic acquisitions.

The model forecasts the business’s future earnings-per-share based on revenue growth and margin expansion and then applies a P/E multiple to estimate the future stock price.

This helps investors understand what financial performance is required to generate strong returns and how much upside is available if those expectations are met.

What Happens If Things Go Better or Worse?

The model enables various scenarios based on the execution of strategic initiatives and market dynamics.

Here’s the range of potential outcomes:

- Low Case: Slower product adoption with competitive pressure → 0-1% annual returns.

- Mid Case: Steady execution of innovation strategy → 5-7% annual returns.

- High Case: Accelerated market expansion and margin improvement → 9-10% annual returns.

Even the conservative scenario offers reasonable returns, reflecting Motorola Solutions’ defensive characteristics and the mission-critical nature of its solutions.

MSI’s earnings growth is likely to be driven by a combination of factors:

- Product Innovation Leadership: The APX NEXT radio family is gaining substantial traction, with 200,000 devices deployed and accounting for 25% of public safety shipments. Meanwhile, the SVX converged device represents a breakthrough in body-worn technology.

- Recurring Revenue Growth: Software and services approaching 40% of revenue, with $300 annual recurring revenue per APX NEXT device and expanding application ecosystem.

- Strategic Acquisitions: The pending $4.4 billion Silvus acquisition adds high-growth MANET technology for defense and autonomous systems, expanding the total addressable market by several billion dollars.

- Market Expansion: Growth beyond traditional LMR into video security, command center software, and emerging technologies like drone and counter-drone solutions.

- Operational Excellence: Strong margin profile with continued focus on operational efficiency and premium pricing for mission-critical solutions.

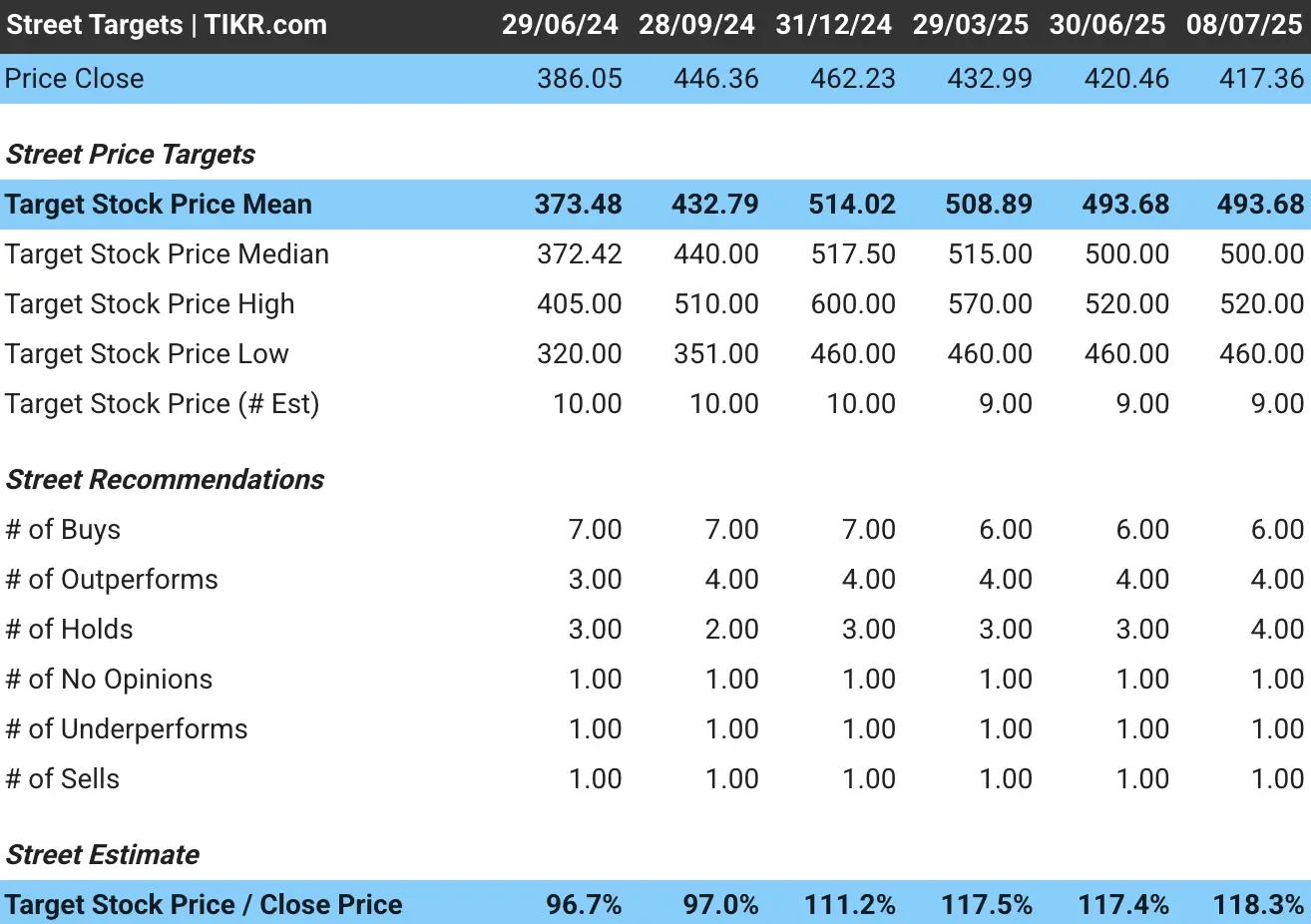

How Wall Street Sees Motorola Solutions Stock

Wall Street analysts maintain a positive outlook on Motorola Solutions, with an average price target of approximately $494 per share, implying about 18% upside from current levels.

Our model suggests additional upside potential based on the successful execution of the company’s strategic initiatives.

See analysts’ growth forecasts and price target for Motorola Solutions stock (It’s free!) >>>

Risks to Consider

Despite the bullish outlook, investors should be aware of several risks that could impact MSI’s growth trajectory:

- Integration Execution: Successfully integrating the Silvus acquisition while maintaining growth momentum and cultural alignment presents operational challenges.

- Competitive Pressure: New entrants in body-worn cameras and video security could pressure market share and pricing, particularly in enterprise segments.

- Technology Disruption: Rapid changes in communication technology or the emergence of new competitive solutions could impact the company’s market leadership position.

- Customer Budget Constraints: Economic pressures on state and local government budgets could affect capital spending on public safety technology.

- Regulatory Changes: Changes in spectrum allocation, privacy regulations, or government procurement policies could impact business operations.

TIKR Takeaway

Motorola Solutions presents a compelling growth story as it leverages its leadership in mission-critical communications to expand into adjacent technology markets.

MSI’s defensive end market positioning, innovation pipeline, and strategic acquisitions position it well for sustained growth in the evolving public safety technology landscape.

The 28% upside potential over the next 2.5 years, combined with strong competitive moats and an expanding recurring revenue base, makes Motorola Solutions attractive for investors seeking exposure to public safety technology trends while benefiting from the stability of mission-critical communications.

Success will depend on management’s ability to execute product innovations, successfully integrate strategic acquisitions, and maintain competitive advantages in an increasingly technology-driven public safety environment.

Is MSI stock a buy over the next 24 months? Use TIKR’s Valuation Model alongside analysts’ growth forecasts and price targets to see if it is undervalued today.

Value any stock with TIKR’s Valuation Models (It’s free!) >>>

Wall Street Analysts Are Bullish on These 5 Undervalued Compounders With Market-Beating Potential

TIKR just released a new free report on 5 compounders that appear undervalued, have beaten the market in the past, and could continue to outperform on a 1-5 year timeline based on analysts’ estimates.

Inside, you’ll get a breakdown of 5 high-quality businesses with:

- Strong revenue growth and durable competitive advantages

- Attractive valuations based on forward earnings and expected earnings growth

- Long-term upside potential backed by analyst forecasts and TIKR’s valuation models

These are the kinds of stocks that can deliver massive long-term returns, especially if you catch them while they’re still trading at a discount.

Whether you’re a long-term investor or just looking for great businesses trading below fair value, this report will help you zero in on high-upside opportunities.

Click here to sign up for TIKR and get our full report on 5 undervalued compounders completely free.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!