Key Takeaways:

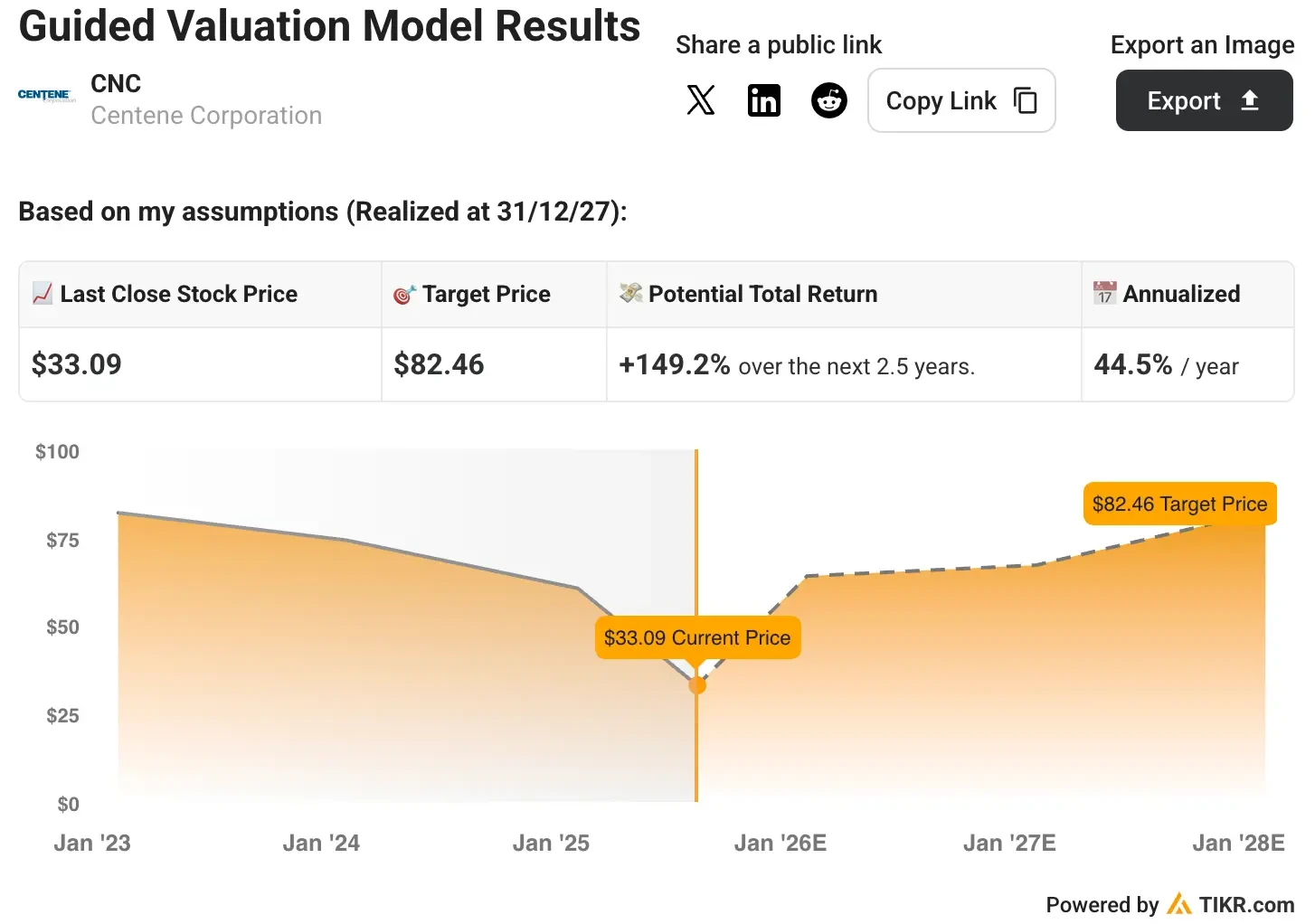

- Centene stock could reach $82.46 per share by the end of 2027, based on our valuation assumptions.

- That implies a 149.2% total return from today’s price of $33.09 per share, with an annualized return of 44.5% over the next 2.5 years.

- Centene operates as a diversified managed care organization serving government-sponsored healthcare programs, with leading positions in Medicaid, Medicare Advantage, and Health Insurance Marketplace segments.

Centene (CNC) is a multi-national healthcare enterprise that provides managed care services to government-sponsored healthcare programs, focusing on under-insured and uninsured individuals.

It benefits from long-term demographic trends driving enrollment growth, improving Medicaid rate negotiations following redetermination acuity shifts, and a path to Medicare Advantage breakeven by 2027.

The stock is down over 50% in the past year, which could present an opportunity today. Analysts have an average price target of $66/share for the stock today, meaning they see 100% upside from the stock’s current price of $33/share.

With $42.5 billion in quarterly revenue, strong membership growth across segments, and multiple opportunities for margin expansion, CNC stock remains well-positioned as a compelling healthcare services play in the government-sponsored market.

Here’s why CNC stock could return over 44% annually through 2027 and potentially continue its strong performance through 2030.

Try TIKR’s Valuation Model today for FREE (It’s the easiest way to find undervalued stocks) >>>

What the Model Says for CNC Stock

We analyzed Centene’s potential using valuation assumptions based on its diversified portfolio performance and management guidance.

Based on assumptions of 4.4% annual revenue growth, 1.7% operating margins, and moderate multiple expansion, the model estimates Centene stock could rise from $33.09/share to $82.46/share.

That represents a 149.2% total return and a 44.5% annualized return over the next 2.5 years.

Value CNC with TIKR’s Valuation Model today for FREE (Find undervalued stocks fast) >>>

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for Centene stock:

1. Revenue Growth: 4.4%

Centene delivered strong Q1 results with $42.5 billion in premium revenue and added $6 billion to full-year guidance, driven by better-than-expected membership retention.

We used a conservative 4.4% forecast reflecting a mature market position while accounting for continued government program expansion.

2. Operating Margins: 1.7%

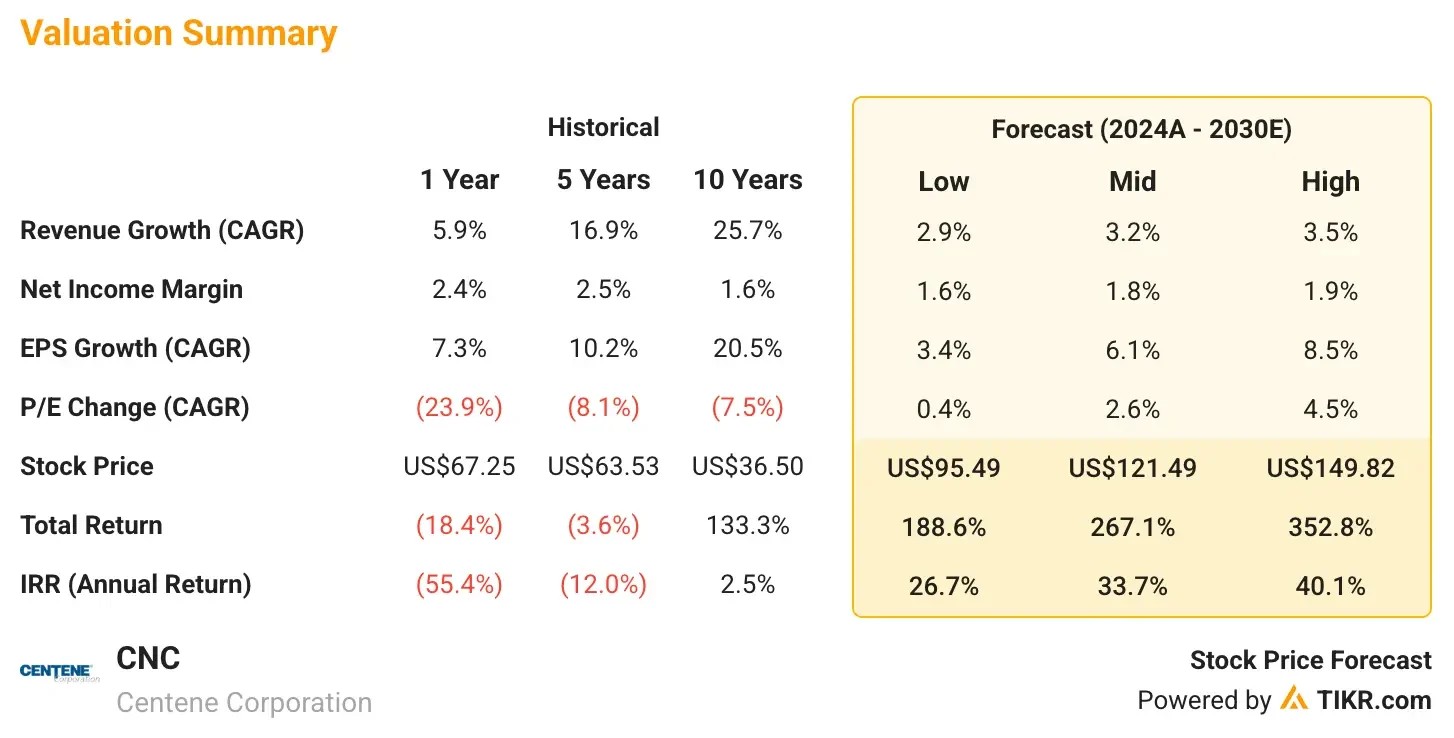

Centene’s EBIT margins have averaged around 2.6% over the last three years.

The company has demonstrated disciplined expense management with adjusted SG&A ratios improving to 7.9% from 8.7% year-over-year.

We project modest margin expansion as Medicaid rates better align with member acuity and Medicare Advantage approaches breakeven by 2027.

3. Exit P/E Multiple: 10.1x

CNC stock currently trades at a forward P/E of 10.1x, which is lower than its average three-year multiple of 11x.

Centene trades at depressed multiples relative to its diversified government healthcare franchise and embedded earnings potential.

We have maintained a conservative earnings estimate, despite Centene’s margin recovery trajectory and stable cash flows.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

TIKR’s valuation tool allows investors to test a wide range of outcomes based on how CNC stock performs through 2030 under different scenarios (these are estimates, not guaranteed returns):

- Low Case: Slower policy environment and margin pressure → 27% annual returns.

- Mid Case: Solid execution on rate negotiations and Medicare turnaround → 34% annual returns.

- High Case: Accelerated margin expansion and market share gains → 40% annual returns.

Even in the conservative case, Centene offers exceptional potential returns, while the upside scenario could deliver outsized gains if operational improvements accelerate.

See analysts’ growth forecasts and price targets for any stock (It’s free!) >>>

TIKR Takeaway

Centene represents a compelling turnaround story in government-sponsored healthcare, with significant embedded earnings growth as margins recover across its diversified portfolio.

With an estimated 149.2% upside by the end of 2027 and annual returns exceeding 44%, Centene stands out as an undervalued healthcare services play benefiting from demographic tailwinds, improving rate adequacy, and operational leverage.

This healthcare stock is best suited for investors seeking exposure to government healthcare programs, companies with proven ability to navigate complex regulatory environments, and turnaround situations with multiple margin expansion catalysts.

The combination of strong membership growth, improving fundamentals, and conservative valuation makes Centene an attractive consideration for value-oriented healthcare portfolios positioned for long-term outperformance.

Is CNC stock worth buying today? Use TIKR’s Valuation Model and analyst forecasts to see if it looks undervalued.

Value any stock with TIKR’s Valuation Model (It’s free!) >>>

Wall Street Analysts Are Bullish on These 5 Undervalued Compounders With Market-Beating Potential

TIKR just released a new free report on 5 compounders that appear undervalued, have beaten the market in the past, and could continue to outperform on a 1-5 year timeline based on analysts’ estimates.

Inside, you’ll get a breakdown of 5 high-quality businesses with:

- Strong revenue growth and durable competitive advantages

- Attractive valuations based on forward earnings and expected earnings growth

- Long-term upside potential backed by analyst forecasts and TIKR’s valuation models

These are the kinds of stocks that can deliver massive long-term returns, especially if you catch them while they’re still trading at a discount.

Whether you’re a long-term investor or just looking for great businesses trading below fair value, this report will help you zero in on high-upside opportunities.

Click here to sign up for TIKR and get our full report on 5 undervalued compounders completely free.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!