Key Takeaways:

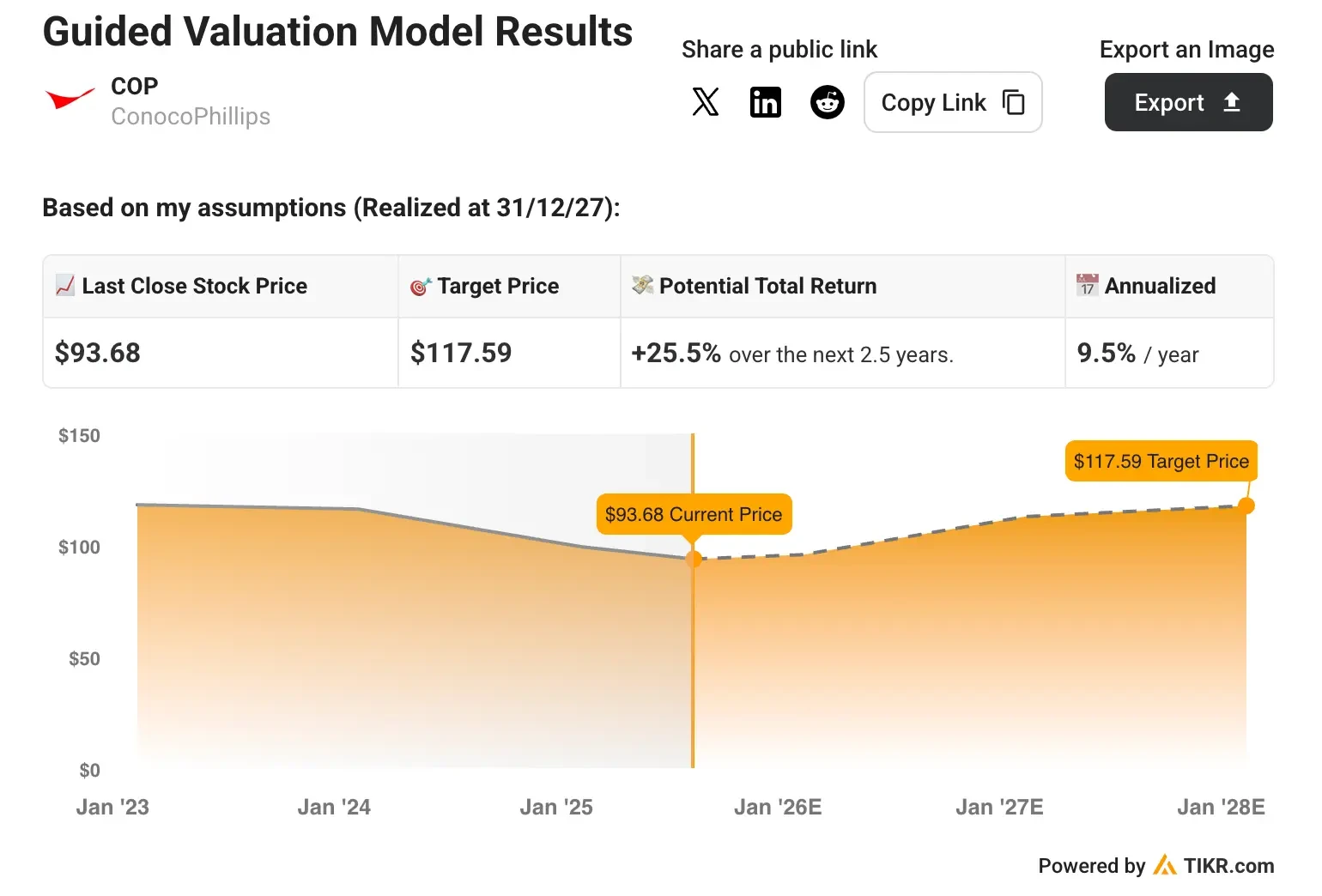

- ConocoPhillips stock could conservatively reach $118 per share by the end of 2027.

- That represents a potential 26% upside from today’s price of approximately $94 per share.

- The oil giant is positioned as a leader among “inventory haves” with decades of low-cost supply below $40/barrel.

- Unlock our Free Report: 5 stock screeners inspired by top investors like Warren Buffett to help you find high-upside stock ideas (Sign up for TIKR, it’s free) >>>

ConocoPhillips (COP) stands as one of the world’s largest independent oil and gas companies, operating a diversified portfolio of assets across the United States and internationally.

It has built a reputation for disciplined capital allocation, operational excellence, and maintaining one of the industry’s strongest balance sheets through commodity cycles.

Despite facing near-term headwinds from volatile oil prices and softer demand outlooks, ConocoPhillips is demonstrating the resilience that defines its business model.

The oil and gas giant recently reduced capital spending by $500 million while maintaining production guidance, illustrating its ability to deliver operational efficiency improvements even in challenging environments.

We conducted a comprehensive valuation analysis on ConocoPhillips stock to assess its investment potential through 2027.

Using reasonable assumptions based on the company’s low-cost inventory position and proven cycle management capabilities, our model suggests ConocoPhillips stock could reach $118 per share by late 2027, representing a 26% upside potential.

Try TIKR’s Valuation Model today for FREE (It’s the easiest way to find undervalued stocks) >>>

What ConocoPhillips Does

ConocoPhillips operates as a leading independent exploration and production company with a global portfolio of oil and natural gas assets.

Its operations span key basins in the Lower 48 United States, including the Permian, Eagle Ford, and Bakken, where it maintains significant acreage positions and operates as a leading producer.

Internationally, ConocoPhillips has strategic assets in Alaska, Canada, Norway, and through its APLNG joint venture in Australia. The company’s Alaska operations encompass both legacy fields and major growth projects, such as the Willow development, which represents one of the largest new oil developments in the United States.

ConocoPhillips has strategically positioned itself with what management calls a “deep, durable and diverse” portfolio featuring decades of inventory below its $40 per barrel cost of supply threshold.

This low-cost inventory base provides operational flexibility and competitive advantages, particularly during challenging commodity price environments when higher-cost producers face pressure.

The energy heavyweight’s business model emphasizes consistent shareholder returns through its commitment to returning approximately 45% of cash flow from operations to shareholders, supported by a disciplined capital allocation framework that has been battle-tested through multiple commodity cycles.

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

In our valuation, we’ll simply use analysts’ consensus estimates and break down what analysts think the stock is worth today.

Here’s what we used for COP stock:

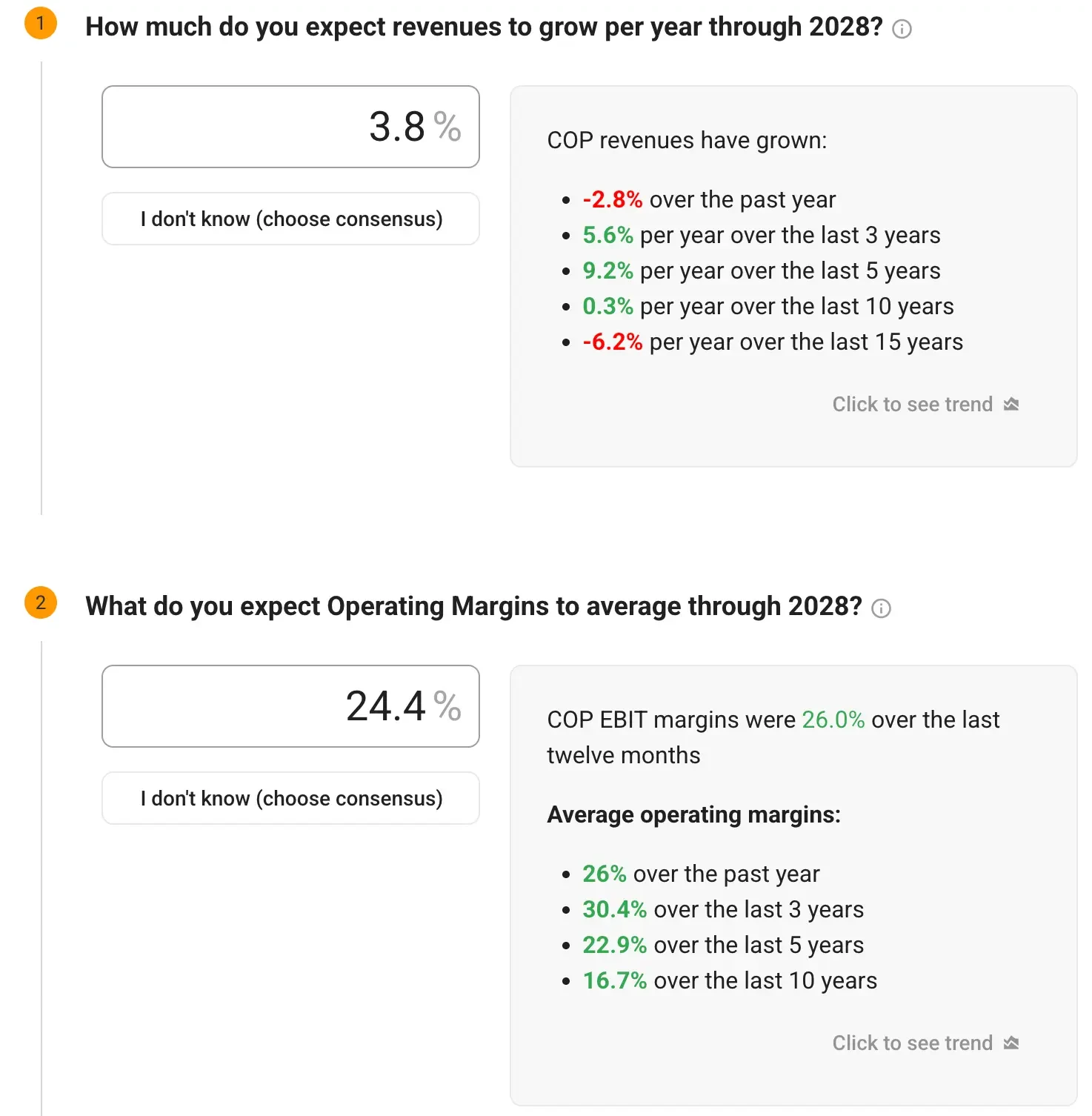

1. Revenue Growth: 3.8% CAGR

ConocoPhillips has experienced a revenue decline of 2.8% over the past year, primarily due to lower commodity prices. However, it has demonstrated annual revenue growth of 9.2% over the last five years.

Our conservative growth assumption reflects the cyclical nature of oil prices while accounting for the ability to optimize production from its low-cost inventory base.

2. Operating Margins: 24.4%

The company’s EBIT margins currently stand at 26.0% over the last twelve months, reflecting strong operational efficiency.

ConocoPhillips continues to drive cost reductions and capital efficiency improvements, as evidenced by recent guidance updates that reduced both capital spending and operating costs while maintaining production targets.

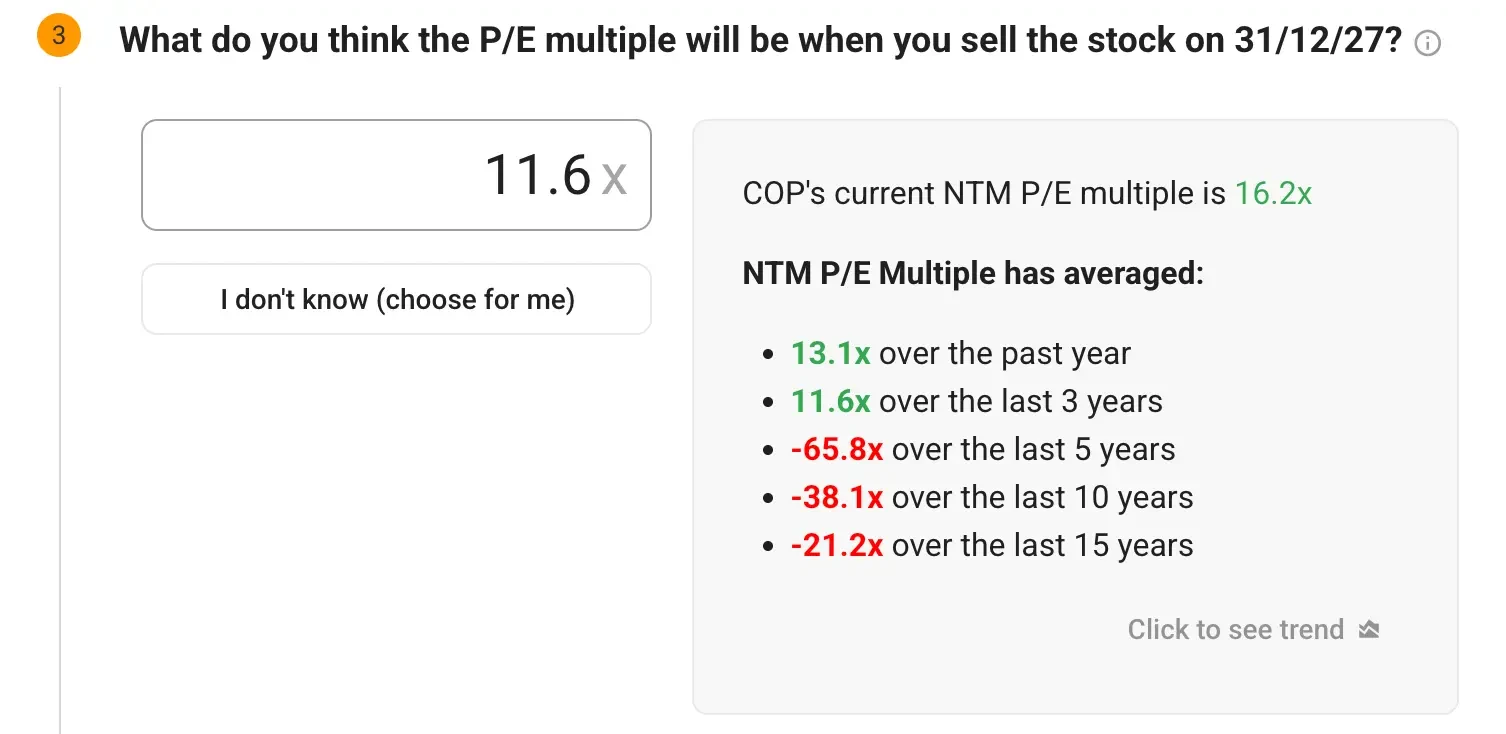

3. Exit P/E Multiple: 23.3x

ConocoPhillips currently trades at a P/E multiple of 16.2x, but energy companies typically see multiple compressions during commodity cycles.

We assume a more conservative exit multiple that reflects the cyclical nature of the business while recognizing its superior asset quality and financial discipline.

Build your own Valuation Model to value any stock (It’s free!) >>>

What the Model Says for COP Stock

With these inputs, the valuation model estimates that COP stock could reach approximately $118/share by the end of 2027.

Value ConocoPhillips with TIKR’s Valuation Model today for FREE (Find undervalued stocks fast) >>>

This translates to an annualized return of approximately 9.5% over the next 2.5 years. The forecast assumes ConocoPhillips successfully executes its operational efficiency programs, maintains its disciplined capital allocation framework, and benefits from its low-cost inventory position as the market distinguishes between inventory “haves and have-nots.”

The model forecasts the business’s future earnings-per-share based on revenue growth and margin expansion and then applies a P/E multiple to estimate the future stock price.

This helps investors understand what financial performance is required to generate strong returns and how much upside is available if those expectations are met.

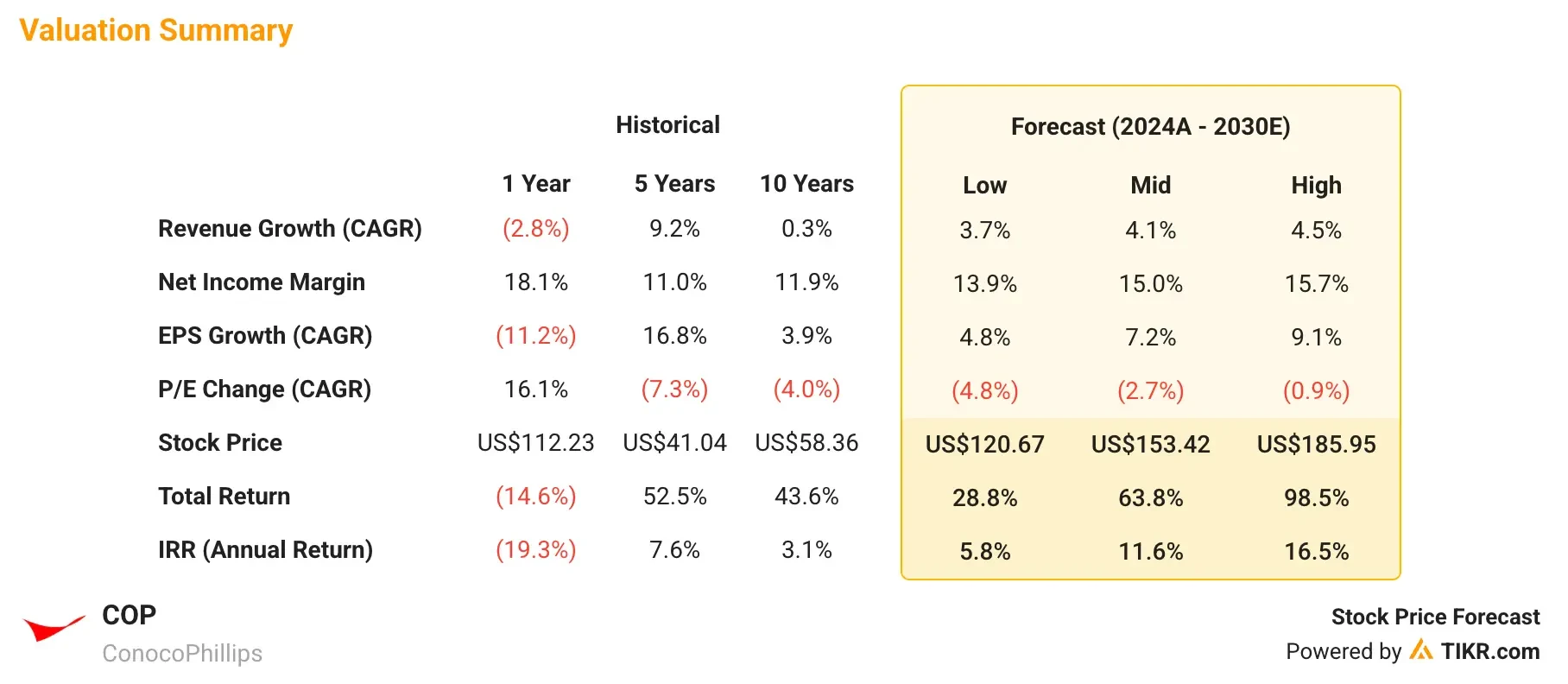

What Happens If Things Go Better or Worse?

The model enables various scenarios based on commodity price environments and operational execution.

Here’s the range of potential outcomes:

- Low Case: Prolonged low oil prices with operational challenges → 6-8% annual returns.

- Mid Case: Steady execution with moderate commodity recovery → 9-12% annual returns.

- High Case: Strong commodity environment with operational excellence → 14-17% annual returns.

Even the conservative scenario offers attractive returns, reflecting ConocoPhillips’ defensive characteristics and a proven ability to generate cash flow at commodity prices well below current levels.

COP’s earnings growth is likely to be driven by a combination of factors:

- Low-Cost Inventory Advantage: With decades of sub-$40 cost of supply inventory, COP can maintain profitability and returns even in challenging price environments when competitors face pressure.

- Major Project Development: The Willow project in Alaska and LNG investments are nearing completion, which is expected to drive significant free cash flow growth as capital requirements decline and production increases.

- Operational Excellence: Continued efficiency improvements, including the successful Marathon Oil integration that is ahead of schedule and delivering over $500 million in capital synergies.

- Capital Discipline: COP’s proven ability to adjust capital spending while maintaining production, as demonstrated by the recent $500 million capital reduction with unchanged production guidance.

- Shareholder Returns: Commitment to returning approximately 45% of cash flow to shareholders through dividends and buybacks, providing attractive income and capital return potential.

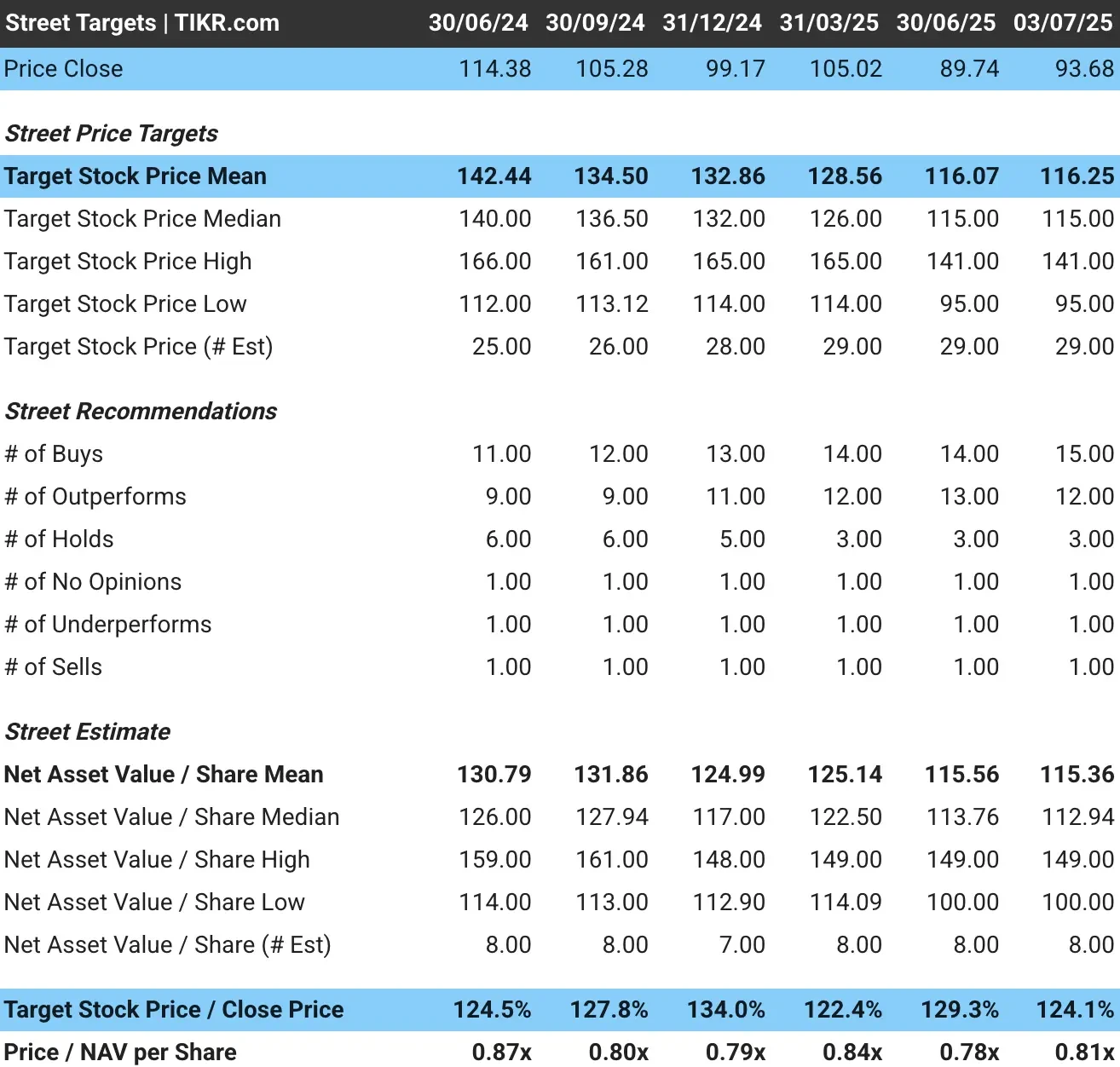

How Wall Street Sees COP Stock

Wall Street analysts maintain a positive outlook on COP stock, with an average price target of approximately $116 per share, implying about 24% upside from current levels.

Our model aligns well with Street expectations while reflecting the potential for commodity price recovery and operational execution.

See analysts’ growth forecasts and price target for ConocoPhillips stock (It’s free!) >>>

Risks to Consider

Despite the bullish outlook, investors should be aware of several risks that could impact ConocoPhillips’ growth trajectory:

- Commodity Price Volatility: Sustained low oil prices below $50 could pressure returns and force additional capital allocation adjustments, though its low-cost structure provides relative resilience.

- Demand Uncertainty: Slower global economic growth and evolving energy transition policies could impact long-term oil demand, affecting asset values and investment returns.

- Operational Execution: The successful completion of major projects, such as Willow, and the integration of the Marathon Oil acquisition are critical to achieving projected cash flow growth.

- ESG and Regulatory Pressures: The increasing focus on environmental regulations and sustainability by investors could impact operational flexibility and access to capital.

- Geopolitical Risks: International operations expose the company to political and regulatory changes in key jurisdictions, such as Norway and the Middle East.

TIKR Takeaway

ConocoPhillips presents a compelling value proposition for investors seeking exposure to energy markets with a focus on capital discipline and shareholder returns.

Its low-cost inventory base, operational flexibility, and proven cycle management capabilities position it well to navigate volatile commodity environments.

The 26% upside potential over the next 2.5 years, combined with substantial dividend income and share buyback programs, makes ConocoPhillips attractive for investors seeking both income and capital appreciation in the energy sector.

Is COP stock a buy over the next 24 months? Use TIKR’s Valuation Model alongside analysts’ growth forecasts and price targets to see if it is undervalued today.

Value any stock with TIKR’s Valuation Models (It’s free!) >>>

Want to Invest Like Warren Buffett, Joel Greenblatt, or Peter Lynch?

TIKR just published a special report breaking down 5 powerful stock screeners inspired by the exact strategies used by the world’s greatest investors.

In this report, you’ll discover:

- A Buffett-style screener for finding wide-moat compounders at fair prices

- Joel Greenblatt’s formula for high-return, low-risk stocks

- A Peter Lynch-inspired tool to surface fast-growing small caps before Wall Street catches on

Each screener is fully customizable on TIKR, so you can apply legendary investing strategies instantly. Whether you’re looking for long-term compounders or overlooked value plays, these screeners will save you hours and sharpen your edge.

This is your shortcut to proven investing frameworks, backed by real performance data.

Click here to sign up for TIKR and get this full report now, completely free.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!