Key Takeaways:

- Analysts expect JPMorgan to report revenue of $44 billion in Q2, down 12.26% year over year.

- CEO Jamie Dimon estimates a 50-50 odds of recession while maintaining the bank’s position as a “source of strength” in turbulent times.

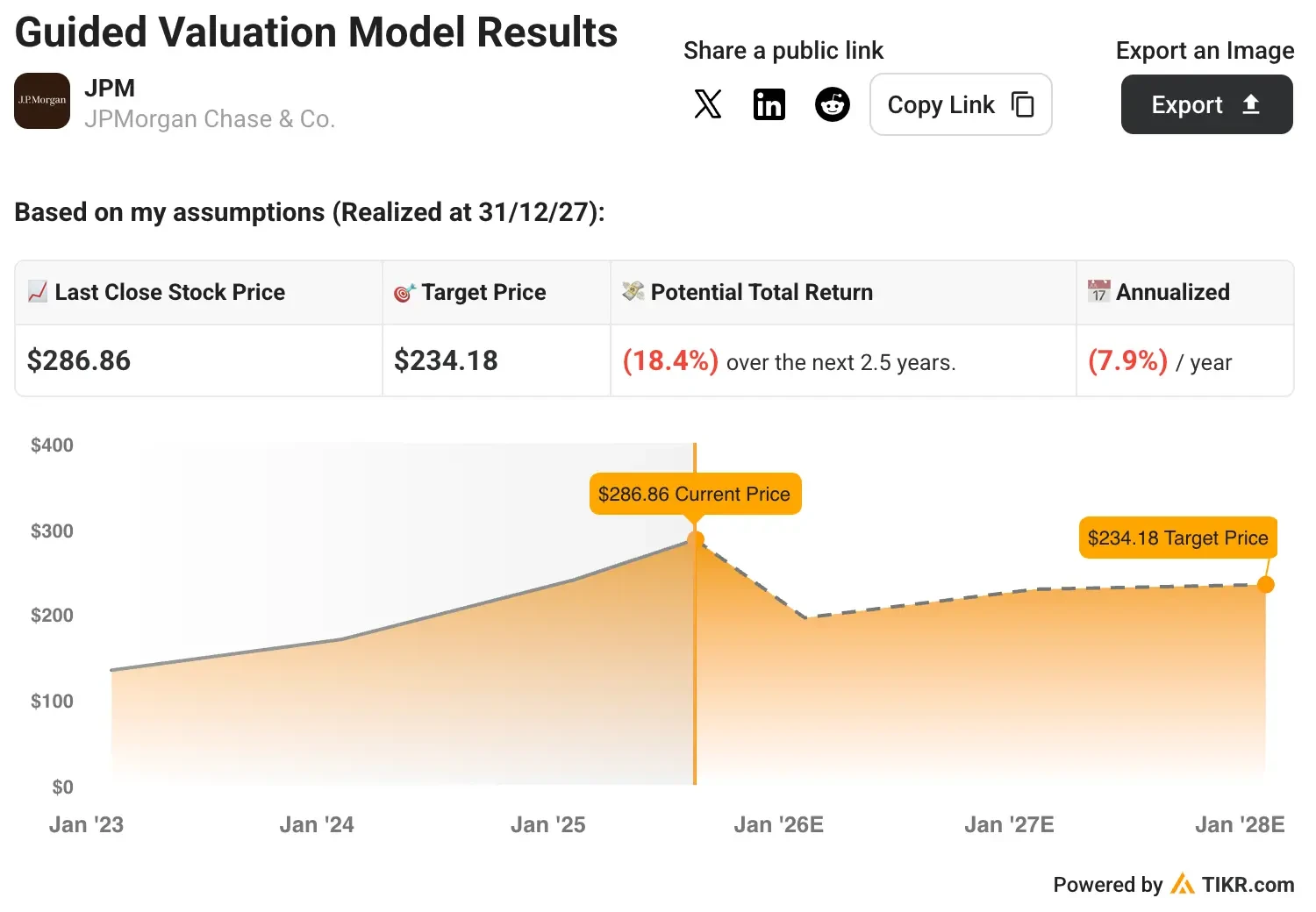

- Our valuation model projects JPM stock to decline 18.4% over the next 2.5 years, reflecting concerns about economic headwinds and credit normalization.

In Q1 of 2025, JPMorgan Chase (JPM) reported net income of $14.6 billion and earnings per share of $5.07 on revenue of $46 billion.

Analysts covering JPM stock expect revenue to decline by 12.3% year over year to $44.04 billion in Q2 of 2025, while earnings are forecast to drop by 26.7% to $4.48 per share.

The banking giant has maintained industry-leading profitability with ROTCE above 17% for seven consecutive years, though management warns of elevated economic uncertainty ahead.

The banking giant has beaten consensus revenue and earnings estimates in each of the last five quarters.

See analysts’ growth forecasts and price targets for any stock (It’s free!) >>>

A Challenging Macro Environment for JPM Stock

JPMorgan has demonstrated exceptional resilience through multiple economic cycles, positioning itself as a fortress during periods of uncertainty.

JPMorgan’s excess capital position will be a key stability factor, as management maintains $60 billion in excess capital with a CET1 ratio of 15.4%. This positions the bank to weather various economic scenarios while continuing to serve clients and support markets during turbulent periods.

The company’s $18 billion annual technology investment exemplifies its commitment to operational excellence and efficiency. JPMorgan’s approach of investing relentlessly in people, technology, and process improvements has proven successful in maintaining market-leading returns across business cycles.

JPMorgan’s regulatory reform opportunity, while currently uncertain, targets significant capital efficiency improvements. CEO Jamie Dimon expects potential changes to SLR, LCR, and Basel III implementation could free up “hundreds of billions of dollars” for lending while maintaining safety and soundness.

The bank’s credit loss allowance increase of $973 million, bringing total reserves to $27.6 billion, reflects prudent risk management rather than actual credit deterioration.

Management increased the weighted average unemployment rate in their economic scenarios to 5.8% from 5.5%, demonstrating proactive reserve building during uncertain times.

With projected stable net interest income around $90 billion and disciplined expense management targeting $95 billion, JPM stock maintains flexibility for strategic investments while returning excess capital to shareholders through dividends and buybacks, supporting long-term value creation.

Build your own Valuation Model to value any stock (It’s free!) >>>

Is JPM Stock a Buy Before Its Q2 Earnings?

Our valuation model estimates JPMorgan to increase revenue by 1.5% year over year through 2028, while maintaining an operating margin of 44.5%.

Moreover, the model estimates JPM stock to maintain a forward price-to-earnings multiple of 10x, which is lower than the current multiple of 15.7x but in line with its long-term average.

We can see that the valuation model projects JPM stock to decline 18.4% over the next 2.5 years, indicating an annual return of negative 7.9%. This suggests potential downside risks given current economic uncertainties.

Notably, JPMorgan stock has returned 35% in the last year and more than 340% in the past decade, easily outpacing the broader market returns.

Value JPM with TIKR’s Valuation Model today for FREE (Find undervalued stocks fast) >>>

Wall Street Analysts Are Bullish on These 5 Undervalued Compounders With Market-Beating Potential

TIKR just released a new free report on 5 compounders that appear undervalued, have beaten the market in the past, and could continue to outperform on a 1-5 year timeline based on analysts’ estimates.

Inside, you’ll get a breakdown of 5 high-quality businesses with:

- Strong revenue growth and durable competitive advantages

- Attractive valuations based on forward earnings and expected earnings growth

- Long-term upside potential backed by analyst forecasts and TIKR’s valuation models

These are the kinds of stocks that can deliver massive long-term returns, especially if you catch them while they’re still trading at a discount.

Whether you’re a long-term investor or just looking for great businesses trading below fair value, this report will help you zero in on high-upside opportunities.

Click here to sign up for TIKR and get our full report on 5 undervalued compounders completely free.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!