Key Takeaways:

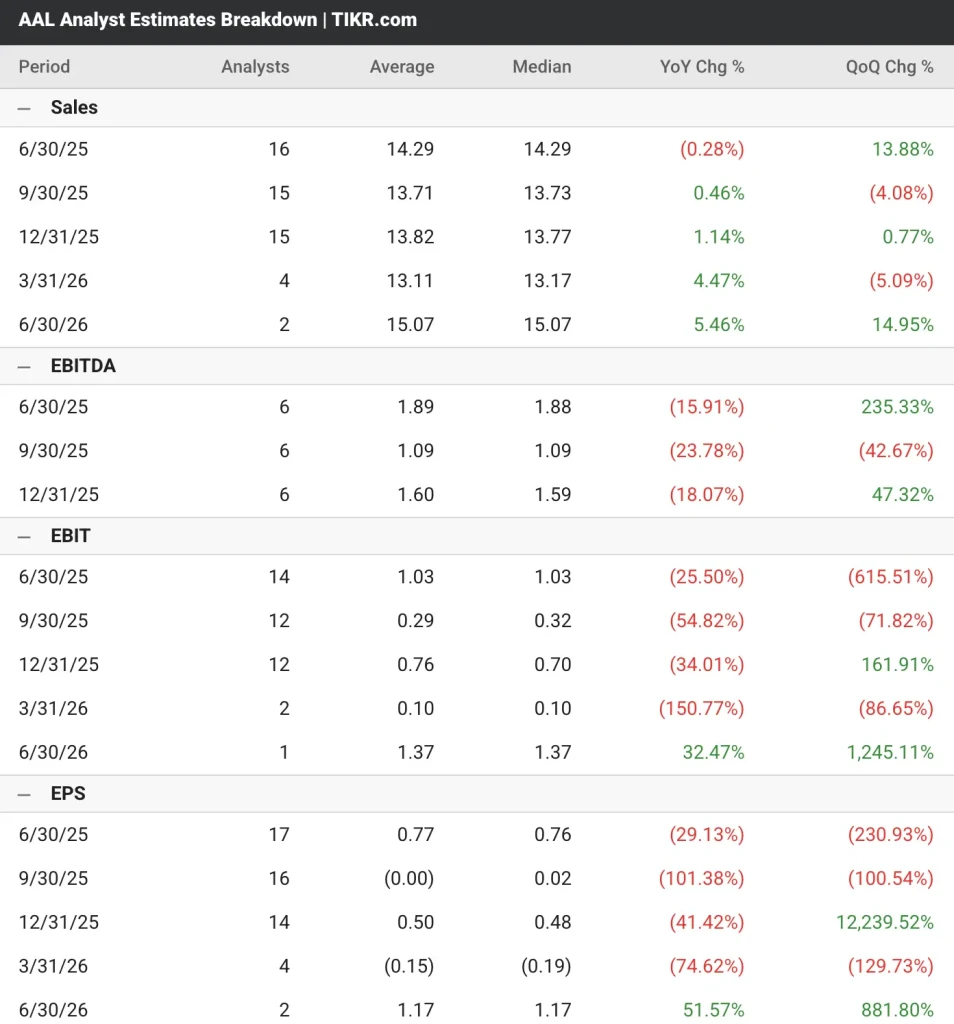

- Analysts expect American Airlines to report revenue of $14.29 billion, down 0.28% year over year.

- The airline withdrew full-year guidance due to domestic demand weakness but expects to remain profitable and generate positive free cash flow if trends stabilize.

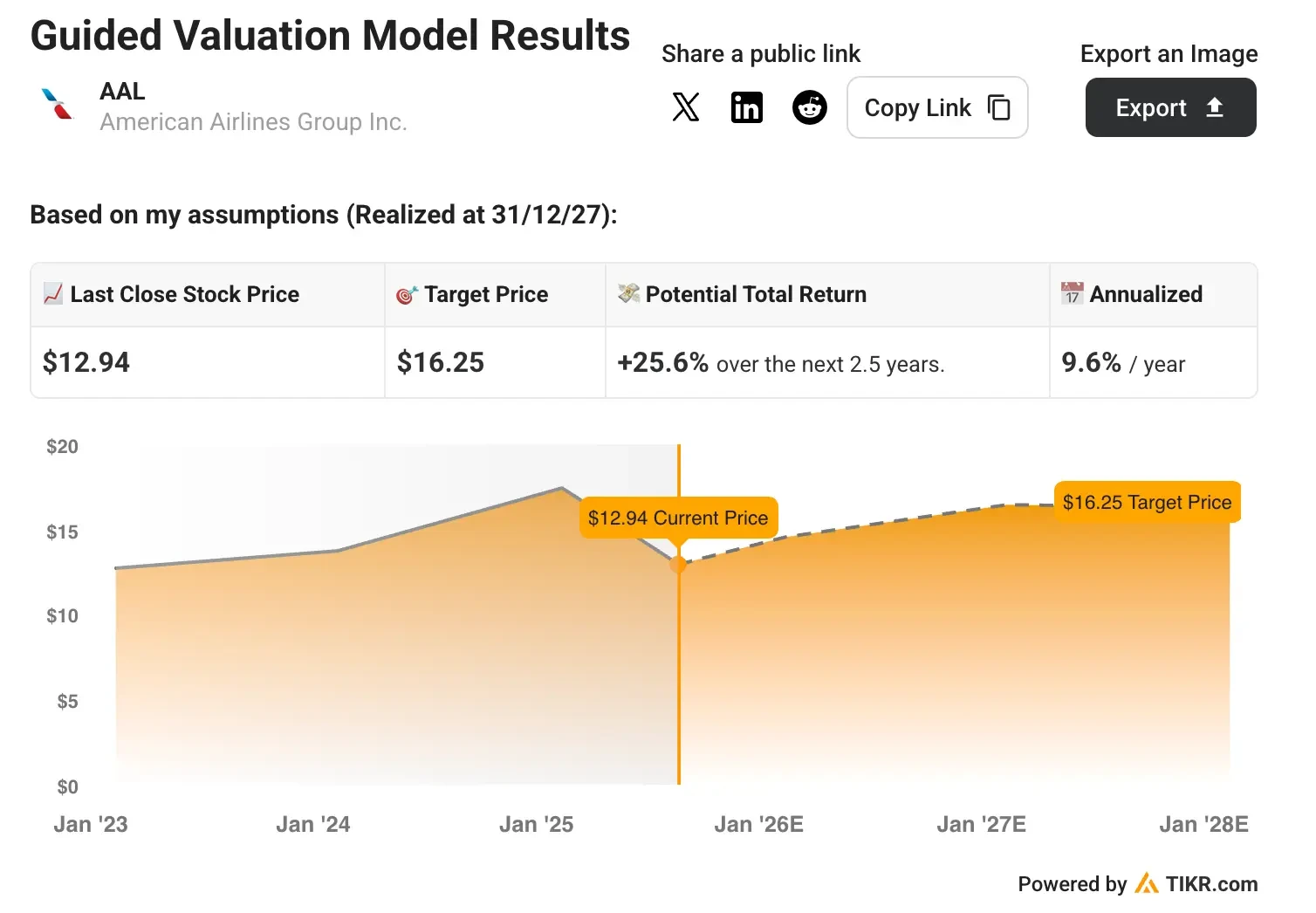

- Our valuation model projects AAL stock to deliver steady returns over the next 2.5 years.

American Airlines (AAL) is expected to report its second-quarter results on July 24, 2025. Analysts covering AAL stock anticipate revenue to decline by 0.28% year over year to $14.29 billion, while adjusted earnings are forecast to narrow by 29% to $0.77 per share.

The airline giant has beaten consensus earnings estimates in four of the last five quarters.

See analysts’ growth forecasts and price targets for any stock (It’s free!) >>>

A Challenging Macro Environment for AAL Stock

American Airlines reported its first-quarter 2025 results, which highlighted the challenging operating environment facing the airline industry.

The company posted a GAAP net loss of $473 million, or an adjusted loss of $0.59 per diluted share, while revenue of $12.6 billion declined 0.2% year-over-year, despite unit revenue growing 0.7%.

The airline has withdrawn its full-year outlook due to economic uncertainty. Still, management stated that if current demand trends continue, American expects to deliver a profitable year and produce positive free cash flow.

American Airlines faces a bifurcated demand environment that reflects broader economic pressures on consumer discretionary spending.

Its domestic passenger revenue per available seat mile (RASM) declined 0.7% year-over-year in Q1 as U.S. consumer spending on air travel decelerated throughout the quarter.

However, the airline’s international operations demonstrated resilience, with long-haul international passenger RASM leading performance.

Specific Metrics

Atlantic passenger RASM surged 10.5% year-over-year while Pacific passenger RASM increased 4.9% despite 24.1% more capacity, primarily driven by strength in Japan markets.

Premium cabin performance continues to outshine main cabin results, with premium revenue up 3% year-over-year despite a 0.3% decrease in capacity.

Premium cabin RASM outperformed main cabin RASM by 4 points domestically and 8 points internationally, while paid load factors in premium cabins reached historically high levels.

The company’s sales and distribution recovery remains on track, with management targeting the restoration of revenue share from indirect channels to historical levels by year-end.

Corporate-managed business revenue grew 8% year-over-year, despite the challenging backdrop, with particular strength in the financial and professional services sectors.

American’s loyalty program continues expanding, with AAdvantage enrollments increasing 6% year-over-year and loyalty revenues up 5%.

The enhanced co-branded credit card partnership with Citi, set to begin in 2026, represents a significant long-term revenue opportunity with expected 10% annual growth in remuneration.

Build your own Valuation Model to value any stock (It’s free!) >>>

Is AAL Stock a Buy Before Its Q2 Earnings?

Our valuation model estimates American Airlines to increase revenue by 4% year over year through 2028, while maintaining an operating margin of 5%.

Moreover, the model estimates AAL stock to maintain a forward price-to-earnings multiple of 7.5x, which is lower than the current multiple of 11x but in line with its three-year average.

We can see that the valuation model projects AAL stock to gain just 25% over the next 30 months, indicating an annual return of 9.6%. This suggests AAL stock might be reasonably valued today.

Notably, American Airlines stock has returned 10% in the last year, -9% in the last five years, and -73% in the previous 10 years.

Value AAL with TIKR’s Valuation Model today for FREE (Find undervalued stocks fast) >>>

Wall Street Analysts Are Bullish on These 5 Undervalued Compounders With Market-Beating Potential

TIKR just released a new free report on 5 compounders that appear undervalued, have beaten the market in the past, and could continue to outperform on a 1-5 year timeline based on analysts’ estimates.

Inside, you’ll get a breakdown of 5 high-quality businesses with:

- Strong revenue growth and durable competitive advantages

- Attractive valuations based on forward earnings and expected earnings growth

- Long-term upside potential backed by analyst forecasts and TIKR’s valuation models

These are the kinds of stocks that can deliver massive long-term returns, especially if you catch them while they’re still trading at a discount.

Whether you’re a long-term investor or just looking for great businesses trading below fair value, this report will help you zero in on high-upside opportunities.

Click here to sign up for TIKR and get our full report on 5 undervalued compounders completely free.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!