Key Stats for Pegasystems Stock

- Past-Week Performance: -3.5%

- 52-Week Range: $29.8 to $68.1

- Current Price: $43.7

What Happened?

Pegasystems stock (PEGA) trade at $43.7, sitting 35.8% below their 52-week high of $68.1 as sector-wide “SaaS apocalypse” fears batter the stock despite the company posting record-breaking $2 billion backlog milestones.

The selling pressure intensified after four analyst firms slashed their price targets on February 12, with Barclays delivering the most aggressive cut, dropping its target to $48 from $67, while D.A. Davidson, RBC, and Wedbush all trimmed to the $60 to $65 range.

Beneath the analyst downgrades, Pega’s 2025 engine ran at full throttle, with Pega Cloud ACV surging 33%, free cash flow jumping 45% to $491 million, and contractually committed backlog crossing $2 billion for the first time in company history.

Yet investors are actively debating whether Pegasystems deserves a premium workflow-automation multiple or whether AI disruption fears will keep dragging it down alongside commoditized SaaS peers.

COO and CFO Kenneth Stillwell stated on the Q4 earnings call that “we are seeing faster pipe build, faster progression and faster close times across the board with Blueprint,” directly linking the AI design agent to accelerating sales cycles and expanding net revenue retention of roughly 150 basis points above 2024 levels.

Also, supporting that growth thesis, the company’s board separately authorized an additional $1 billion in share buyback capacity alongside 2026 guidance calling for $575 million in free cash flow, signaling institutional-level conviction in the durability of Pega’s subscription model.

Looking further out, Pega’s structural bet on workflow-native agentic AI positions it as a direct alternative to Microsoft, Salesforce, and ServiceNow at the enterprise orchestration layer, a market Gartner now formally tracks as BOAT, where Pega currently holds the top-ranked position.

Wall Street’s Take on PEGA Stock

Pega’s Blueprint-driven ACV acceleration, which pushed Cloud ACV 33% higher in 2025 and backlog past $2 billion for the first time, directly validates the company’s path toward its $2 billion revenue guidance for 2026.

That trajectory is grounded in real numbers: revenue grew 16.6% in 2025 to $1.75 billion, EPS surged 38.6% to $2.10, and EBITDA margins expanded to 25.9%, with consensus projecting further expansion to 30.7% by end of 2026.

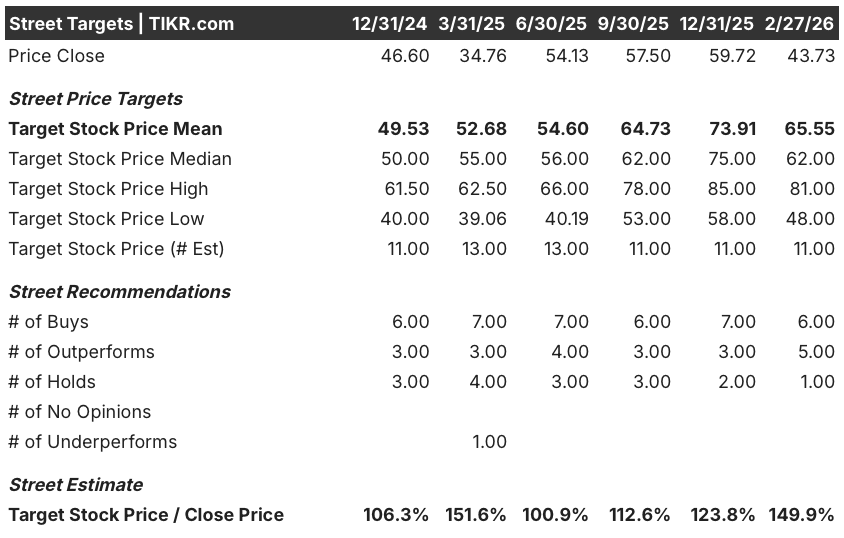

Currently, 6 analysts rate PEGA a Buy, 5 rate it Outperform, and 1 maintains a Hold, producing a mean price target of $65.55, implying 49.9% upside from the February 27 close of $43.73.

The analyst target range spans $48 on the low end to $81 on the high end, where Pega Cloud ACV sustaining above 30% growth and Blueprint-driven new logo wins would push shares toward the upper band, while further multiple compression from AI disruption fears anchors the downside.

What Does the Valuation Model Say?

TIKR’s mid-case valuation model sets a target price of $64.93, implying 48.5% total return over 4.8 years at an 8.5% annual IRR from current levels.

The market is pricing PEGA as a structurally threatened SaaS company, yet its free cash flow jumped 45% to $491 million in 2025, a performance inconsistent with a business in decline.

EPS is forecast to grow another 28.9% to $2.71 in 2026, making the current price a significant disconnect from the earnings trajectory.

Management’s $1 billion additional buyback authorization signals that leadership views the stock as meaningfully undervalued at these levels, not merely cheap.

The primary risk is that Pega Cloud ACV growth decelerates below 30% in 2026, which would collapse the premium multiple justification and expose the stock to another leg lower toward the $48 analyst floor.

Investors should watch the June 8 Investor Day at PegaWorld, where management will present the first full year of Blueprint data including pipeline build, win rates, and close time metrics that will either confirm or challenge the bull case.

PEGA is undervalued at $43.73, with a 49.9% mean analyst upside and an 8.5% IRR model target, but the June 8 Investor Day is the event that makes or breaks conviction here.

Should You Invest in Pegasystems Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up PEGA stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Pegasystems Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze PEGA stock on TIKR for Free →