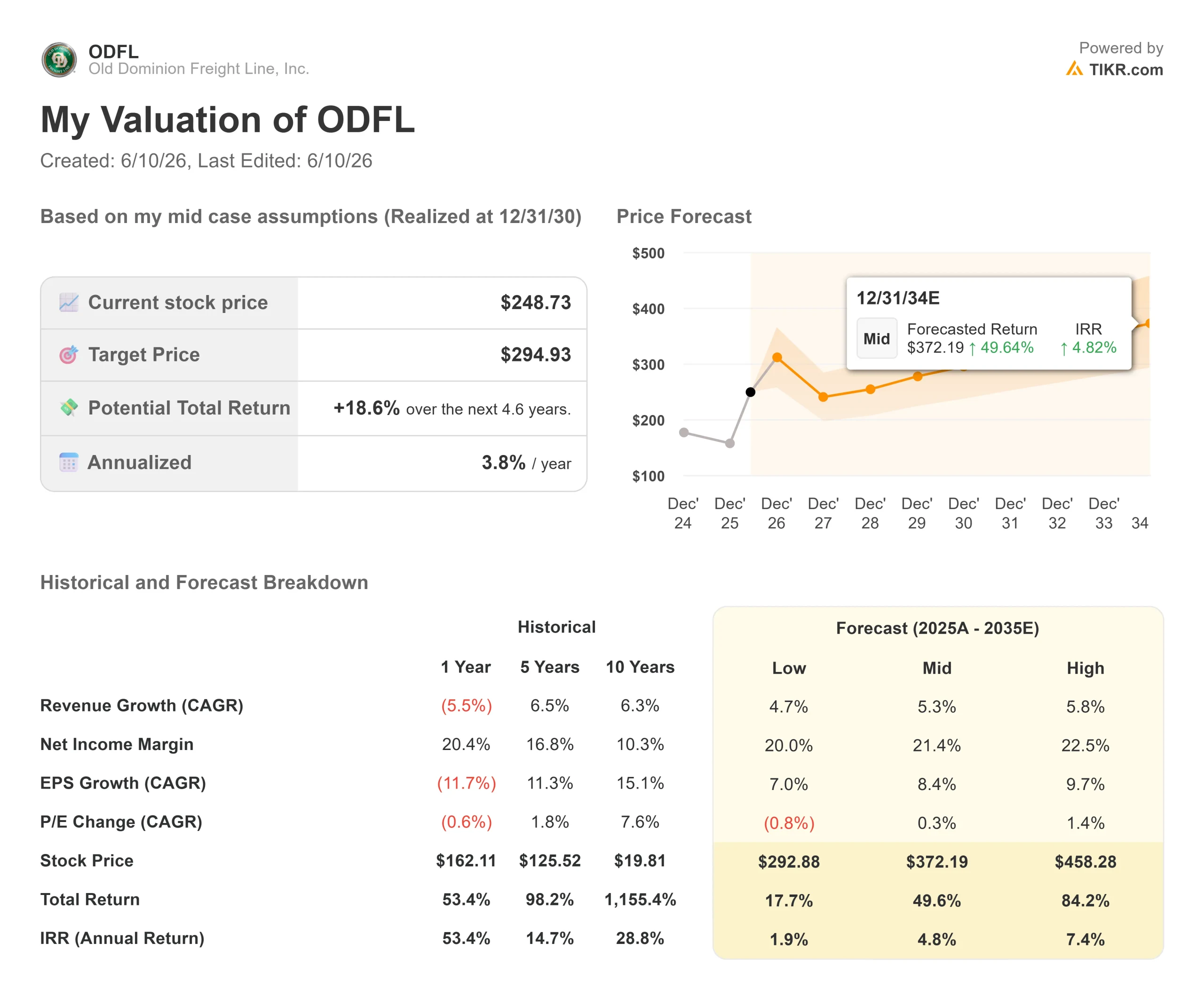

Key Stats for Old Dominion Freight Line Stock

- Current Price: $235.48

- Target Price (Mid): ~$295

- Street Consensus Target: ~$221

- Potential Total Return: ~19% (from model entry price of $248.73)

- Annualized IRR: ~4% / year

- Earnings Reaction: +1.47% on 4/29/26

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

The Day Amazon Came for LTL

Old Dominion Freight Line, Inc. (NASDAQ: ODFL) fell 5.33% to $235.48 on June 10 after Amazon announced a nationwide expansion of its less-than-truckload freight service. The stock had just touched a 52-week high of $252.03 the session prior. Saia and the newly independent FedEx Freight, which completed its spin-off from FedEx Corp. on June 1, also dropped sharply. The reaction was sector-wide and fast.

Amazon’s move, made through its Amazon Supply Chain Services unit, extends its LTL offering beyond inbound-to-Amazon shipments to any destination, including third-party warehouses, distribution centers, and retail partners. According to Amazon’s press release, the service is backed by more than 80,000 trailers and 24,000 intermodal containers and targets shipments between one and six pallets, or between 150 and 15,000 pounds. That is a direct push into territory Old Dominion has served for over 90 years.

The question investors need to answer: is the market pricing in a real structural threat, or just a headline?

What the Reaction Is Actually Pricing In

Raymond James said Amazon’s entry is not near-term thesis-changing for public LTL carriers but is worth watching. The firm noted that LTL operations depend on terminal density, pickup-and-delivery execution, freight handling, and service consistency, areas where carriers like Old Dominion hold structural advantages built over decades. Raymond James also said the greatest near-term risk falls on small and mid-sized shippers already inside Amazon’s ecosystem, while larger enterprise shippers may resist sharing freight and supply chain data with a direct competitor.

That distinction is important. Old Dominion’s business, detailed in its investor relations materials, is built on a service premium that commands higher pricing, not pallet-rate competition.

On the Q1 2026 earnings call, CFO Adam Satterfield addressed competitive pressure directly when asked about the FedEx Freight spin-off: “The service gap between us and our competition is as wide as it’s ever been, if not getting wider.” That statement was backed by concrete metrics: 99% on-time delivery and a cargo claims ratio below 0.1% in Q1, both industry-leading figures.

Amazon does not replicate either of those metrics overnight.

See historical and forward estimates for Old Dominion Freight Line stock (It’s free!) >>>

What the Operating Data Shows

The sell-off arrives during genuinely improving fundamentals.

Old Dominion reported Q1 2026 EPS of $1.14 against a Street estimate of $1.05, an 8.46% beat, with revenue of $1.33 billion also above expectations. The stock rose 1.47% on earnings day. On the call, Satterfield said the company was comfortable with the historical seasonal improvement of 300 to 350 basis points in operating ratio from Q1 to Q2. That guidance was issued before Amazon’s announcement.

Then on June 3, Old Dominion’s mid-quarter update showed May revenue per day up 12.3% year-over-year, driven by pricing strength that more than offset a 3.8% decline in LTL tons per day. Weight per shipment, a measure Satterfield flagged as a leading indicator of industrial demand, rose 1.6% year-over-year in May. He noted on the Q1 call that weight per shipment in strong markets has historically run around 1,600 pounds, compared to the current roughly 1,490 pounds. That gap is where the operating leverage story lives.

On the quality of freight coming back from truckload consolidation, President and CEO Marty Freeman was direct: “When it moves back over to us, it moves at that profitable LTL pricing that we have in effect for them.” Amazon’s competing on small-pallet pricing does not unwind that dynamic.

The Balance Sheet Behind the Position

Old Dominion carries a net cash position of $248 million with no meaningful debt. In Q1 2026, it generated $373.6 million in cash from operations, returned $88.1 million through share repurchases, and spent $62.6 million on capital expenditures.

Full-year 2025 free cash flow was $985 million. Consensus estimates on the TIKR project are that it will rise to around $1.28 billion in 2026, a roughly 30% increase, as the capital spending cycle winds down. The 2026 capital plan is $265 million, compared to $415 million in 2025. That pullback is deliberate: after nearly $2 billion in capital expenditures over the prior three years, the network was built in anticipation of volume recovery. With over 35% excess service center capacity, incremental freight flows through at very high profit margins without requiring proportional new spending.

Return on invested capital sits at 27.9% on a trailing basis, at depressed volume levels.

See how Old Dominion Freight Line performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $235.48

- Target Price (Mid): ~$295

- Potential Total Return: ~19% (from model entry of $248.73)

- Annualized IRR: ~4% / year

The mid case uses a revenue CAGR of around 5% and a net income margin expanding toward 21%, up from 18.6% in 2025. Both inputs are driven by operating leverage: more freight flowing through a largely fixed-cost network running well below capacity. Satterfield noted on the Q1 call that in prior recovery years, specifically 2014-15, 2017-18, and 2021-22, ODFL outgrew peers by 900 to 1,000 basis points in volume. If that pattern repeats, the mid case may prove conservative.

The primary risk is a stalled recovery. If macro uncertainty keeps industrial freight subdued through 2026, or if Amazon captures enough small-shipper volume to blunt sequential tonnage improvement, operating leverage gets delayed. The stock trades at 26.56x NTM EV/EBITDA and 43.64x NTM P/E, which leaves limited room for disappointment and means ODFL already trades above the Street consensus target of ~$221.

Conclusion

The real test is not Amazon’s announcement. It is Q2 tonnage.

Satterfield guided to sequential volume improvement through June, and the May data confirmed that the trend is intact. If June holds and Q2 operating ratio improvement lands in the guided 300 to 350 basis point range, today’s sell-off will look like an overreaction. If tonnage misses and the operating ratio disappoints, the premium valuation at 43.64x forward earnings becomes harder to defend. Watch Old Dominion’s Q2 earnings report, expected in late July. That number will answer the question raised in today’s headline.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Old Dominion Freight Line?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Old Dominion Freight Line, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Old Dominion Freight Line alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Old Dominion Freight Line on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!