Key Takeaways:

- The 2-Minute Valuation Model values Block stock at $75 per share in 2 years.

- That’s a potential 63% upside from today’s price of $36 per share.

- XYZ stock currently trades at 14.0x forward earnings, significantly below its historical average of 33.7x.

- Block’s recent earnings missed Wall Street expectations across key metrics, leading to multiple analyst downgrades.

- Get accurate financial data on over 100,000 global stocks for free on TIKR >>>

Block (XYZ), the financial technology entity formerly known as Square (SQ), presents a complex investment case.

The company shows strong long-term earnings growth potential. However, it faces near-term challenges with Cash App user stagnation and weakening consumer spending.

The recent stock selloff following disappointing Q1 results creates risks and opportunities for investors.

Given its mixed outlook, let’s analyze whether Block’s current valuation offers a compelling risk-reward proposition today.

Find the best stocks to buy today with TIKR. (It’s free) >>>

What is the 2-Minute Valuation Model?

Three core factors drive a stock’s long-term value:

- Revenue Growth: How big the business becomes.

- Margins: How much the business earns in profit.

- Multiple: How much investors are willing to pay for a business’s earnings.

Our 2-Minute Valuation Model uses a simple formula to value stocks:

Expected Normalized EPS * Forward P/E ratio = Expected Share Price

Revenue growth and margins drive a company’s long-term normalized earnings per share (EPS), and investors can use a stock’s long-term average P/E multiple to get an idea of how the market values a company.

Why Block Stock Looks Undervalued

Forecast

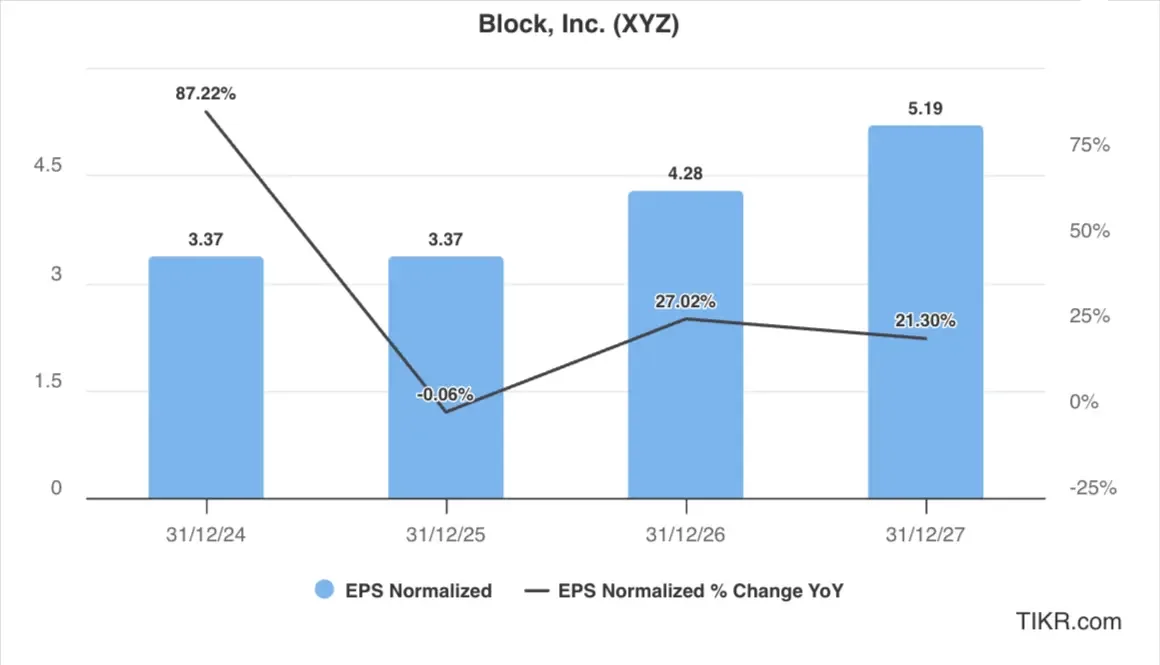

Block’s projected earnings path shows considerable volatility but ultimately leads to steady growth. This earnings pattern reflects Block’s current challenges, with flat growth expected in 2025 and over 20% expected annual EPS growth in 2026 and 2027.

This earning trajectory aligns with management’s comments about facing a “more dynamic macro environment” while implementing strategies to reignite growth in the latter half of the year.

Block’s revenue is expected to grow 6% in 2025, followed by high-single-digit expected annual revenue growth in 2026 and 2027.

This earnings growth for XYZ stock is likely to be driven by:

- Cash App Borrow Expansion: FDIC approval enables Block to double the eligible users for its lending product while improving unit economics by bringing loan servicing in-house.

- International Growth: International markets now represent nearly 18% of volume and continue to show strong momentum, providing a buffer against U.S. market challenges.

- Ecosystem Strength: The integration of Afterpay’s buy-now-pay-later functionality with Cash App Card enhances the company’s credit offerings and strengthens its ecosystem.

- Square Business Resilience: Despite competitive pressures, Square continues to gain market share in target verticals, including retail, food, and beverage.

For our valuation, we’ll estimate that Block will reach $5 in EPS in 2027.

Check out Block’s full analyst estimates (It’s free) >>>

Is Block Stock Undervalued Right Now?

XYZ stock has averaged a forward P/E multiple of 34x over the last three years, with peaks above 99 during growth-oriented market periods. Currently, Block stock trades at about 14 times forward earnings.

The fintech stock is trading at less than half its historical average multiple and near its all-time lows, which indicates extreme investor skepticism.

While some multiple compression is justified given recent challenges, the current multiple may not fully account for the company’s long-term growth potential and the value of its ecosystem across Square and Cash App.

For our valuation, we’ll use a conservative forward P/E multiple of 15x, which is slightly higher than where the stock trades today acknowledging the company’s strong growth profile.

Fair Value of Block Stock

Using our 2-Minute Valuation Model and applying a conservative approach:

- Conservative 2027 EPS estimate: $5

- Conservative forward P/E multiple: 15x

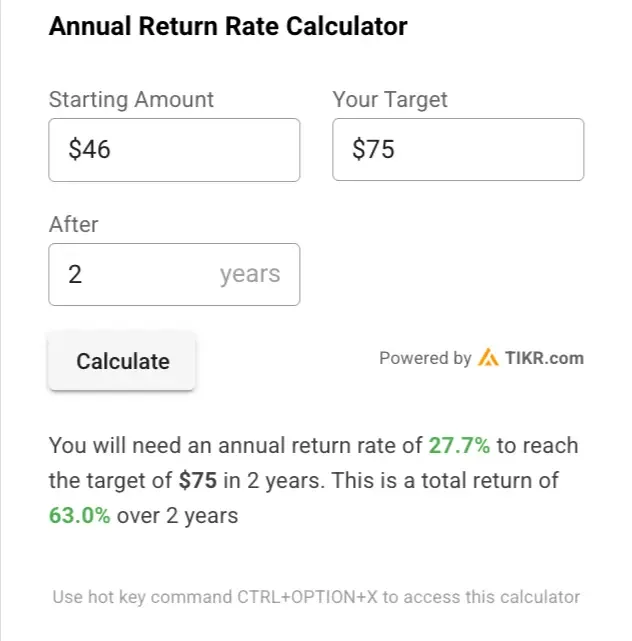

Expected Normalized EPS ($5) * Forward P/E ratio (15x) = Expected Share Price ($75)

The 2-year expected XYZ stock price we would get from this valuation is $75 per share.

With Block stock currently trading at around $46 per share, this implies a potential upside of 63% over the next two years or a 28% annualized return.

Remember, this is just a valuation exercise, and we don’t know for sure what the stock’s price will be in the future.

Value stocks quicker with TIKR (It’s free, no card required) >>>

What is the Target Price for XYZ Stock?

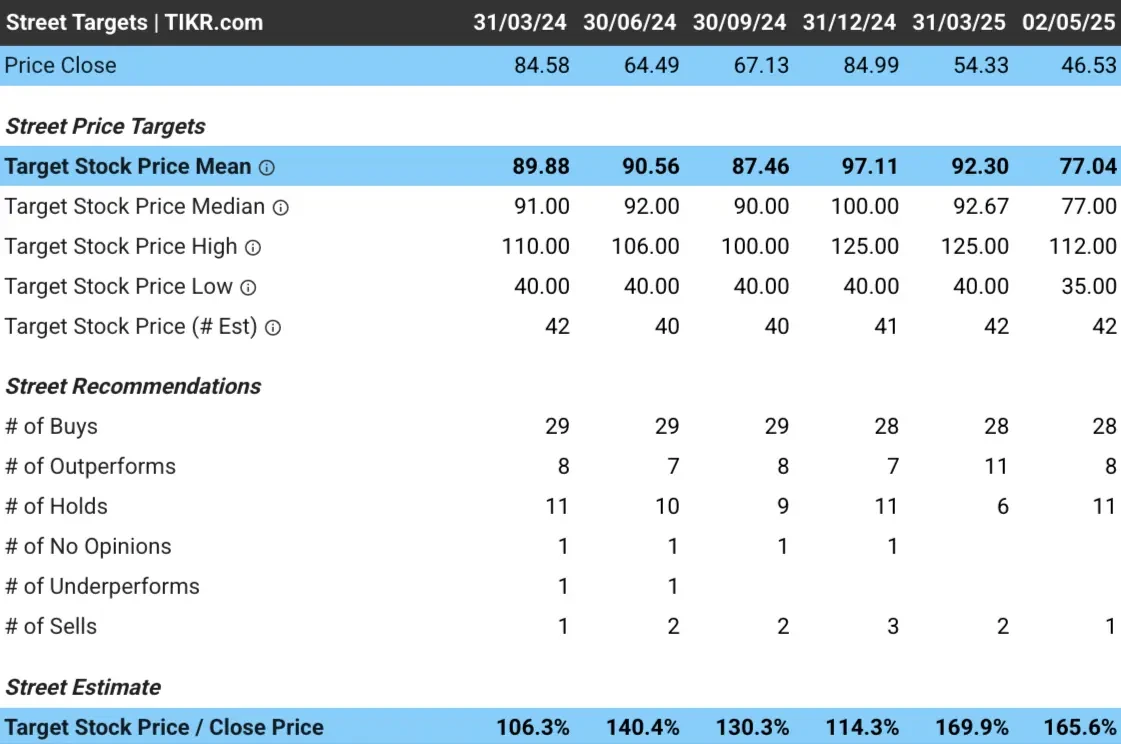

Block could have strong upside today.

Analysts have an average price target of around $77 per share for XYZ stock, indicating they see about 66% upside today for Block based on the stock’s current share price:

Risks to Consider

Even though our valuation suggests the stock could be worth around $75 per share, investors should be aware of several risks for the stock:

- Cash App User Stagnation: The flat user growth in Cash App, traditionally a key growth driver, raises serious concerns about market saturation and competitive pressures from rivals like Venmo.

- Consumer Spending Weakness: Lower consumer spending and reduced inflows during tax season suggest broader economic headwinds that could persist.

- Heightened Competition: Block faces competition from established players like Toast, Fiserv’s Clover, and PayPal’s Venmo, which reported 20% revenue growth in the same quarter.

- Execution Challenges: The company’s plan to increase marketing spend by 50% in Q2 to reaccelerate growth represents a significant expense with uncertain returns.

- Macroeconomic Headwinds: Recent tariff announcements and broader economic uncertainty could further pressure consumer spending and payment volumes.

TIKR Takeaway

Block presents a higher-risk, high-reward investment proposition. The recent selloff has compressed the stock’s valuation to near historical lows, potentially creating an attractive entry point for long-term investors who believe in the company’s ability to overcome current challenges.

However, the stagnation in Cash App users, missed earnings, and reduced guidance suggest ongoing operational issues that may take time to resolve. Investors considering a position should be prepared for continued volatility in the near term.

For investors with high risk tolerance and a long-term horizon, the current valuation may represent an opportunity to acquire shares of a leading fintech innovator at a substantial discount to historical levels.

Is Block stock a buy over the next 24 months? Use TIKR to check the stock’s analyst price targets and growth forecasts to see if it is undervalued today.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!