Key Takeaways:

- RTX offers a 1.8% dividend yield, slightly below its 5-year average of 2.45%, reflecting recent share price gains.

- Over the next 2 years, EPS is expected to grow 11.2% annually, while dividends are projected to rise 8.5% annually over the same period.

- TIKR’s valuation model suggests a potential total return of 22% by 2027, supported by steady earnings growth, a robust defense backlog, and a reasonable valuation multiple.

RTX is one of the most important players in the global aerospace and defense industry, with a portfolio that includes Pratt & Whitney (jet engines), Collins Aerospace (avionics and systems), and Raytheon (defense systems).

These three segments serve both commercial aviation and military customers, allowing RTX to benefit from two powerful growth trends at once.

Global air travel is rebounding, driving demand for engine parts, MRO services, and new aircraft systems. At the same time, rising geopolitical tensions are prompting governments to boost defense spending.

That combination gives RTX a unique advantage as one of the few industrials with diversified and resilient long-term growth drivers.

The company faced pressure in 2023 due to engine inspections and supply chain issues, but it has started recovering.

With earnings expected to grow steadily through 2027 and dividends rising alongside, RTX remains a compelling pick for long-term investors looking for exposure to both global security and commercial aviation.

RTX Could Offer Nearly 22% Upside Based on Analyst Forecasts

RTX shares currently trade around $157, but based on analysts’ consensus estimates used in TIKR’s valuation model, the stock could reach $191.53 by the end of 2027. That implies a potential total return of 21.9% over the next 2.4 years, or about 8.5% annually including dividends.

The model assumes RTX grows revenue at 5.9% per year, expands operating margins to 13.5%, and trades at a 23.5x P/E multiple. This is slightly below the 25.6x forward P/E multiple that the stock trades at today.

Given RTX’s strong defense backlog, improving fundamentals, and exposure to rising global defense budgets, this valuation looks reasonable. If the company continues to deliver across both its commercial and defense businesses, long-term investors could see some upside from here.

Value any stock in less than 60 seconds with TIKR (It’s free) >>>

A 1.75% Dividend Yield That Could Grow With Earnings

RTX’s forward dividend yield sits at 1.8%, below its 5-year average of 2.45%. The lower yield reflects the recent stock rally, not a lack of dividend strength.

The company is projected to pay $2.62/share in dividends in 2025, rising to $3.09/share by 2027. That represents roughly 8.6% annual dividend growth, outpacing many industrial peers and closely tracking earnings growth.

While the current yield may not satisfy income-focused investors, the payout is backed by consistent free cash flow and long-term defense contracts.

RTX is also well-positioned to benefit from long-term trends in global defense spending, which should support both earnings and dividend growth for years to come.

Find high-quality dividend stocks that look even better than RTX Corporation today. (It’s free) >>>

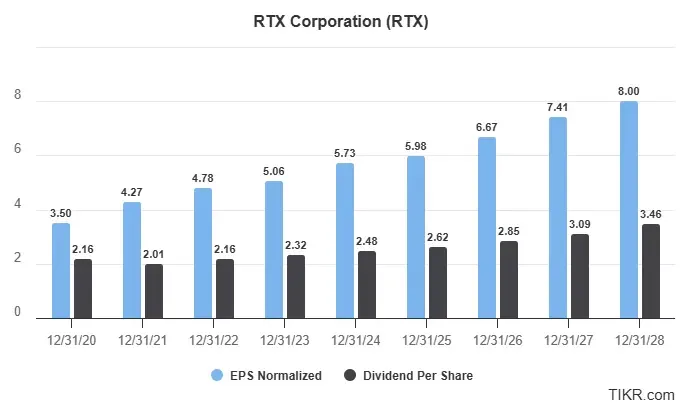

Dividend Payout Looks Safe With Room for Upside

RTX is projected to earn $5.98 per share in 2025, with EPS expected to grow to $7.41 by 2027. That represents a 3-year compound annual growth rate (CAGR) of approximately 11.2%.

Over the same period, the company is expected to grow its annual dividend from $2.62 to $3.09, a CAGR of about 8.5%.

This puts the payout ratio at a healthy 43.8% in 2025, improving slightly to 41.7% by 2027, giving RTX room to continue growing its dividend while reinvesting in both defense and aerospace operations.

These levels are comfortably below the 60% threshold most dividend investors look for, giving RTX plenty of room to continue growing its payout without stretching its balance sheet.

RTX’s growth is being fueled by a multi-year increase in global defense spending, a recovery in commercial air traffic, and steady demand for high-margin aftermarket services. Its large backlog of long-term contracts also provides strong visibility and consistent earnings potential.

Long-term, RTX’s blend of commercial aerospace and defense makes it uniquely resilient. If one side of the business slows down, the other can help offset the dip.

From an investor’s point of view, the dividend isn’t the headline. It’s the cherry on top. The real story is the consistent earnings growth and long-term compounding potential, backed by strong free cash flow and global demand.

See RTX Corporation’s full growth forecast and analyst estimates. (It’s free) >>>

Wall Street Analysts Are Bullish on These 5 Undervalued Compounders With Market-Beating Potential

TIKR just released a new free report on 5 compounders that appear undervalued, have beaten the market in the past, and could continue to outperform on a 1-5 year timeline based on analysts’ estimates.

Inside, you’ll get a breakdown of 5 high-quality businesses with:

- Strong revenue growth and durable competitive advantages

- Attractive valuations based on forward earnings and expected earnings growth

- Long-term upside potential backed by analyst forecasts and TIKR’s valuation models

These are the kinds of stocks that can deliver massive long-term returns, especially if you catch them while they’re still trading at a discount.

Whether you’re a long-term investor or just looking for great businesses trading below fair value, this report will help you zero in on high-upside opportunities.

Click here to sign up for TIKR and get our full report on 5 undervalued compounders completely free.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!