Key Takeaways:

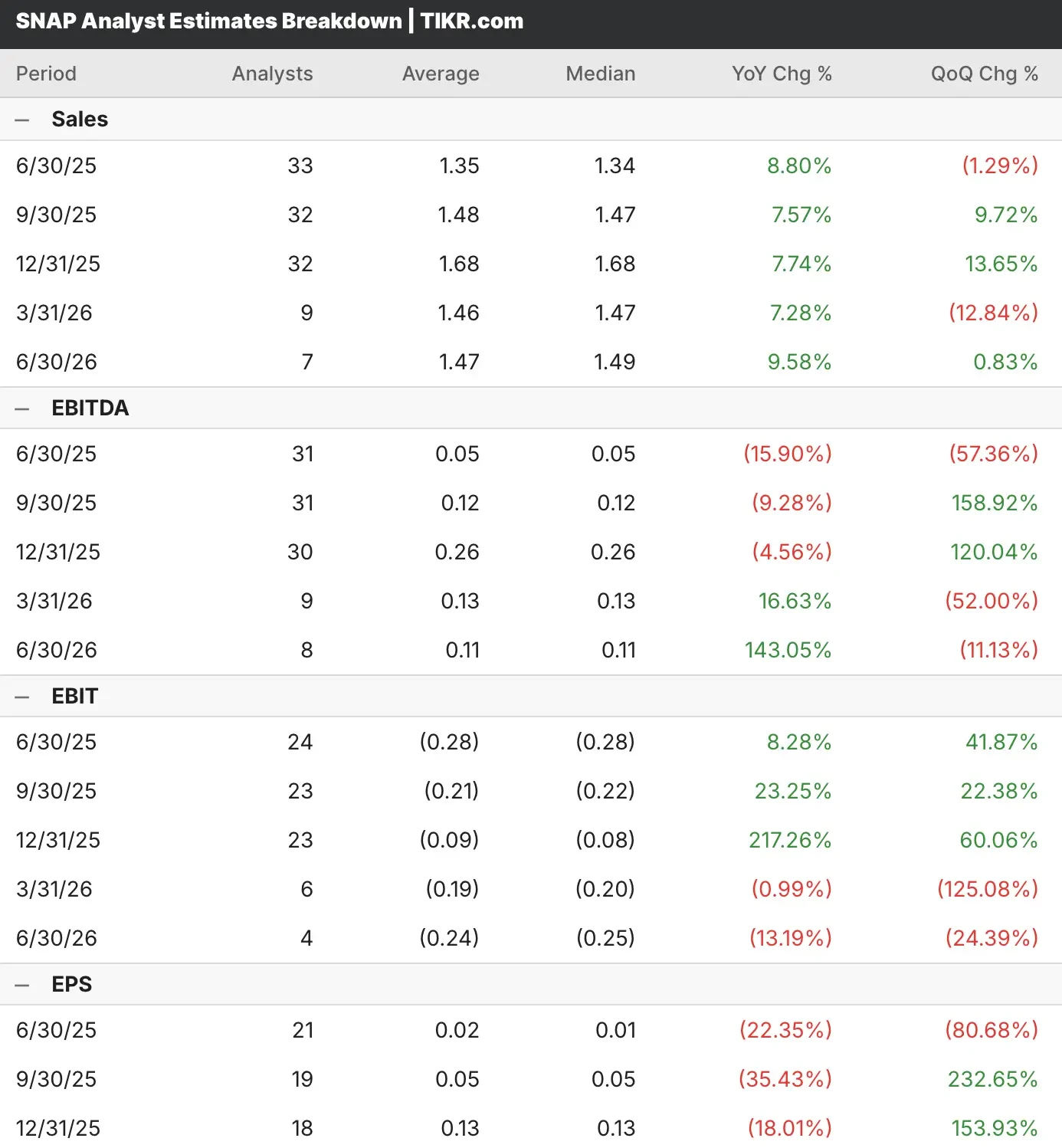

- Analysts expect Snap to report modest revenue growth of 9% in Q2, amid macroeconomic headwinds and trade policy uncertainties affecting advertiser spending.

- The social media platform is approaching the milestone of 1 billion monthly active users while demonstrating strong momentum in direct response advertising and subscription revenue.

- Our valuation model forecasts that SNAP stock could deliver an annualized return of 6.9% over the next 2.4 years.

Snap (SNAP) is prepared to report its second-quarter results following a volatile first-quarter performance that showcased progress in advertising platform improvements and user engagement growth.

Analysts covering SNAP stock expect revenue to increase by 9% year over year to $1.35 billion while the company continues working toward profitability, with projected losses narrowing significantly.

The visual communication platform has demonstrated resilience through macroeconomic uncertainties while building toward its strategic goal of reaching 1 billion monthly active users and achieving sustainable profitability.

Snap has shown consistent execution across key strategic priorities, including advertising platform enhancement, community growth, and augmented reality innovation.

SNAP stock has beaten revenue and earnings estimates in four of the last five quarters. Despite its consistent outperformance, SNAP stock has declined following its earnings results in three of the last five quarters.

See analysts’ growth forecasts and price targets for any stock, including SNAP (It’s free!) >>>

A Focus on Snap’s Platform Evolution

Snap continued to see strong user growth, reporting over 850 million monthly active users while maintaining steady growth toward its 1 billion user target, driven by continued adoption of visual communication in emerging markets.

SNAP’s direct response advertising business accounted for 75% of total advertising revenue for the first time, reflecting successful platform improvements and growing advertiser performance optimization capabilities.

Machine learning model enhancements delivered substantial improvements with 6x faster learning rates and 5x increased training data volume, contributing to better ad personalization and content recommendation systems.

Snapchat+ subscription revenue reached an annualized run rate of over $500 million, with over 13 million subscribers, demonstrating successful revenue diversification beyond traditional advertising models.

The fifth-generation Spectacles platform continues to advance augmented reality capabilities with features like advanced hand tracking and enhanced developer tools for AR content creation.

Small and medium business advertiser growth remains strong, with total active advertisers increasing over 60% year-over-year, supported by Snap Promote platform expansion and simplified advertising tools.

Content engagement improvements through fresher machine learning models doubled views on Spotlight posts less than 24 hours old, accelerating the creator posting flywheel and improving user retention.

Trade policy uncertainties and de minimis exemption changes have created near-term headwinds for some advertiser segments, though management maintains confidence in long-term platform fundamentals.

Build your own Valuation Model to value any stock (It’s free!) >>>

Is SNAP Stock a Buy Before Its Q2 Earnings?

Our valuation model estimates that Snap will benefit from continued user growth and advertising platform improvements while successfully navigating macroeconomic challenges throughout the forecast period.

The model projects SNAP stock to appreciate from its current price of $9.43 to a target price of $11.09, representing a potential total return of 17.6% over the next 2.4 years.

This translates to an annualized return expectation of 6.9%, suggesting SNAP stock offers moderate upside potential for investors seeking exposure to visual communication platforms and augmented reality innovation trends.

Management’s disciplined approach to cost management, evidenced by lowering full-year expense guidance while maintaining strategic investments, positions Snap to achieve improved profitability as revenue growth accelerates.

Snap’s focus on direct response advertising and revenue diversification through Snapchat+ subscriptions creates multiple pathways to sustainable business model improvement and long-term value creation.

FAQs

1. Is SNAP stock a buy, hold, or sell now?

Of the 44 analysts covering SNAP stock, eight recommend “Buy”, 33 recommend “Hold”, and three recommend “Sell”.

2. Who is the biggest shareholder of SNAP?

Tencent is the largest shareholder in SNAP stock and owns over 16% of the total outstanding shares.

3. What is the SNAP stock price target?

Our valuation model suggests a 2.4-year target price of $11.09, representing an upside potential of 18% from current trading levels.

4. How much is Snapchat worth in 2025?

As of today, SNAP stock trades at a market cap of almost $16 billion.

Value SNAP with TIKR’s Valuation Model today for FREE (Find undervalued stocks fast) >>>

Wall Street Analysts Are Bullish on These 5 Undervalued Compounders With Market-Beating Potential

TIKR just released a new free report on 5 compounders that appear undervalued, have beaten the market in the past, and could continue to outperform on a 1-5 year timeline based on analysts’ estimates.

Inside, you’ll get a breakdown of 5 high-quality businesses with:

- Strong revenue growth and durable competitive advantages

- Attractive valuations based on forward earnings and expected earnings growth

- Long-term upside potential backed by analyst forecasts and TIKR’s valuation models

These are the kinds of stocks that can deliver massive long-term returns, especially if you catch them while they’re still trading at a discount.

Whether you’re a long-term investor or just looking for great businesses trading below fair value, this report will help you zero in on high-upside opportunities.

Click here to sign up for TIKR and get our full report on 5 undervalued compounders completely free.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!