Key Takeaways:

- Arista Networks delivered its first $2 billion quarterly revenue milestone in Q1, doubling from its first billion-dollar quarter just 11 quarters prior, driven by robust AI infrastructure demand.

- The company maintains confidence in its $750 million back-end AI revenue target for 2025 while navigating tariff uncertainties that could impact margins by 1-1.5 percentage points without mitigation.

- Our valuation model forecasts that ANET stock could deliver an annualized return of 7.6% over the next 2.4 years, with shares potentially reaching $140 from current levels around $118.

Arista Networks (ANET) is prepared to report its second-quarter results tomorrow after the market closes.

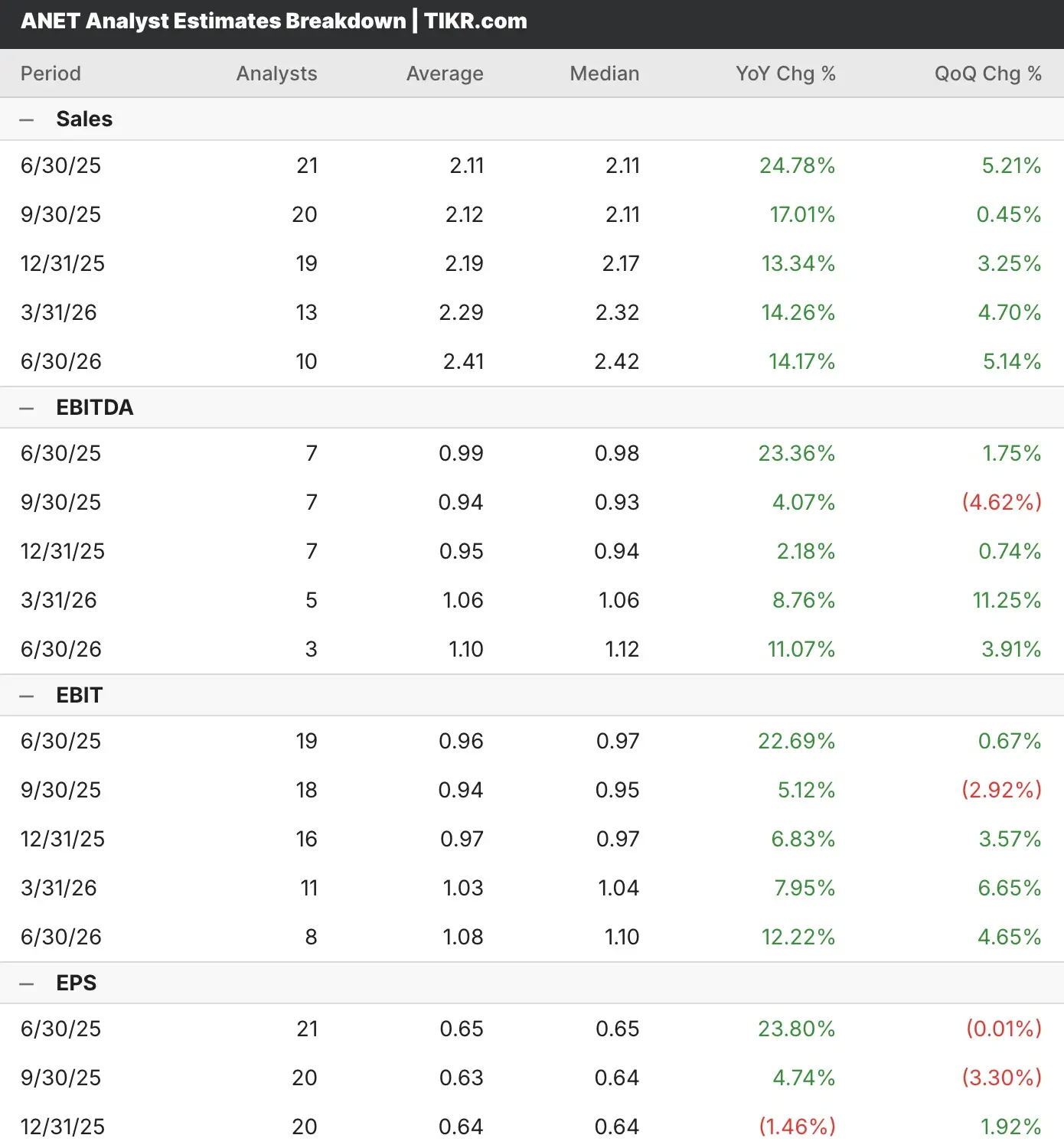

Analysts covering ANET stock expect revenue to increase by 25% year over year to $2.11 billion while earnings are forecast to expand by 24% to $0.65 per share.

Arista Networks continues its impressive growth trajectory as the networking infrastructure leader positions itself at the center of the artificial intelligence revolution sweeping through data centers worldwide.

The company reported exceptional first-quarter results with revenue of $2.01 billion, representing 27.6% year-over-year growth and marking its first $2 billion quarter, a milestone achieved just 11 quarters after crossing the $1 billion threshold.

Analysts covering ANET stock expect continued momentum with robust growth projections, as the company benefits from massive AI infrastructure buildouts by cloud titans and emerging AI-focused customers.

ANET stock has beaten revenue and earnings estimates in each of the last five quarters. Despite its consistent outperformance, Arista Networks’ stock has declined following its earnings results in the previous three quarters.

See analysts’ growth forecasts and price targets for any stock, including ANET (It’s free!) >>>

A Focus on Arista’s AI Infrastructure Leadership

Arista Networks delivered exceptional first-quarter results with non-GAAP gross margins of 64.1%, demonstrating strong pricing power across cloud titans, enterprise customers, and AI-focused deployments.

Revenue growth was primarily driven by accelerating demand for its AI infrastructure solutions, purpose-built for AI workloads requiring ultra-low latency networking solutions. Software and service renewals contributed 17% of total revenue, underscoring recurring revenue strength.

Management guided Q2 revenue to approximately $2.1 billion while updating its outlook to incorporate the effects of both strong performance and the new tariff risks.

Arista has established itself as the preferred networking partner for major cloud providers building massive GPU clusters.

Arista Networks remains confident in its $750 million back-end AI revenue target for 2025, with all four major AI customers progressing toward production. Management noted that two customers are approaching 50,000 GPU deployments by year-end, with the potential to scale to 100,000 GPUs.

CEO Jayshree Ullal highlighted Arista’s key differentiation: single-point network control and visibility crucial for identifying performance bottlenecks in clusters scaling to 100,000 XPUs. The Etherlink product family has become the industry standard for AI spine and leaf network designs.

Beyond AI, Arista continues expanding in traditional cloud and enterprise markets. The campus networking initiative gained Q1 momentum, targeting a $16 billion addressable market.

Notable wins include a major federal agency deployment, marking government sector entry with comprehensive switching and CloudVision management.

International revenue increased to 20.3% from 16% quarter-over-quarter, demonstrating global demand growth.

Arista faces potential 1-1.5 percentage point gross margin pressure from proposed tariffs. The company implemented a three-pronged strategy: supply chain diversification, tariff absorption, and selective price increases.

Inventory increased from $1.8 billion to about $2 billion quarter-over-quarter as a strategic buffer, with manufacturing flexibility across Mexico, Malaysia, and Vietnam.

Build your own Valuation Model to value any stock (It’s free!) >>>

Is ANET Stock a Buy Before Its Q2 Earnings?

Our valuation model, based on analysts’ consensus estimates, expects that Arista will benefit from sustained AI infrastructure growth and successful enterprise market expansion while navigating macroeconomic challenges throughout the forecast period.

The model projects ANET stock to appreciate from its current price of $118 to a target price of $140, representing a potential total return of 19.3% over the next 2.4 years.

This translates to an annualized return expectation of 7.6%, suggesting ANET stock offers attractive upside potential for investors seeking exposure to AI infrastructure trends and cloud networking modernization.

Management’s demonstrated execution across AI customer ramps, combined with disciplined cost management and strategic diversification into enterprise markets, positions ANET stock for sustained growth as digital transformation accelerates across industries.

Arista’s unique position as the premier Ethernet networking provider for AI workloads, coupled with its expanding campus networking presence, creates multiple pathways for long-term value creation and market share gains.

FAQs

1. What is the price target for ANET stock?

Given consensus estimates, the ANET stock price target is $111, which is 5% below the current target price.

2. Who is the biggest shareholder of ANET?

The Bechtolsheim Family Trust is the largest shareholder in ANET stock and owns over 14% of the total outstanding shares.

3. Is ANET stock profitable?

Yes, Wall Street projects Arista Networks to end 2025 with an adjusted net income of $3.28 billion or $2.57 per share.

4. How much is Arista Networks worth in 2025?

As of today, ANET stock trades at a market cap of almost $148 billion.

Value ANET with TIKR’s Valuation Model today for FREE (Find undervalued stocks fast) >>>

Wall Street Analysts Are Bullish on These 5 Undervalued Compounders With Market-Beating Potential

TIKR just released a new free report on 5 compounders that appear undervalued, have beaten the market in the past, and could continue to outperform on a 1-5 year timeline based on analysts’ estimates.

Inside, you’ll get a breakdown of 5 high-quality businesses with:

- Strong revenue growth and durable competitive advantages

- Attractive valuations based on forward earnings and expected earnings growth

- Long-term upside potential backed by analyst forecasts and TIKR’s valuation models

These are the kinds of stocks that can deliver massive long-term returns, especially if you catch them while they’re still trading at a discount.

Whether you’re a long-term investor or just looking for great businesses trading below fair value, this report will help you zero in on high-upside opportunities.

Click here to sign up for TIKR and get our full report on 5 undervalued compounders completely free.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!