Key Takeaways:

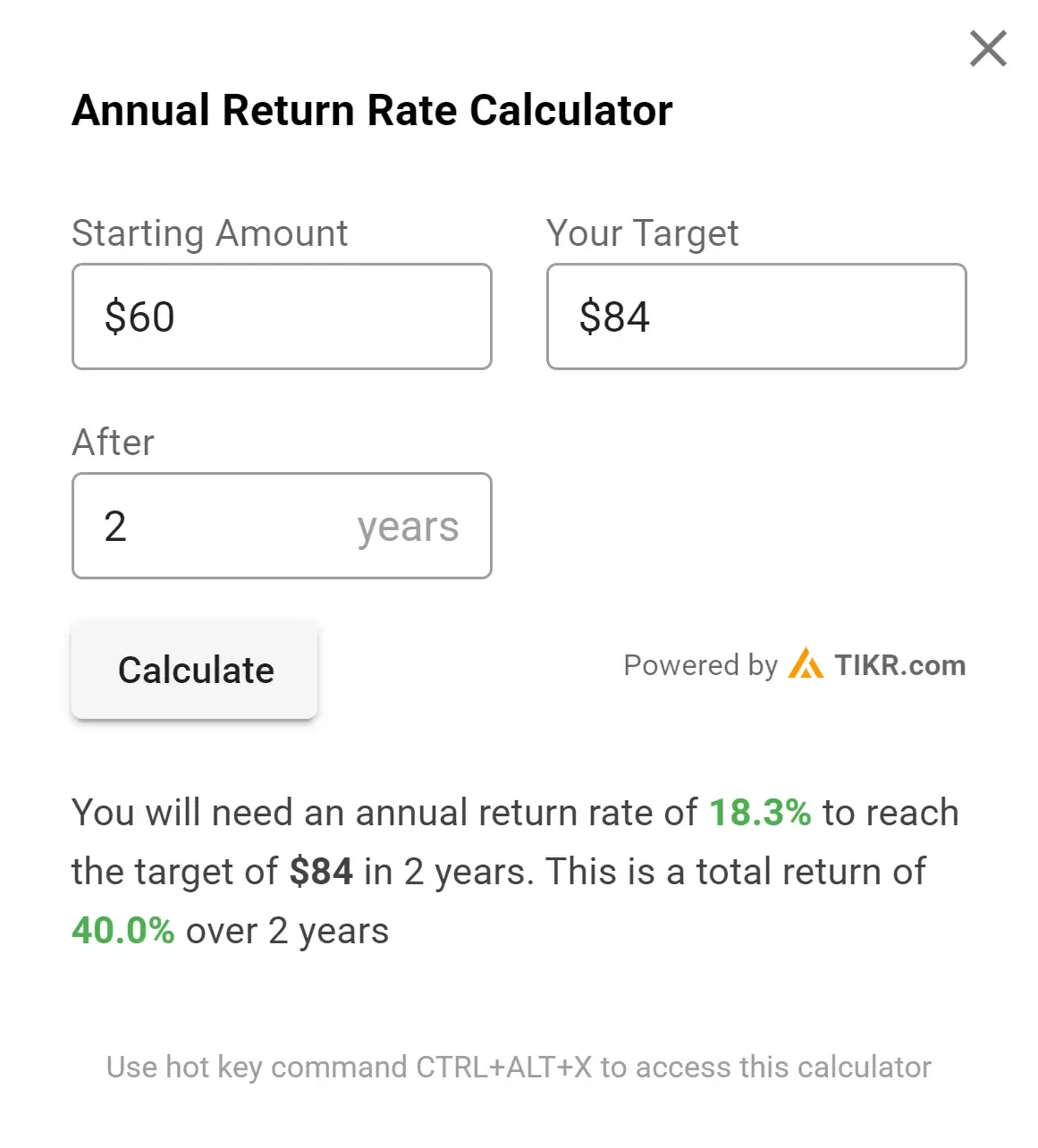

- The 2-Minute Valuation Model values SWK stock at $84 per share in 2 years.

- That’s a potential 40% upside from today’s share price of $60.

- Analysts expect Stanley Black & Decker’s earnings-per-share to grow a total of about 60% over the next three years.

- Get accurate financial data on over 100,000 global stocks for free on TIKR >>>

Stanley Black & Decker might be in the middle of a quiet turnaround.

The company has been cutting costs, reshaping its supply chain, and raising prices to offset tariffs, which make the stock look undervalued today.

Additionally, the stock offers a 5.4% dividend yield, which means investors are paid to wait for the turnaround.

Let’s examine why this stock might offer substantial upside for patient investors.

Find the best stocks to buy today with TIKR. (It’s free) >>>

What is the 2-Minute Valuation Model?

Three core factors drive a stock’s long-term value:

- Revenue Growth: How big the business becomes.

- Margins: How much the business earns in profit.

- Multiple: How much investors are willing to pay for a business’s earnings.

Our 2-Minute Valuation Model uses a simple formula to value stocks:

Expected Normalized EPS * Forward P/E ratio = Expected Share Price

Revenue growth and margins drive a company’s long-term normalized earnings per share (EPS), and investors can use a stock’s long-term average P/E multiple to get an idea of how the market values a company.

Why SWK Stock Looks Undervalued

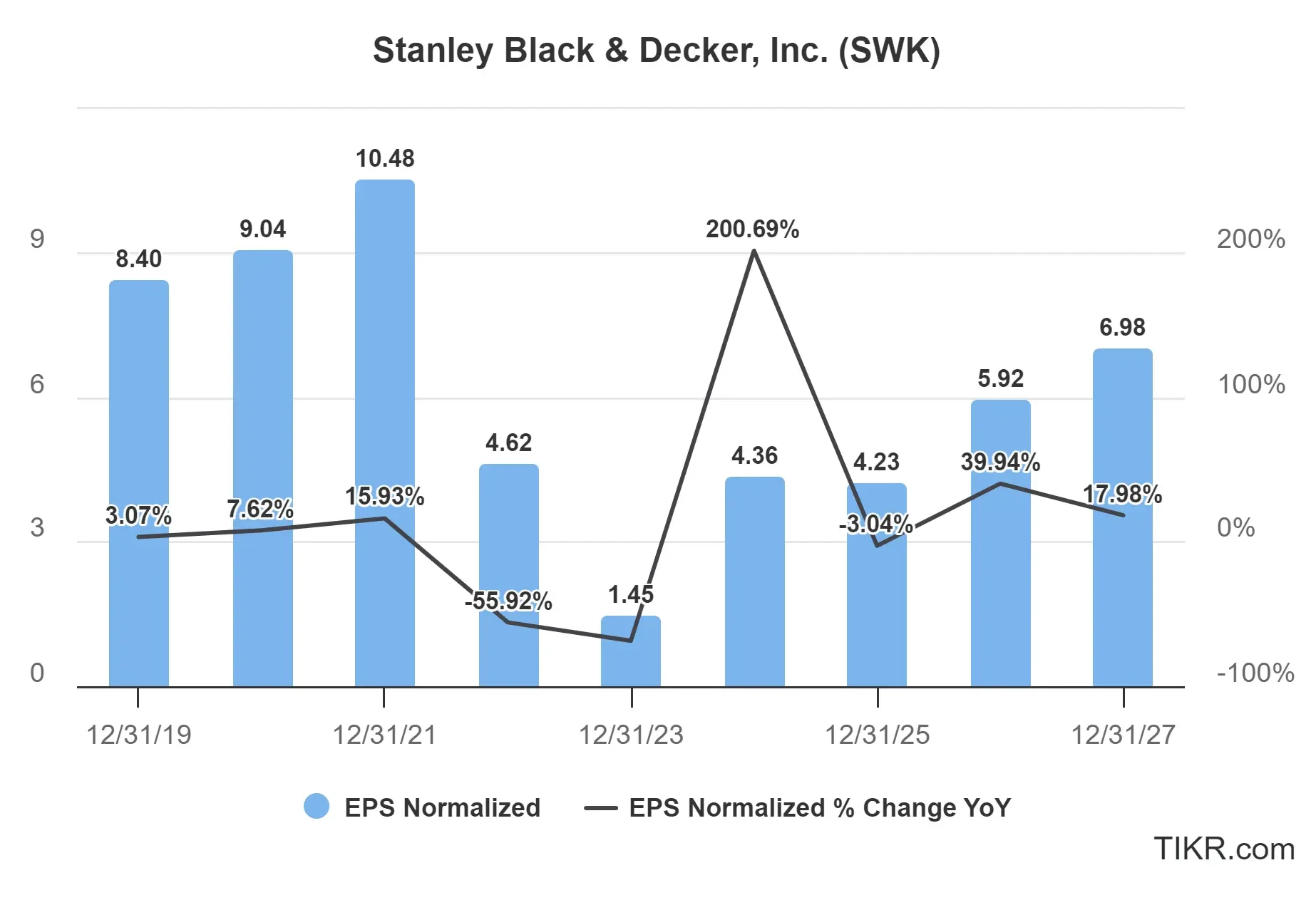

Forecast

Stanley Black & Decker is expected to see earnings recover over the next three years, with normalized EPS projected to increase from $4.36 in 2024 to $6.98 in 2027.

The company is executing a $2 billion cost-saving program aimed at enhancing operational efficiency and margins by the end of 2025. These measures, combined with targeted price adjustments, are positioning the company for sustained earnings growth despite current economic challenges.

This earnings growth for SWK stock is likely to be driven by:

- Recovery from Previous Challenges: The company has been working through inventory issues and cost pressures that impacted performance in recent years. As these headwinds dissipate, profit margins are expected to improve.

- Strong Brand Portfolio: Stanley Black & Decker owns some of the most recognized brands in the tool industry, including DEWALT, Craftsman, and BLACK+DECKER, giving it pricing power and customer loyalty.

- Housing Market Recovery Potential: Any recovery in housing construction and renovation activity would benefit SWK stock, as tools and hardware products represent a core part of their business.

- Cost-Cutting Initiatives: Management has implemented restructuring programs aimed at reducing costs and improving operational efficiency, which could accelerate earnings growth beyond current projections.

View Stanley Black & Decker’s full analyst estimates (It’s free) >>>

Is Stanley Black & Decker Stock Undervalued Right Now?

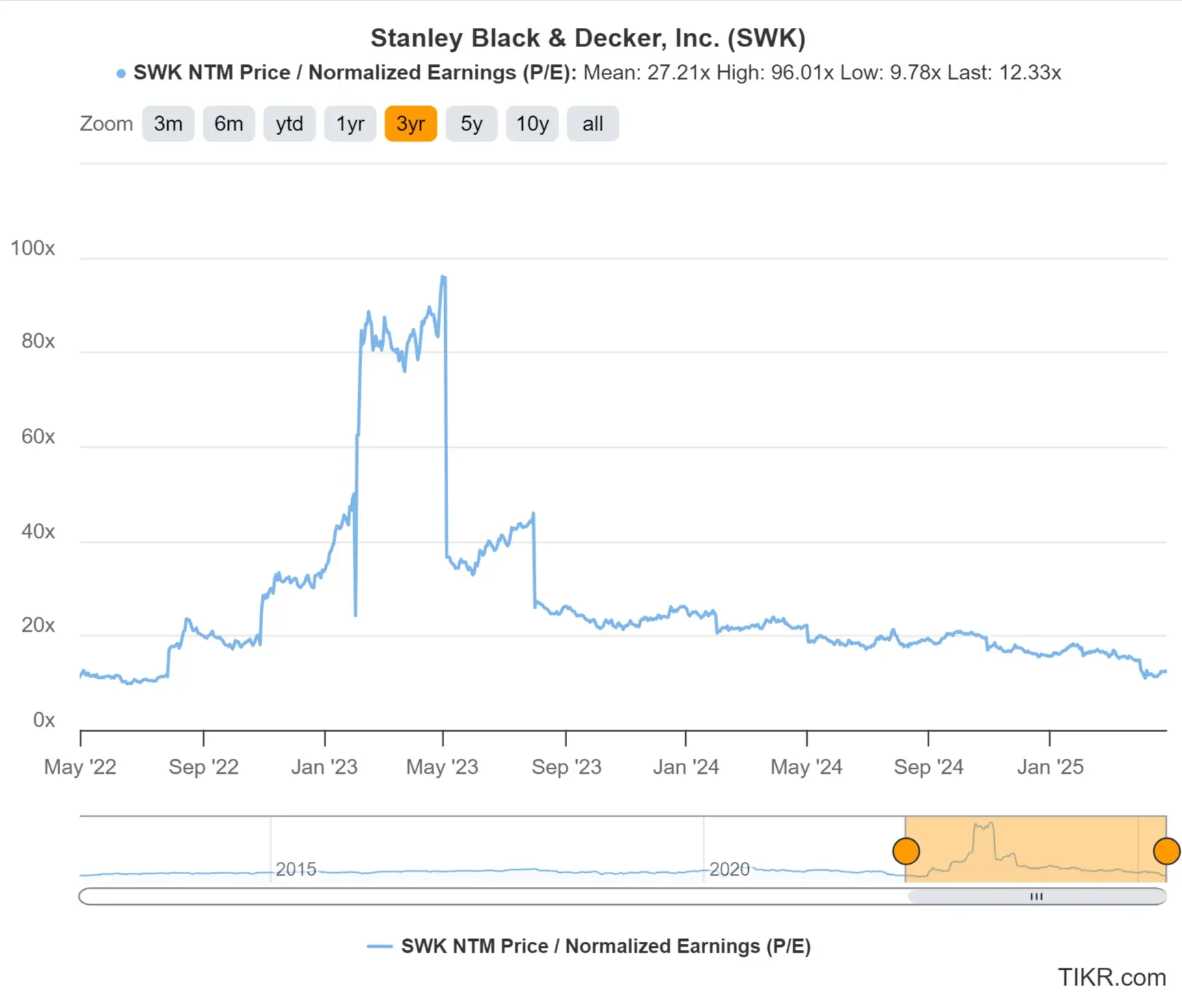

SWK stock is currently trading near the lower end of its historical valuation range, which means the stock could be undervalued if the company achieves its expected earnings growth.

We’ll use a conservative forward P/E of 12x for our valuation, which is in line with the stock’s current multiple. Even if the valuation multiple doesn’t expand in the future, the stock still looks undervalued today because earnings are expected to grow significantly in the coming years.

Fair Value of SWK Stock

Using our 2-Minute Valuation Model and applying a conservative approach:

- Conservative 2027 EPS estimate: $6.50

- Conservative forward P/E multiple: 12x

- Expected dividends over the next 2 years: $6

Expected Normalized EPS ($6.50) * Forward P/E ratio (12x) + Expected Dividends ($6) = Expected Share Price ($84)

The 2-year expected SWK stock price we would get from this valuation is $84 per share.

With SWK stock currently trading at around $60 per share, this implies that the stock could have a potential upside of about 40% over the next two years, which would be an 18% annualized return.

Keep in mind, this is just a valuation exercise, and we don’t know for sure what the stock’s price will be in the future.

Value stocks quicker with TIKR (It’s free, no card required) >>>

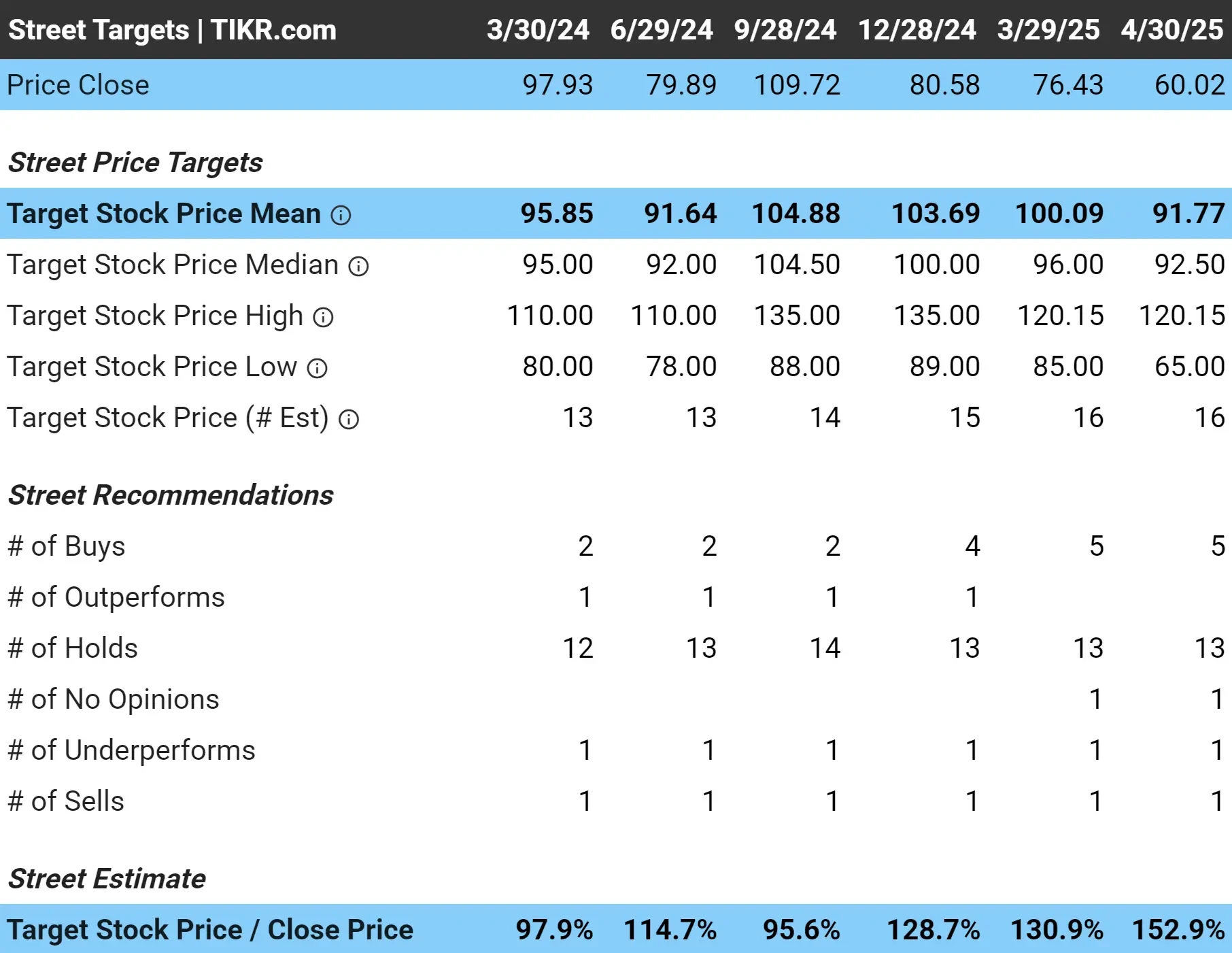

What is the Target Price for SWK Stock?

Analysts have an average price target of around $92 per share for SWK stock. That means they’re even more bullish on the stock, and see an average of about 53% upside from the stock’s current share price:

Risks to Consider

While our valuation suggests meaningful upside, investors should be aware of several risks:

- As a company that sources components globally, SWK could face margin pressure from increasing tariffs on imported goods, particularly from China.

- SWK’s products are tied to construction, renovation, and industrial activity, making it vulnerable to economic downturns.

- SWK faces intense competition from both traditional rivals and newer entrants, particularly in the battery-powered tool segment.

- The company has taken on significant debt for acquisitions in recent years, which could limit its financial flexibility if business conditions deteriorate.

TIKR Takeaway

Stanley Black & Decker offers an attractive combination of strong projected earnings growth, a historically low valuation multiple, and a 5.4% dividend yield today.

While the tool industry faces challenges from economic cycles and tariff concerns, SWK’s strong brand portfolio and path to improved earnings make it a worthy consideration for value and dividend-oriented investors.

Is SWK stock a buy over the next 24 months? Use TIKR to check the stock’s analyst price targets, growth forecasts, and see if the stock is undervalued today.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!