Key Stats for NVIDIA Stock

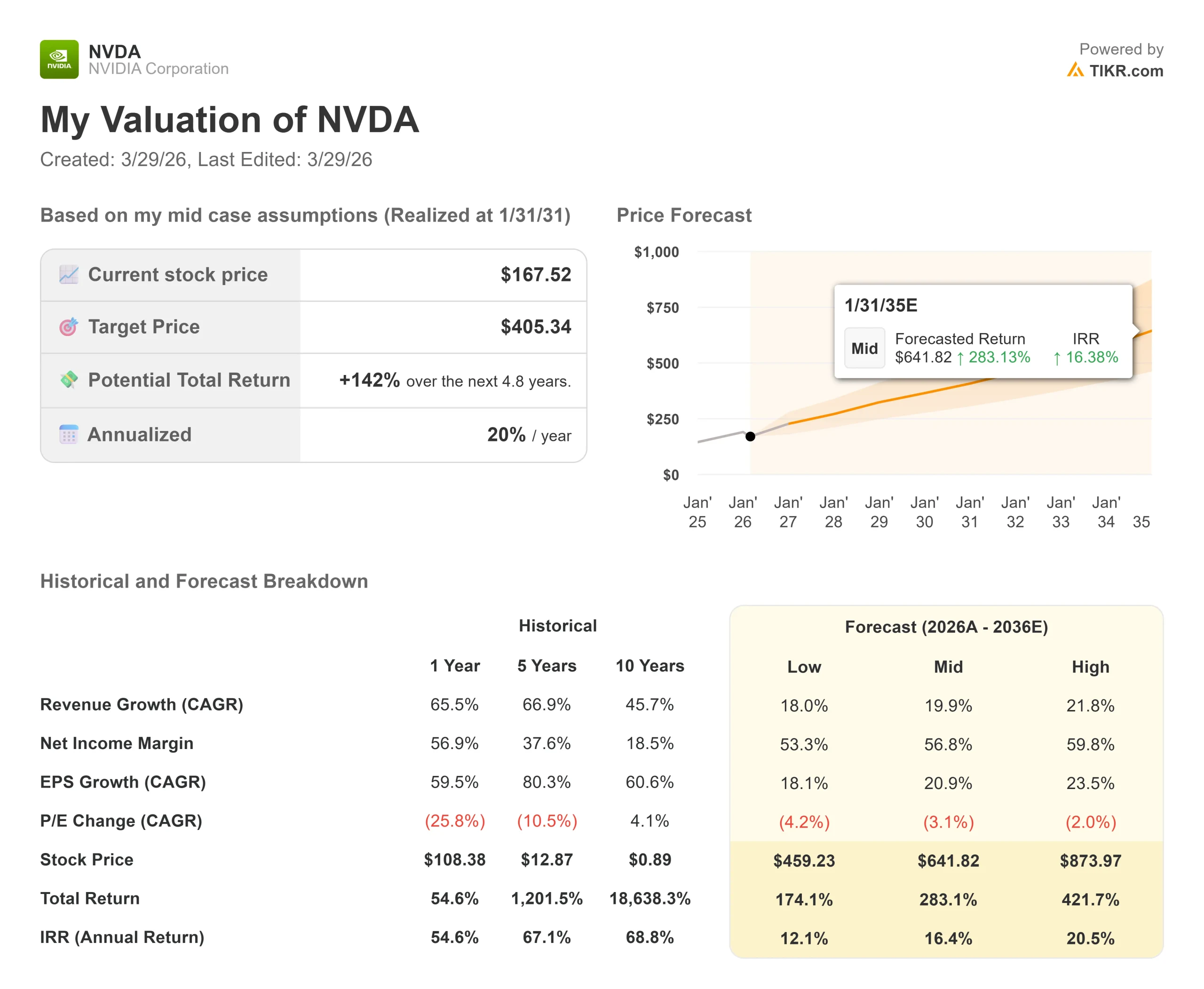

- Current Price: $167.52

- Target Price (Mid): $405.34

- Street Target: $268.22

- Potential Total Return: +142%

- Annualized IRR: 20.00% / year

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

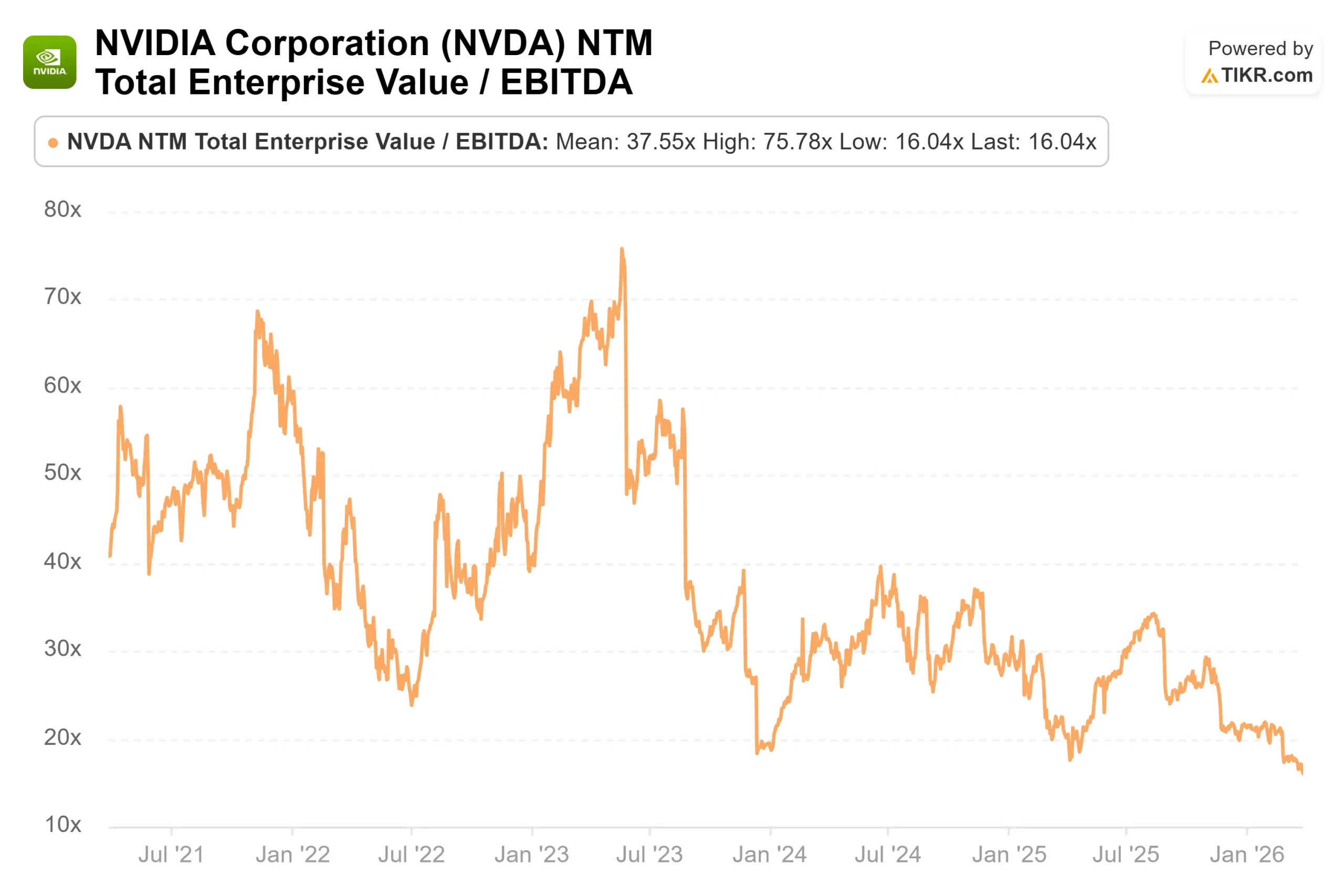

NVIDIA (NVDA) now trades at 20.20x next-twelve-months earnings, and NVIDIA’s forward P/E has dropped to about 20, near its lowest level in five years and below that of the S&P 500 index, the first time in 13 years the stock has traded at a discount to the index.

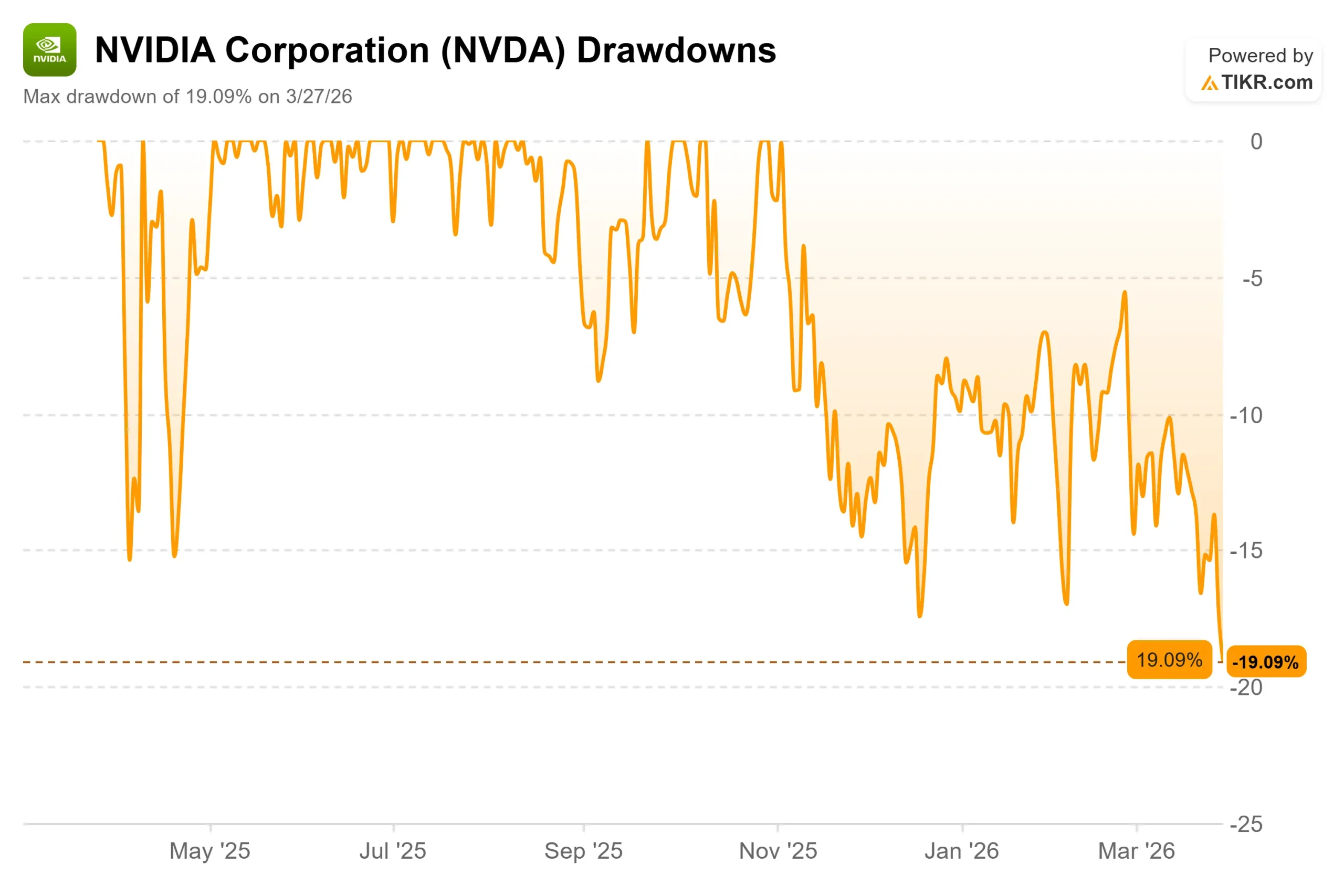

The stock has pulled back 19.09% from its all-time high and is down roughly 8% year to date, pressured by a broader tech selloff tied to the Iran conflict and rising interest rates.

Bulls argue the selloff is irrational given the demand picture. Bears point to the stock’s persistent failure to hold post-earnings gains.

The key unresolved question: is this the most asymmetric entry point in years, or can macro pressure keep NVDA pinned even as the business accelerates?

NVIDIA’s Q4 FY2026 revenue came in at $68.1 billion, up 73% year over year, with data center revenue of $62.3 billion ahead of the Street consensus.

GAAP EPS of $1.76 beat the average estimate of $1.47 by 19.57%, the fifth consecutive quarter of revenue beats. The stock fell 5.46% the next session regardless. For Q1 FY2027, management guided revenue of $78.0 billion, plus or minus 2%, explicitly excluding any data center compute revenue from China.

Two weeks later at GTC 2026, CEO Jensen Huang raised the stakes further.

Huang disclosed that NVIDIA now sees at least $1 trillion in purchase orders for Blackwell and Vera Rubin chips through end-2027, doubling the $500 billion figure he cited at the same conference a year earlier.

At the March 18 analyst session, Huang noted the figure excludes newer products, including Groq, stand-alone CPUs, and storage, meaning total revenue through 2027 is expected to run materially above the headline number.

Despite that, shares briefly spiked to session highs following the announcement before losing all gains and closing below where they were trading when the presentation began.

See historical and forward estimates for NVIDIA stock (It’s free!) >>>

Is NVIDIA Undervalued Today?

The valuation setup is hard to ignore.

At 20.20x NTM P/E and 16.04x NTM EV/EBITDA, NVIDIA is priced as though growth is about to decelerate, not accelerate into a $78 billion quarter. The Street consensus of $268.22 across 56 price target estimates implies 60% upside from the current price.

The product picture supports that conviction.

NVIDIA’s Vera Rubin system, comprising 1.3 million components, is designed to deliver 10 times more performance per watt than its predecessor, Grace Blackwell, a critical advance as energy consumption becomes one of the most pressing constraints on AI data center expansion.

At the March 18 analyst session, Huang explained that the Vera Rubin rack system expands the addressable revenue per deployment by adding CPUs, Groq language processing units (chips specialized for ultra-low-latency inference), and AI-native storage alongside the core GPU compute.

Goldman Sachs stated the $1 trillion demand guidance directly counters concerns that AI capital expenditure will peak in 2026, and noted the Groq integration can increase throughput per watt by 35 times for trillion-parameter models.

Wolfe Research reiterated an Outperform rating and $275 price target, calling Nvidia’s Rubin Ultra Pods a blueprint for agentic AI data centers.

The bear case centers on what surrounds the product.

The Iran conflict has weighed on the broader technology sector, contributing to multiple compressions across high-growth names, while rising interest rates could slow data center construction financing.

China’s export controls remain a structural constraint, and any further tightening would remove revenue with no offsetting gain.

On peer valuation, Broadcom trades at 17.98x NTM EV/EBITDA and AMD at 28.73x, both on a next-twelve-months basis per TIKR data.

NVIDIA at 16.04x trades at a discount to both, despite a meaningfully higher growth rate and stronger margins, with an LTM gross margin of 71.1% and an LTM operating margin of 60.4%.

That discount is either an opportunity or a signal that the market is pricing in a growth slowdown that has not yet appeared in the numbers.

See how NVIDIA performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

Key Stats:

- Current Price: $167.52

- Target Price (Mid): $405.34

- Potential Total Return: +142%

- Annualized IRR: 20.00% / year

See analysts’ growth forecasts and price targets for NVIDIA stock (It’s free!) >>>

The TIKR mid-case model applies a 19.9% revenue CAGR, driven by continued data center compute expansion as Vera Rubin and the subsequent Feynman architecture sustain a multi-year upgrade cycle, and by the broadening attach rate of CPUs, Groq-based inference products, and AI-native storage on each new rack deployment. The margin driver is a software and platform mix, with the mid case modeling a 56.8% net income margin as higher-margin software revenue grows as a share of total sales. The mid-case target of $405.34 per share, realized by January 2031, implies 20.00% annualized compounding from the current price.

The primary downside risk is a reacceleration of China export restrictions, a deceleration in hyperscaler capital expenditure, or faster-than-expected erosion of NVIDIA’s inference leadership by custom silicon from AMD, Broadcom, or hyperscaler-designed chips, any of which would compress both the growth rate and the multiple.

Conclusion: Watch data center revenue at NVIDIA’s next earnings report on May 27, 2026. If it comes in at or above $72 billion against the $78 billion total guidance midpoint, it confirms the Vera Rubin ramp is on track and that non-China demand is absorbing the export control gap. A miss on that line reopens the duration debate regardless of the headline number.

NVIDIA is growing revenue at 73% annually, guiding $78 billion for its next quarter, carrying $1 trillion in confirmed demand through 2027, and trading below the S&P 500’s forward multiple for the first time in 13 years. The May 27 report is where the market’s skepticism gets tested.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in NVIDIA?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up NVIDIA, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track NVIDIA alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!