Key Stats for Extra Space Storage Stock

- Past-Week Performance: -1%

- 52-Week Range: $122 to $155.2

- Current Price: $129

What Happened?

Extra Space Storage (EXR), the Salt Lake City-based self-storage REIT owning 4,281 properties nationwide, logged its first positive same-store revenue quarter in over a year at +0.4%, while Q4 core FFO, the recurring cash earnings measure REITs use instead of net income, rose 2.5% to $2.08 per share against a $145.18 stock that has since pulled back to $128.96.

On February 19, Extra Space reported Q4 core FFO of $2.08 per share, beating the LSEG analyst consensus of $2.04, while guiding full-year 2026 core FFO to $8.05 to $8.35, a range whose midpoint sits one cent below the Street’s $8.21 estimate.

New customer move-in rates, the leading indicator of future rent roll health, turned positive in 16 of the company’s top 20 markets in Q4 versus only 2 of 20 a year earlier, a recovery pace that peers including Public Storage have not publicly matched at the same scale.

Chief Executive Officer Joe Margolis stated on the Q4 2025 earnings call that “we feel better with regard to our positioning going into 2026 than we did heading into 2025, and in our ability to gradually accelerate performance as fundamentals continue to improve through 2026,” grounding that confidence in mid-February occupancy holding at 92.5% with new customer rates running more than 6% above the prior year.

Additionally, last January 5, Extra Space promoted Noah Springer to President to oversee operations alongside his existing strategy role, a leadership move that coincides with Barclays raising its EXR price target to $170 on March 5 citing scale advantages and data capabilities as structural differentiators.

The company’s $1.5 billion bridge loan portfolio, a lending platform that finances third-party storage operators and feeds EXR’s acquisition pipeline, a third-party management base of 1,856 stores, $149.5 million in share repurchases completed in 2025, and incremental supply reduction across Sunbelt markets collectively position Extra Space to convert its rate momentum into accelerating NOI growth as the next leasing season unfolds.

Wall Street’s Take on EXR Stock

The positive same-store revenue inflection reported February 19, the first in over a year, signals that EXR’s largely fixed-cost storage portfolio is approaching the operating leverage point where modest top-line recovery drives outsized margin expansion.

EXR’s EBITDA is estimated by TIKR to grow 9.3% to $2.41 billion in 2026, as property tax normalization, confirmed by management on the Q4 call, and a 5%-plus drop in utility costs convert modest same-store revenue recovery into outsized margin expansion from 76.1% to 81.3%.

Wall Street’s conviction is building but cautious: 6 buys, 3 outperforms, 11 holds, and 1 underperform across 20 analysts yield a mean price target of $152.85, implying 18.5% upside from the current $128.96 as analysts await confirmation from the spring leasing season before upgrading.

The analyst target range of $140 to $178 tells the real story: the low end prices in continued LA County pricing restrictions and a weak leasing season, while the high end reflects move-in rate momentum accelerating through the rent roll into second-half same-store NOI growth.

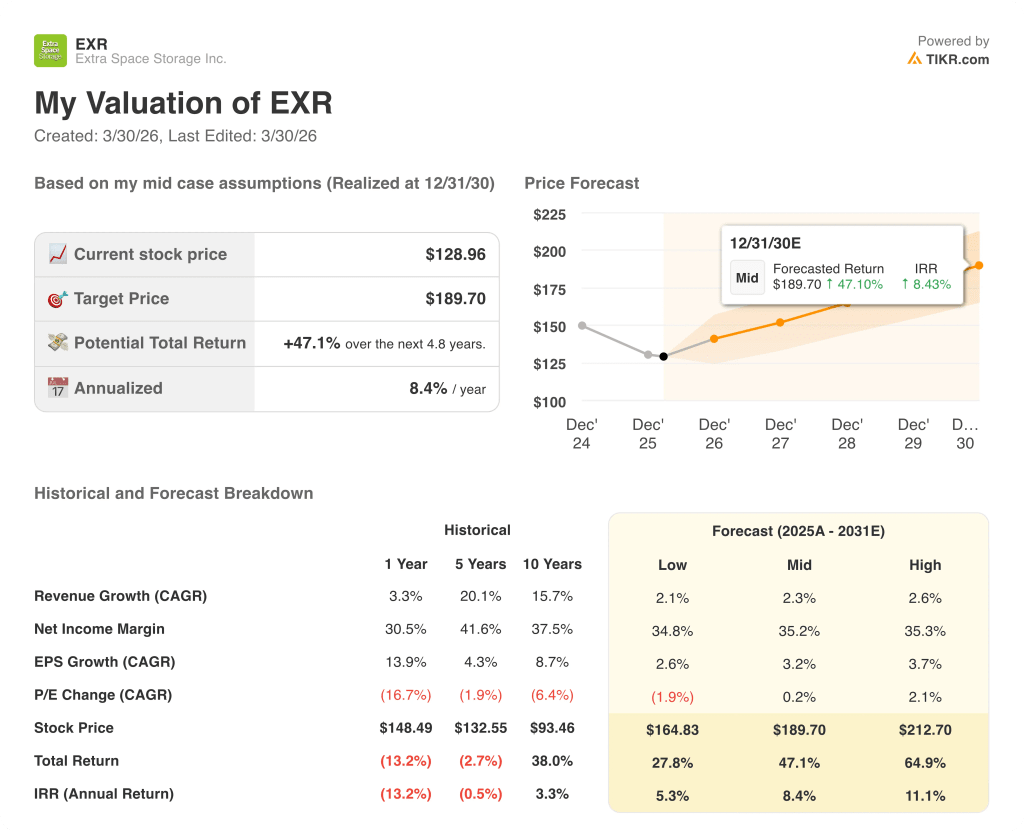

What Does the Valuation Model Say?

The TIKR mid-case model prices EXR at $189.70 by December 2030, implying a 47.1% total return at an 8.4% annual IRR, anchored by 2.3% revenue CAGR and net income margins expanding toward 35.2% as the fixed-cost platform absorbs demand recovery without proportional expense growth.

The market is pricing EXR at 0.86x NAV per share against a Street NAV estimate of $149.28, treating a recovering REIT as if its asset base has permanently deteriorated, which the 16-of-20-market move-in rate data directly contradicts.

Move-in rates running more than 6% above prior-year levels as of mid-February confirm that the rent roll, which turns over only 5% to 6% monthly, is filling with higher-rate customers, the precise input the TIKR model’s $189.70 target requires to materialize.

CEO Joe Margolis’s February 20 statement that new customer rates have been positive for “a number of months” and occupancy held at 92.5% mid-February signals the trough is behind EXR, not still ahead, a distinction the current price has not priced in.

The New York City lawsuit filed February 10, seeking more than $5 million in penalties across 60 properties, represents a contained but real regulatory risk: if municipalities broaden pricing-restriction legislation beyond LA County, the TIKR model’s 81.3% EBITDA margin assumption faces compression.

Q1 2026 same-store revenue, expected with first-quarter results, is the number to watch: any acceleration beyond the Q4 exit rate of +0.4% confirms that move-in rate gains are flowing into the rent roll and that the TIKR mid-case recovery path is on track.

Should You Invest in Extra Space Storage Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up EXR stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Extra Space Storage Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze EXR stock on TIKR for Free →