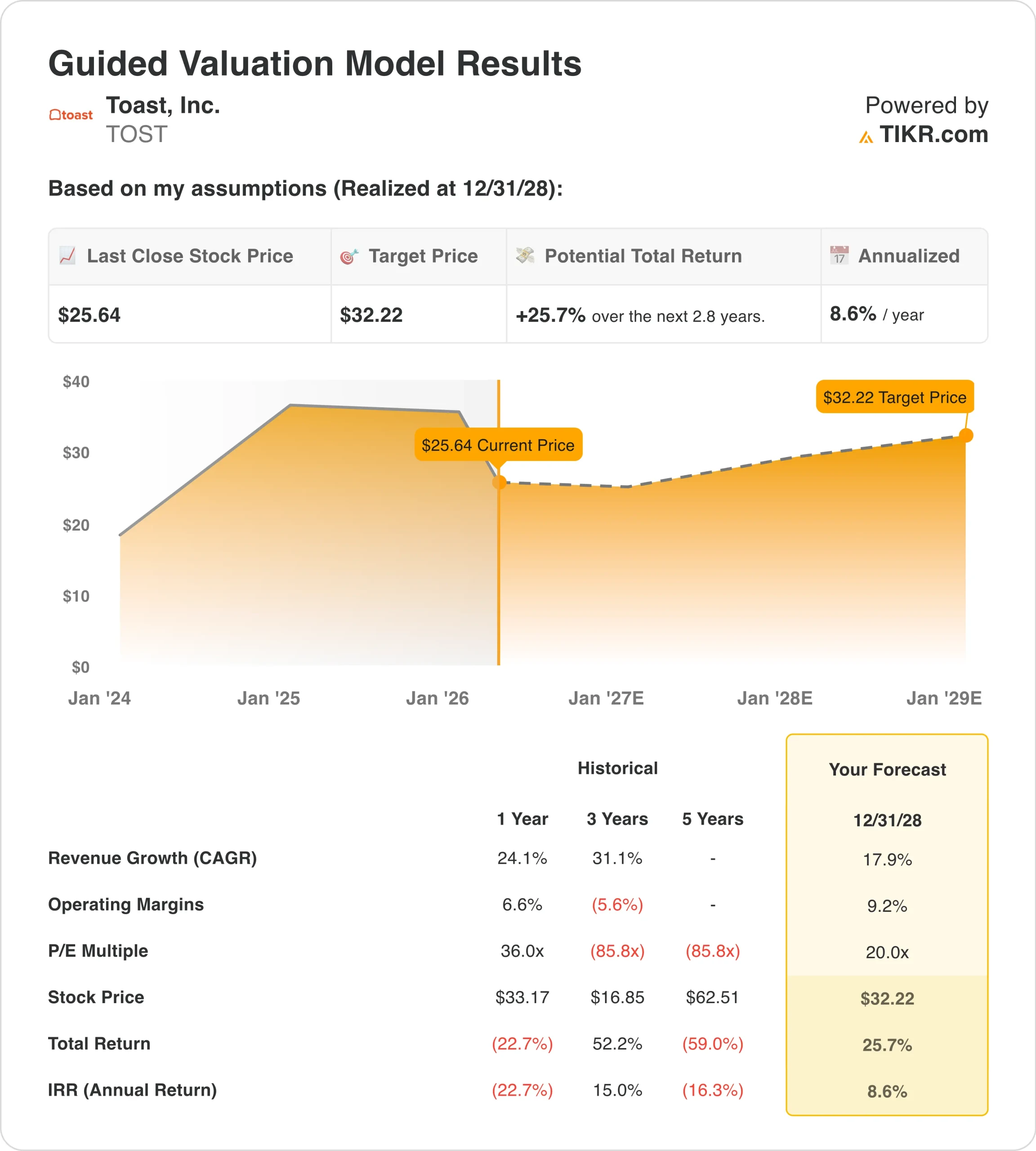

Key Stats for TOST Stock

- Past week’s performance: -7%

- 52-week range: $24 to $50

- Valuation model target price: $32

- Implied upside: 25.7% over 2.8 years

Value your favorite stocks like TOST with 5 years of analysts’ forecasts using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Toast, Inc. (TOST) stock fell about 7% over the past week, and the move came without a major new negative operating update. That matters because the market still seems to be repricing the company after its February earnings report and softer near-term outlook. The stock also traded during a rough stretch for growth and software names, as broader risk appetite weakened again.

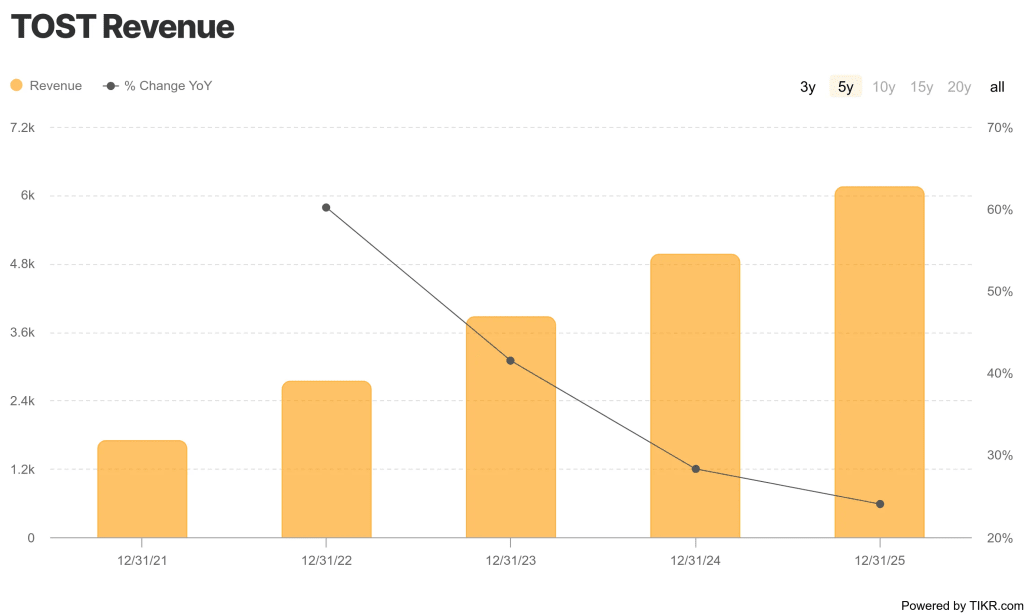

The core business story itself was still solid. Toast reported full-year 2025 revenue of $6.2 billion, up 24.1%, while gross profit rose 33.7% to $1.6 billion and operating income improved to $305 million.

Toast also said it added a record 30,000 net locations in 2025, including about 8,000 in the fourth quarter, which shows the restaurant platform kept expanding even as investors turned more cautious on the stock.

Still, investors were not focused only on what Toast had already delivered. Management guided for first-quarter 2026 adjusted EBITDA of $160 million to $170 million and full-year adjusted EBITDA of $775 million to $795 million, so the market had to weigh strong current execution against a more measured profit outlook. That helps explain why shares stayed under pressure even after revenue beat expectations in the fourth quarter.

Recent company news was mixed but not dramatic enough to fully change sentiment. Toast announced a strategic partnership with Instacart on February 10, and it later said Teriyaki Madness would roll out Toast’s enterprise platform across more than 200 U.S. locations. But investors appear to be waiting for proof that these wins can translate into faster recurring profit growth, not just more headlines.

See analysts’ growth forecasts and price targets for TOST (It’s free) >>>

Is TOST Stock Undervalued?

Under valuation model assumptions realized through 12/31/28, the stock is modeled using:

- Revenue growth (CAGR): 17.9%

- Operating Margins: 9.2%

- Exit P/E Multiple: 20x

Based on these inputs, the model estimates a target price of $32.22, implying 25.7% total upside from the current share price and a 8.6% annualized return over the next 2.8 years.

The valuation setup suggests moderate upside, but not a screaming bargain. A target price of $32.22 is only about 25.7% above the current share price, and the implied annual return is 8.6%, which is below the double-digit threshold many long-term investors look for. So the model points more to a reasonable value than to a deeply discounted stock.

The growth assumptions are not aggressive relative to Toast’s recent history. Based on analysts’ consensus estimates, we uses 17.9% revenue growth, while Toast just grew revenue 24.1% in 2025 and raised total ARR 26% to over $2.0 billion. That means the bigger debate is less about whether Toast can grow and more about how much of that growth can convert into durable margin expansion.

Margins are the key swing factor in the story. Toast’s LTM EBIT margin is 5.0%, while the model assumes 9.2%, and that is plausible because the company already moved from an operating loss of $287 million in 2023 to an operating income of $305 million in 2025. It also generated $661 million in operating cash flow and $608 million in free cash flow in 2025, so the business is now producing real cash, not just growth.

The multiple also looks more grounded than it once did. The model uses a 20.0x exit P/E, versus a current LTM P/E of 45.8x in your snapshot, so it assumes some multiple compression even if the business keeps improving. That is why the stock can look somewhat undervalued on operations, but still not offer extraordinary modeled returns from here.

What’s Driving the Toast Stock Going Forward?

The next major catalyst is first-quarter 2026 earnings, expected on May 8. Management has already told investors to expect first-quarter non-GAAP subscription services and financial technology solutions gross profit of $505 million to $515 million and adjusted EBITDA of $160 million to $170 million. That report will matter because investors want to see whether Toast can keep growing while also widening profitability.

Location growth remains one of the biggest drivers. Toast ended 2025 with roughly 164,000 locations, and CEO Aman Narang said the company has “momentum across the business” as it scales its core restaurant business, expands in new markets, and increases platform adoption.

Partnerships could help support that expansion. The Instacart tie-up is designed to create a “unified local shelf” that syncs in-store inventory with Instacart’s marketplace, and that could make Toast’s platform more useful for restaurants and hybrid merchants. The Teriyaki Madness rollout matters too, because larger chains can lift payment volume, software usage, and brand credibility faster than small independent accounts.

The market will also keep watching sentiment around software stocks more broadly. Reuters reported in March that software companies were still pushing back against fears that advanced AI tools could weaken traditional software models, and that backdrop has made investors more selective across the sector. So Toast’s next move will likely depend on both company execution and whether growth software names regain favor.

Estimate a company’s fair value instantly (Free with TIKR) >>>

Should You Invest in Toast, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up TOST, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track TOST alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Toast stock on TIKR Free→

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!