Key Stats for Unity Software Stock

- Past-Week Performance: +5.8%

- 52-Week Range: $15.3 to $52.2

- Current Price: $19.5

What Happened?

Unity Software (U), a videogame engine maker now pivoting into AI-powered advertising, beat its own Q1 2026 revenue guidance by as much as $28M before the quarter even closed, with preliminary results of $505M–$508M landing well above both the prior $480M–$490M outlook and the $488.9M analyst consensus.

On March 26, Unity released preliminary Q1 figures showing adjusted EBITDA of $130M–$135M, crushing its own $105M–$110M guidance by roughly 24% at the midpoint, driven by a 48% surge in Strategic Grow revenue, which strips out the legacy ironSource ad network and Supersonic game publishing unit being divested.

The operational proof behind that beat is Vector, Unity’s AI-driven mobile ad platform that matches game publishers with players most likely to convert, which delivered its third straight quarter of mid-teen sequential growth in Q4 2025 and hit a new January 2026 revenue record 72% above the prior-year period, a pace that puts it on track for a $1B annualized quarterly run rate by year-end.

On the April 30 sunset of the ironSource Ads Network, a commoditized legacy ad network Unity acquired and is now winding down, CEO Matt Bromberg stated on the Q4 2025 earnings call that “we are displacing commoditized lower-margin ad network revenue for deeply differentiated AI platform revenue,” a shift the company expects to structurally expand both growth rates and margins across its advertising business.

Unity’s path to competitive relevance rests on three converging catalysts: the integration of runtime engine behavioral data into Vector’s AI model in Q2 2026, the general availability of its in-app commerce tools in Q2 2026, and the browser-based authoring environment launching in 2026 that expands Unity’s addressable market well beyond its core software developer base.

Wall Street’s Take on U Stock

Unity’s Q1 2026 EBITDA beat of roughly 24% above its own guidance confirms the margin inflection already underway, as the ironSource wind-down removes drag on the Grow segment’s contribution margin.

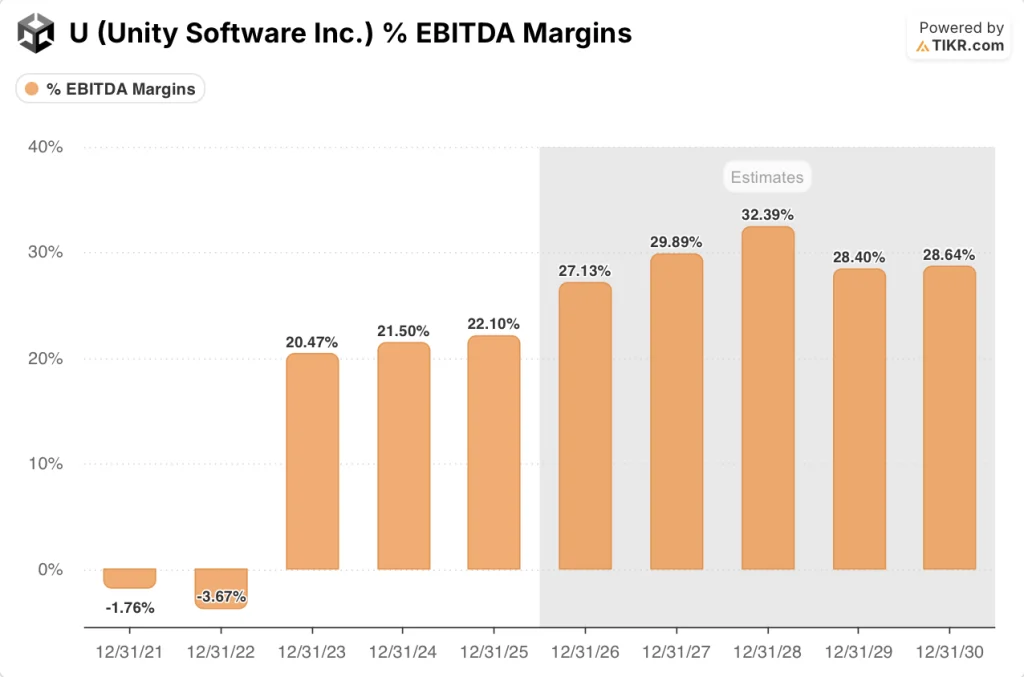

TIKR estimates EBITDA margins expanding from 22.1% in 2025 to 27.1% in 2026 and 32.4% by 2028, driven by Vector’s high-contribution AI ad revenue displacing the commoditized ironSource network sunsetted April 30.

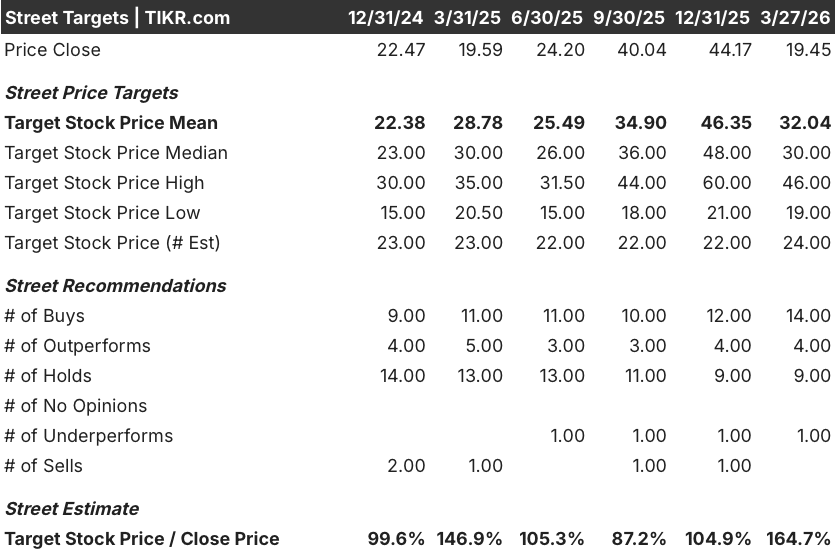

Wall Street’s posture has shifted decisively bullish: 14 buys, 4 outperforms, 9 holds, and 1 underperform among 28 analysts, with a mean price target of $32.04, implying 64.7% upside from the March 27 close of $19.45.

The analyst target range spans $19.00 to $46.00, with the low anchored to execution risk on Vector’s runtime data integration and the high contingent on Strategic Grow revenue sustaining its 48% YoY momentum through 2026.

What Does the Valuation Model Say?

TIKR’s mid-case price target of $37.44, implying 92.5% total return and a 14.7% IRR over 4.8 years, assumes a 13.1% revenue CAGR and net income margins reaching 24.4%, justified by Vector’s $1B annualized quarterly run rate target and the FCF-generative simplification of removing two legacy business lines.

The market appears to be pricing Unity as a declining game engine company, ignoring that free cash flow grew 41% in 2025 to $400M and TIKR estimates FCF margins expanding from 21.8% to 25.7% in 2026.

Vector’s January 2026 revenue, 72% above the prior year and a new monthly record, is the specific operational data point justifying TIKR’s 13.1% revenue CAGR assumption and the $37.44 mid-case target.

CEO Matt Bromberg’s statement that the company sees “no natural ceiling” to Vector’s growth predates runtime engine behavioral data entering the ad model in Q2 2026, the single most significant unpriced catalyst.

Runtime data integration into Vector in Q2 2026 is the key model assumption: if opt-in rates fall below the current above-90% threshold or behavioral signal quality disappoints, the margin expansion timeline slips materially.

The Q2 2026 earnings call is the event to watch, specifically whether Vector sequential growth accelerates beyond the guided 10% Q1 rate once runtime data enters the model and ironSource revenue reaches zero.

Should You Invest in Unity Software Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up U stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Unity Software Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze U stock on TIKR for Free →