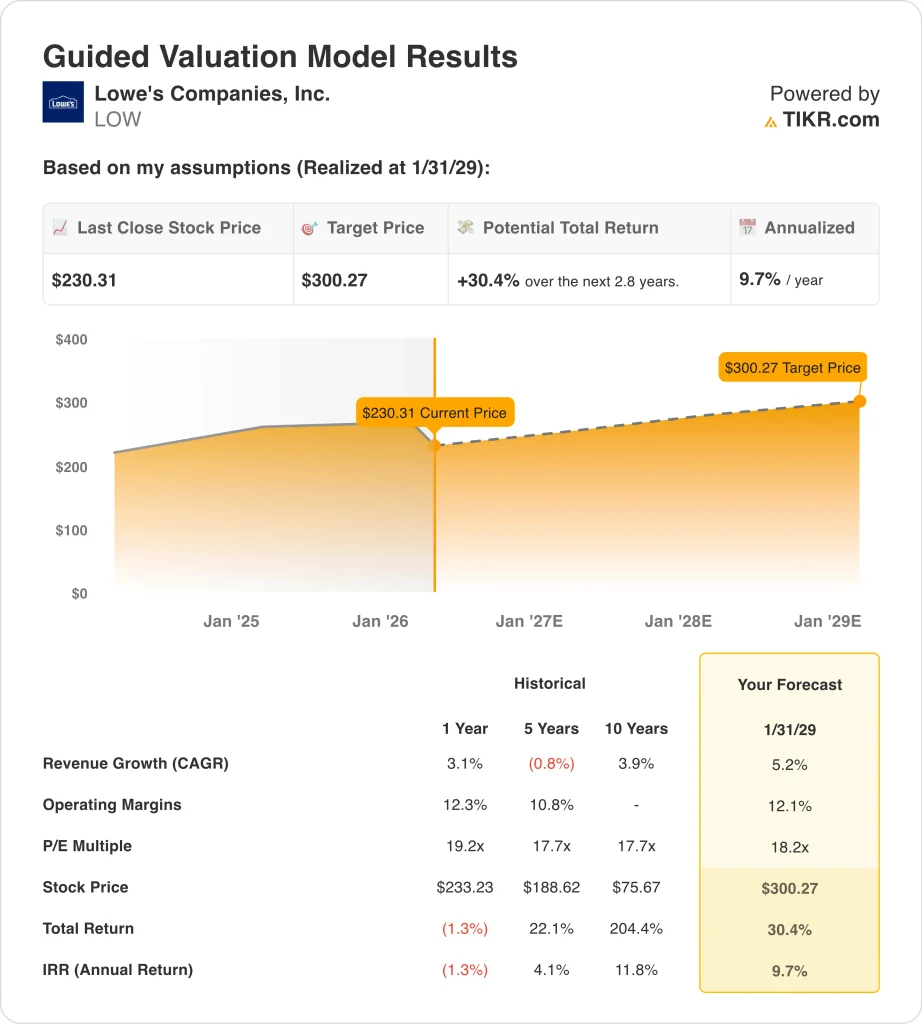

Key Stats for LOW Stock

- Past week’s performance: -1.7%

- 52-week range: $206 to $293

- Valuation model target price: $300

- Implied upside: 30.4% over 2.8 years

Value your favorite stocks like LOW with 5 years of analysts’ forecasts using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Lowe’s Companies, Inc. (LOW) stock slipped 1.7% this week, and the move came without a new earnings shock. The company stayed in the news because Reuters reported fiscal 2025 net earnings fell 4.4% to $6.7 billion. It also declared its next $1.20 quarterly cash dividend, which kept attention on shareholder returns rather than a new growth catalyst.

The bigger setup still comes from late February. Lowe’s beat fourth-quarter expectations with adjusted EPS of $1.98 and posted 1.3% comparable sales growth, but it also gave a cautious 2026 outlook. Reuters said the market focused on delayed big-ticket remodels, a sluggish housing backdrop, and softer consumer spending.

Management is still showing pockets of strength. In the Q4 release, Lowe’s said comparable sales were driven by continued growth in Pro, online, and home services sales, and Marvin Ellison said the company’s Total Home strategy is resonating with both Pro and DIY customers. The Q4 earnings call also said online sales grew 10.5% in the quarter, which shows digital demand is still helping the model.

Even so, sentiment remains tied to housing. Reuters said Home Depot held its forecast partly because its professional contractor business was stronger, while Lowe’s outlook came in more cautiously. So this week’s stock move looked less like a reaction to fresh bad news and more like investors still digesting a slower home-improvement cycle.

See analysts’ growth forecasts and price targets for LOW (It’s free) >>>

Is LOW Stock Undervalued?

Under valuation model assumptions realized through 12/31/28, the stock is modeled using:

- Revenue growth (CAGR): 5.2%

- Operating Margins: 12.1%

- Exit P/E Multiple: 18.2x

Based on these inputs, the model estimates a target price of $300, implying 30.4% total upside from the current share price and a 9.7% annualized return over the next 2.8 years.

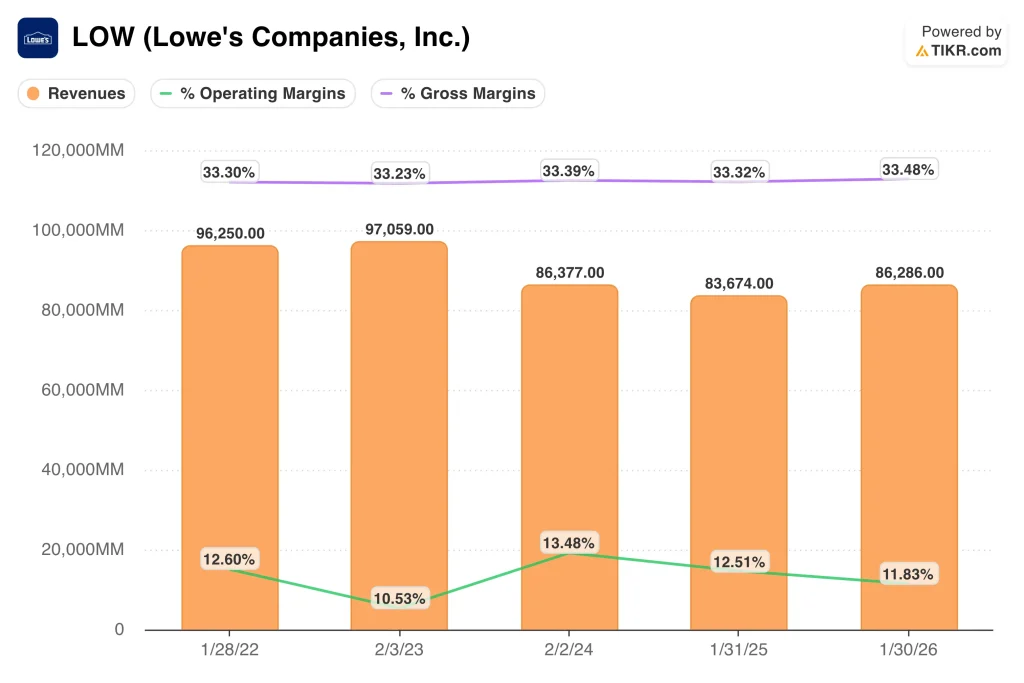

Those assumptions are fairly measured for a mature retailer. Lowe’s generated $86.3 billion of revenue in fiscal 2025, and gross margin held at 33.5%. Operating margin was 11.8%, so the model is not asking for a dramatic turnaround.

The debate is really about growth quality. Same-store sales rose just 0.2% in fiscal 2025, and Lowe’s said 2026 comparable sales should be flat to up 2%. That means the valuation case depends on steady execution in Pro, online, and services rather than a sharp rebound in discretionary DIY spending.

Cash generation still supports the stock. Free cash flow was about $7.7 billion in fiscal 2025, and Lowe’s paid $2.6 billion in dividends during the year. But leverage is meaningful too, with LTM net debt near $43.7 billion, so the market is balancing dependable cash returns against a slower growth profile.

Relative valuation also looks reasonable, not distressed. Lowe’s trades around 18.3x NTM earnings, while the model uses an 18.2x exit P/E multiple. That suggests the shares are priced more like a steady compounder than a deep-value turnaround, which fits a business still waiting for stronger housing

What’s Driving the LOW Stock Going Forward?

The next major catalyst is fiscal Q1 2027 earnings on May 18. Investors will want to see whether spring demand improved and whether professional customers stayed resilient. After Q4, Lowe’s said fiscal 2026 sales should be $92 billion to $94 billion, with an adjusted operating margin of 11.6% to 11.8%.

Management is staying focused on execution. Ellison said, “While the housing macro remains pressured, we are focused on directing what is within our control,” and added that Lowe’s is confident it can take share regardless of the macro environment. That matters because investors want proof that company-specific gains can offset a weak remodeling backdrop.

Professional customers remain a key driver. On the earnings call, Lowe’s said it delivered another quarter of growth in Pro and is expanding its Pro salesforce to win new accounts and deepen wallet share. That is important because Pro demand is usually greater, stickier, and more tied to recurring repair and maintenance work.

Supply-chain and service improvements could help, too. Reuters said Lowe’s expanded its partnership with Relex Solutions to strengthen supply-chain agility, and the company continues to push home services and fulfillment options. So the next move in the stock will likely depend on whether those operating improvements can translate into better comps before the housing market fully recovers.

Estimate a company’s fair value instantly (Free with TIKR) >>>

Should You Invest in Lowe’s Companies, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up LOW, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track LOW alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Lowe’s Companies stock on TIKR Free→

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!