Key Stats for American Tower Stock

- Past-Week Performance: -4.11%

- 52-Week Range: $165.1 to $234.3

- Current Price: $168.9

What Happened?

American Tower (AMT), the world’s largest independent wireless tower and data center landlord, delivered full-year 2025 attributable AFFO per share growth of 8% while trading near its 52-week low of $165.08, roughly 28% below its 52-week high of $234.33, as DISH Wireless defaulted on a Strategic Collocation Agreement signed in March 2021, stripping approximately $200 million in annual U.S. revenue from the run rate heading into 2026.

The Q4 2025 earnings report, released February 24, confirmed total revenue of $2.74 billion against an IBES estimate of $2.69 billion, with adjusted EBITDA of $1.82 billion beating consensus by $40 million, while the board simultaneously declared a $1.79 quarterly distribution payable April 28, a 5.3% sequential increase from the prior $1.70 per share.

CoreSite, AMT’s U.S. colocation and interconnection data center business that connects enterprises directly to major cloud providers, posted roughly 14% revenue growth in 2025, its fourth consecutive record sales year, while the company guided to 13% data center growth in 2026 and committed over $700 million in success-based data center CapEx, a figure that compares favorably against tower-only REITs that carry no equivalent high-yield reinvestment optionality.

On March 9, CFO Rodney Smith stated at the Deutsche Bank 34th Annual Media, Internet and Telecom Conference that “our data center platform continues to perform exceptionally well, growing in the double-digit range,” tying directly to CoreSite’s AI inferencing demand, which management identified as the fastest-growing new customer use case entering 2026.

AMT’s 200 to 300 basis point tower cash EBITDA margin expansion target through 2030, $1.6 billion in remaining board-authorized buyback capacity, and CoreSite’s mid-teens stabilized returns on new deployments collectively position the company to re-accelerate AFFO per share growth well above 2026’s DISH-suppressed ~1% pace, with management explicitly targeting industry-leading AFFO per share growth beginning in 2027.

Wall Street’s Take on AMT Stock

The DISH default, which stripped roughly $200 million in annual U.S. revenue and compressed 2026 AFFO per share growth to approximately 1%, has pushed AMT’s stock near its 52-week low despite the underlying business accelerating on every other dimension.

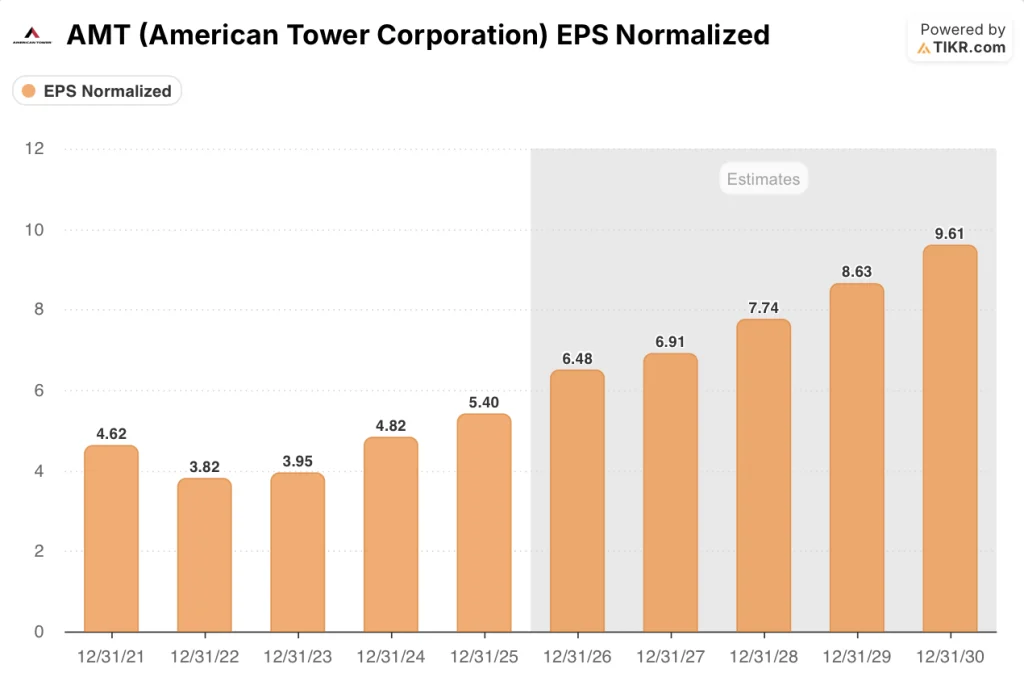

AMT’s normalized EPS is estimated to grow 20% in 2026, from $5.4 to $6.48, driven by CoreSite’s 13% guided data center revenue growth, a 5% dividend increase to approximately $3.3 billion in distributions, and over $700 million in high-return data center CapEx generating mid-teens stabilized yields.

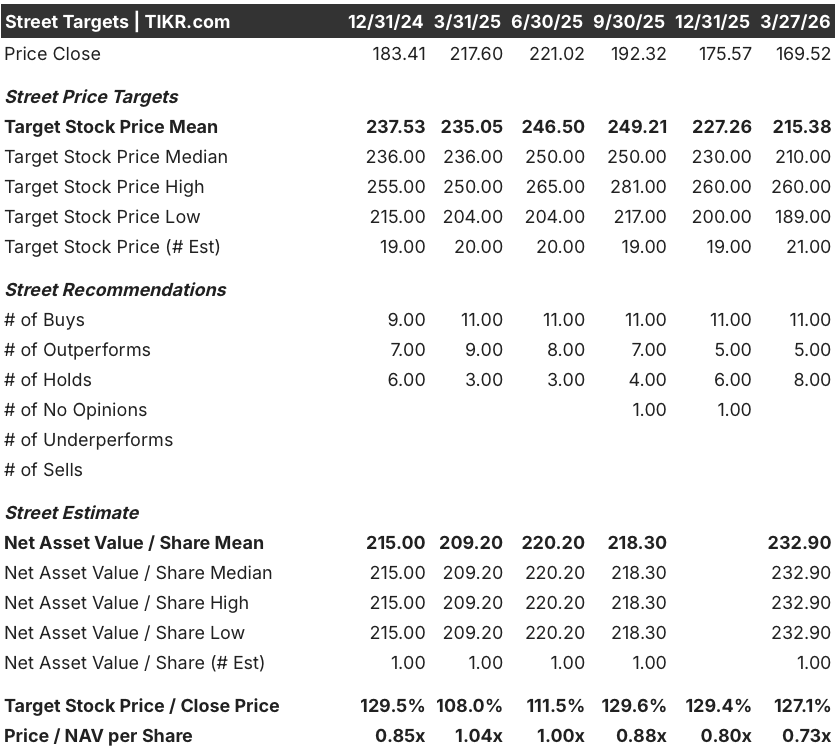

Analysts covering AMT are overwhelmingly constructive: 11 buys, 5 outperforms, and 8 holds among 21 analysts set a mean price target of $215.38, implying 27.1% upside from the current $169.52, with targets anchored to AMT’s 2027 re-acceleration thesis once DISH churn rolls off the base.

The spread between the $189 low target and the $260 high target reflects two divergent readings of the same story: bears anchor to DISH litigation uncertainty and Latin America churn reaching approximately -3% organic tenant billings growth in 2026, while bulls price in the CoreSite AI inferencing wave and a return to mid-single-digit U.S. organic growth in 2027.

What Does the Valuation Model Say?

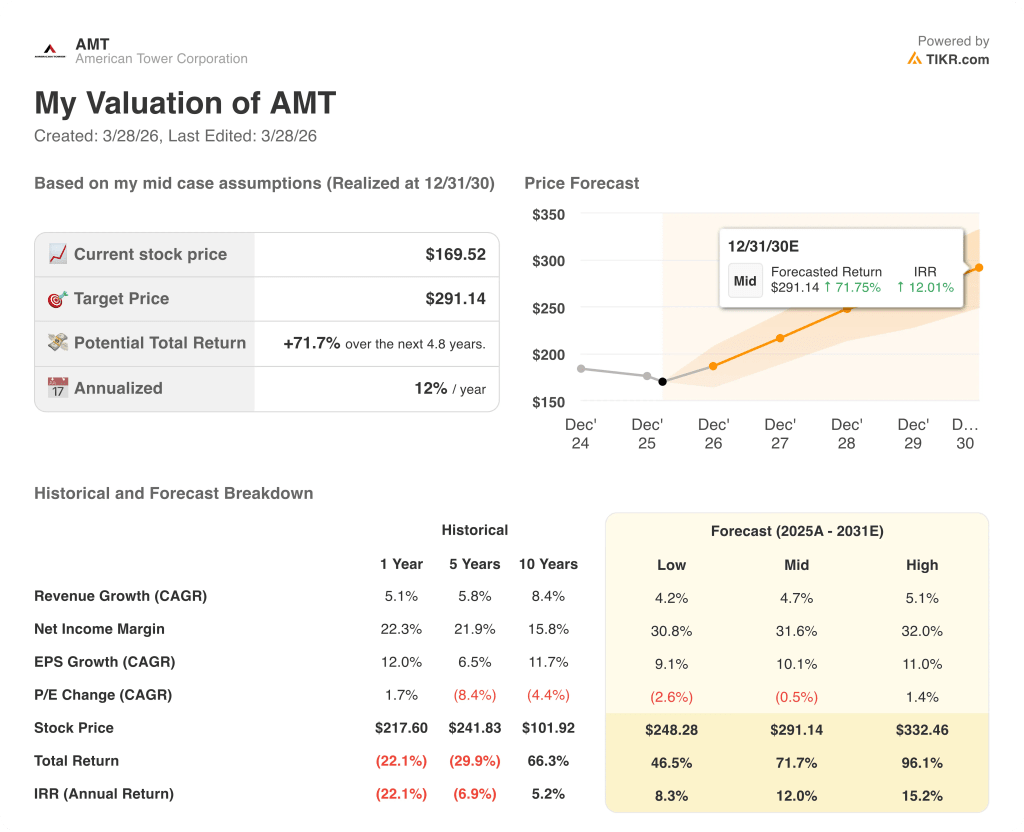

TIKR’s mid-case model targets $291.14 by December 31, 2030, implying a 12% annualized return, underpinned by a 4.7% revenue CAGR and net income margin expansion from 23.8% in 2025 to 31.6% by 2030, justified by AMT’s confirmed 200 to 300 basis point tower cash EBITDA margin expansion initiative and CoreSite’s fourth consecutive record sales year.

The market is pricing AMT at 0.73x NAV per share, its deepest discount in at least five periods tracked, even as free cash flow is estimated to reach $3.98 billion in 2026 and $4.53 billion in 2027.

CoreSite’s AI inferencing demand already exceeds available supply capacity, as management confirmed on the February 24 earnings call, directly supporting TIKR’s $291.14 mid-case target through sustained double-digit data center revenue growth.

Management’s $53 million in share repurchases already executed year-to-date in 2026, against $1.6 billion in remaining board authorization, signals the company itself views the current price as a structural mispricing, not a cyclical dip.

Latin America organic tenant billings growth turning sharply negative at approximately -3% in 2026, driven by accelerated consolidation churn in Brazil, breaks the model if that churn extends beyond 2026 and delays the projected 2027 re-acceleration.

AMT’s Q2 2026 earnings report is the first confirmation point to watch: U.S. ex-DISH colocation and amendment growth holding at approximately 2.5% and CoreSite revenue tracking toward 13% full-year growth are the two numbers that validate the TIKR mid-case.

Should You Invest in American Tower Corporation?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up AMT stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track American Tower Corporation alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze AMT stock on TIKR for Free →