Key Stats for FIS Stock

- Past week’s performance: -5.8%

- 52-week range: $46 to $83

- Valuation model target price: $66

- Implied upside: 41.0% over 2.8 years

Value your favorite stocks like FIS with 5 years of analysts’ forecasts using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Fidelity National Information Services (FIS) stock fell 5.8% over the past week, and the move came as investors kept reassessing the company’s 2026 setup. The latest pressure point was management turnover, because Reuters reported that Chief Product Technology Officer Firdaus Bhathena resigned effective March 20. That kind of change can matter for a fintech company because product leadership shapes software execution and client roadmaps.

The stock is also still digesting a major balance-sheet move from earlier this month. FIS completed senior notes offerings totaling $6.8 billion in U.S. dollars and €1 billion on March 11, after first announcing the planned offerings in late February.

The bigger narrative started with fourth-quarter results on February 24. Reuters reported that FIS posted adjusted EPS of $1.68, just below estimates of $1.69, while revenue rose 8% to $2.75 billion and beat expectations.

On the same day, FIS also completed its acquisition of Global Payments’ Issuer Solutions business and the sale of its Worldpay stake, which reshaped the company and made quarter-to-quarter comparisons more complicated.

So this week’s decline looks less like a reaction to one headline and more like continued skepticism around the reset story. Investors now have to balance stronger banking and issuer revenue against added financing activity, integration work, and leadership changes. That helps explain why the stock kept sliding even without a fresh earnings miss this week.

See analysts’ growth forecasts and price targets for FIS (It’s free) >>>

Is FIS Stock Undervalued?

Under valuation model assumptions realized through 12/31/28, the stock is modeled using:

- Revenue growth (CAGR): 12.1%

- Operating Margins: 24%

- Exit P/E Multiple: 7.5x

Based on these inputs, the model estimates a target price of $66.11, implying 41.0% total upside from the current share price and a 13.2% annualized return over the next 2.8 years.

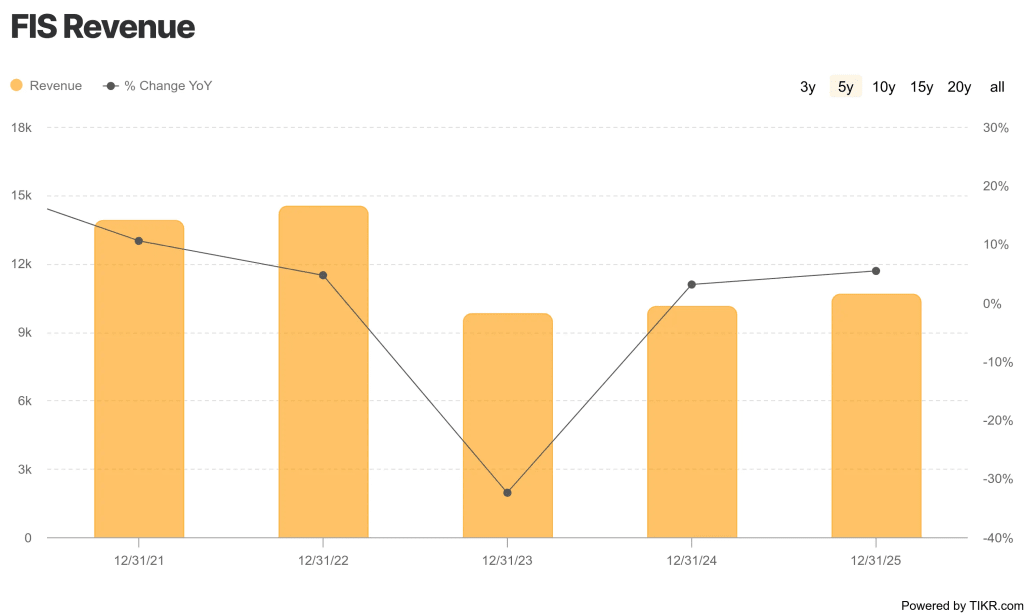

Those assumptions imply a meaningful recovery, but not an aggressive multiple. FIS generated $10.7 billion of revenue in 2025, and LTM EBIT margin was 22.0%, so the margin target mostly assumes the company sustains and modestly expands its current profitability. The more demanding assumption is revenue growth, because 12.1% is well above the 5.4% revenue growth FIS posted in 2025.

The valuation case depends heavily on the new portfolio mix. FIS said its 2026 outlook includes 357 days of contribution from the Issuer Solutions acquisition and only eight days of Worldpay equity-method contribution.

Cash flow still matters here because the market wants proof that the new structure can deleverage. FIS reported 2025 operating cash flow of $2.6 billion and said free cash flow increased 19% over the prior year, while the company returned $2.1 billion to shareholders in 2025, including $1.3 billion of buybacks. But net debt was still about $12.7 billion on an LTM basis, so the balance sheet remains part of the valuation debate.

The multiple in the model is also conservative. A 7.5x exit P/E is far below FIS’s longer-run valuation history and below today’s Street target framework, which helps explain why the model still gets to a double-digit annualized return. Even so, the stock will likely need cleaner execution and better visibility before investors reward it with a higher multiple.

What’s Driving the Stock Going Forward?

The next major catalyst is first-quarter 2026 earnings on May 6. FIS told investors to expect first-quarter revenue of $3.27 billion to $3.29 billion, adjusted EBITDA of $1.275 billion to $1.290 billion, and adjusted EPS of $1.26 to $1.30. Those numbers matter because they will be one of the first cleaner reads on the post-deal company.

Management is already framing 2026 as a growth year. CEO Stephanie Ferris said, “We are entering 2026 with continued strong momentum,” and the company guided for full-year adjusted revenue growth of 30% to 31% and adjusted EPS growth of 8% to 10%. But FIS also said pro forma revenue growth should be 5.1% to 5.7%, which shows how much of the headline growth rate comes from the acquisition rather than pure organic acceleration.

Client wins will be another key watch item. In March, FIS said Mizuho Financial Group selected its Balance Sheet Manager for Japan regulatory reporting, and Integrity Viking Funds chose FIS Investment Accounting Manager. Those wins matter because they support the Banking Solutions and capital-markets software franchise that is supposed to anchor steadier recurring revenue.

The market will also watch execution around debt, integration, and product continuity. The senior notes deal extended funding, but it also kept leverage in focus, while the Bhathena resignation added another leadership variable. So the stock’s next move will likely depend on whether FIS can turn its transaction-heavy reset into simpler growth and cleaner earnings delivery over the next few quarters.

Estimate a company’s fair value instantly (Free with TIKR) >>>

Should You Invest in Fidelity National Information?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up FIS, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track FIS alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Fidelity National Information stock on TIKR Free→

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!