Key Stats for Amazon Stock

- Past week’s performance: -5.1%

- 52-week range: $161 to $259

- Valuation model target price: $245

- Implied upside: 23.1% over 2.8 years

Value your favorite stocks like Amazon with 5 years of analysts’ forecasts using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Amazon (AMZN) stock fell 5.1% this week as investors pulled back from large-cap growth names. Reuters reported that the Dow entered correction territory on March 27, while the Nasdaq hit a seven-month low. Amazon was specifically named among the megacap stocks dragging the market lower as war-driven oil prices and inflation fears hurt risk appetite.

Company-specific headlines also added to the cautious tone. Reuters reported that Amazon’s AI chip product leader, Gadi Hutt, left the company. That does not change Amazon’s broader AI strategy by itself, but it matters because investors are closely watching execution in AWS custom silicon and AI infrastructure.

The market is also still digesting Amazon’s capital intensity. Reuters reported earlier this month that Amazon targeted about $37 billion in a bond sale to help fund AI infrastructure, and Andy Jassy said the company expects about $200 billion of capital expenditures in 2026. For a stock already trading on long-term AI expectations, large spending plans can pressure sentiment when investors start focusing on near-term returns and margin risk.

At the same time, Amazon kept generating growth headlines across several businesses. Zoox will expand in San Francisco and Las Vegas and begin testing robotaxis in Austin and Miami, while Amazon also launched a healthcare AI assistant on its website and app earlier in March. So this week’s decline looked more like a valuation reset in a weak tape than a sign that Amazon’s business momentum had broken.

See analysts’ growth forecasts and price targets for Amazon (It’s free) >>>

Is Amazon Stock Undervalued?

Under valuation model assumptions realized through 12/31/28, the stock is modeled using:

- Revenue growth (CAGR): 12.3%

- Operating Margins: 11.2%

- Exit P/E Multiple: 25.7x

Based on these inputs, the model estimates a target price of $245, implying 23.1% total upside from the current share price and a 7.8% annualized return over the next 2.8 years.

That return profile looks respectable, but not especially cheap. A 7.8% annualized return is below the 10% level many long-term investors usually target. The model also assumes only a modest valuation from here, so most of the case depends on Amazon continuing to grow revenue and protect margins.

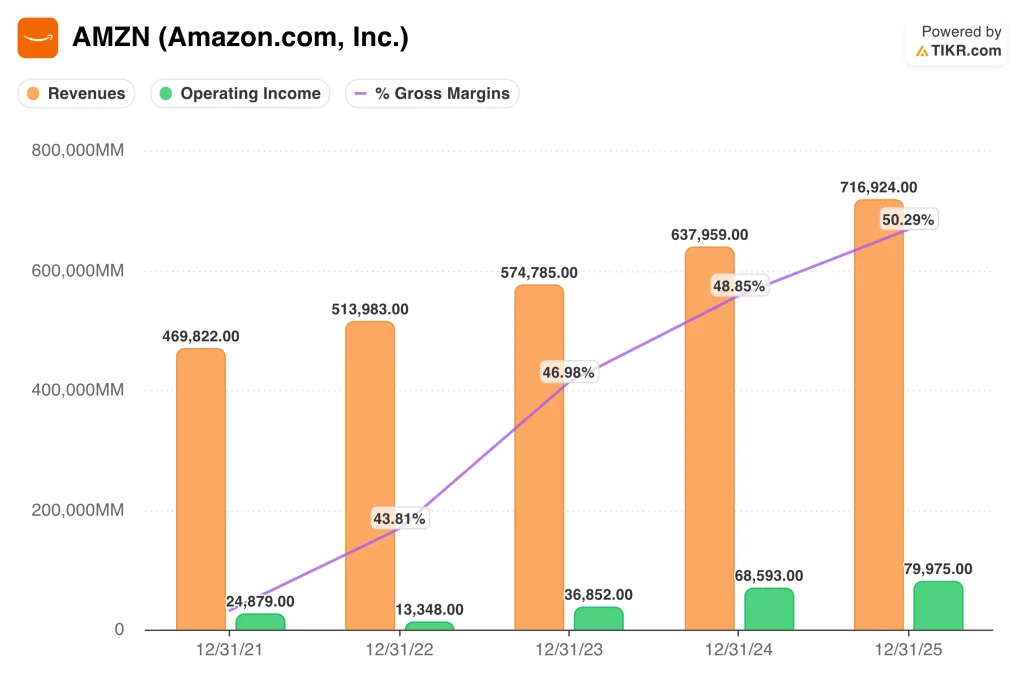

The business itself remains very strong. Amazon reported 2025 net sales of $716.9 billion, up 12%, while operating income rose to $80.0 billion and AWS revenue increased 20% to $128.7 billion. Net income reached $77.7 billion, and operating cash flow rose 20% to $139.5 billion.

Margins have improved meaningfully, and that is a big part of the valuation story. Gross margin reached 50.3%, and operating margin rose to 11.2% in the latest period, which is a major step up from 5.3% in 2021 and 2.6% in 2022. But free cash flow fell to about $11.2 billion in Amazon’s reported measure because property and equipment spending jumped by $50.7 billion year over year, mainly for AI.

That leaves Amazon in an in-between valuation zone. The stock trades at about 25.7x NTM P/E and 10.4x NTM EV/EBITDA in your overview, which is not extreme for a company with double-digit revenue growth and rising profitability. Still, the market is clearly asking whether AI-related spending will keep translating into enough AWS, advertising, and retail profit growth to justify that multiple.

What’s Driving the Amazon Stock Going Forward?

The next major catalyst is first-quarter results, expected on April 29. Investors will be looking for revenue growth, AWS growth, and any change in operating income guidance. They will also want to hear whether AI demand is strong enough to support the company’s unusually high capital spending plans.

Management commentary will matter a lot. In February, Andy Jassy said, “AWS is growing 24%, Advertising is growing 22%, Stores are growing briskly across North America and internationally, our chips business is growing triple-digit percentages year-over-year.” He also said Amazon expects about $200 billion in 2026 capital expenditures because of strong demand in AI, chips, robotics, and low-earth-orbit satellites.

AWS remains the core driver of the long-term thesis. Reuters reported that Amazon is accelerating internal AI use in AWS sales and other groups after staff cuts, and also noted that AWS continues to broaden its infrastructure partnerships, including recent work with Nvidia. If AWS keeps compounding while Amazon’s custom chips gain traction, that can support both revenue growth and margin expansion.

The risk side is straightforward. Reuters reported new scrutiny around online reviews in the UK, AI spending across Big Tech is drawing more debate, and the broader market has turned less patient with megacap names during this oil-driven selloff.

So Amazon’s next move will likely depend on whether earnings and AWS demand are strong enough to offset spending concerns and a tougher macro backdrop.

Estimate a company’s fair value instantly (Free with TIKR) >>>

Should You Invest in Amazon.com, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up AMZN, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track AMZN alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Amazon stock on TIKR Free→

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!