Key Stats for UBER Stock

- Past-Week Performance: -6%

- 52-Week Range: $61 to $102

- Valuation Model Target Price: $122

- Implied Upside: 77%

Analyze your favorite stocks like Uber Technologies with TIKR (It’s free) >>>

What Happened?

Uber Technologies, Inc. stock is down about 6% this week, trading near $69 per share, as investors react to cautious positioning ahead of its upcoming earnings report, moderating growth expectations, and limited new analyst catalysts to support near-term momentum, with the stock also facing pressure alongside competitors like Lyft and DoorDash.

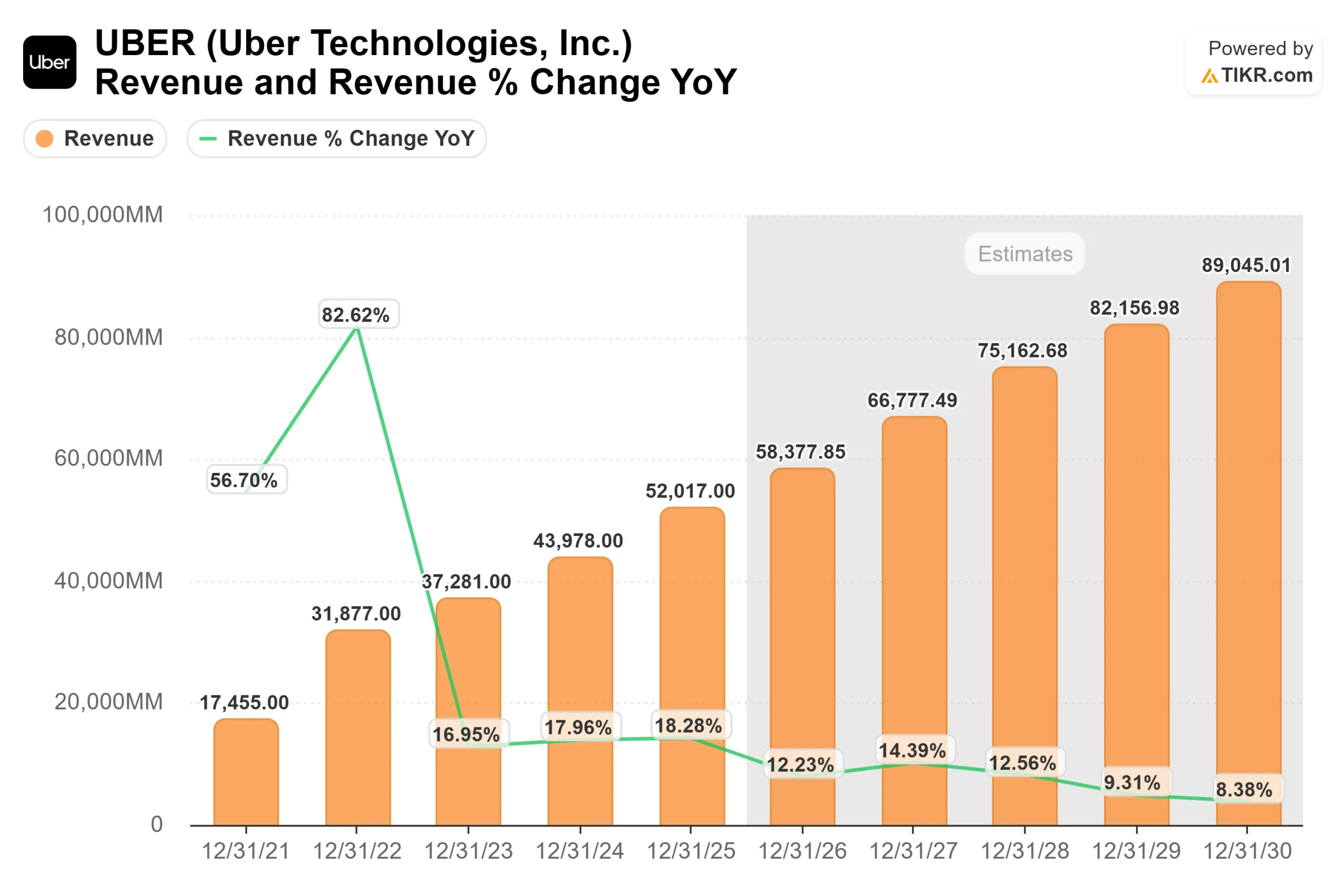

The stock is down primarily because investors are resetting expectations around Uber’s growth and profitability outlook, with revenue growth now expected to normalize into the low-teens range while attention shifts toward whether margin expansion can continue at the pace needed to justify higher valuations.

That shift in focus toward profitability over growth, combined with the absence of new bullish analyst upgrades this week and continued competition from ride-hailing peer Lyft and delivery leader DoorDash, has weighed on sentiment.

At a recent Morgan Stanley conference, Uber reinforced its strong financial position, with CFO Balaji Krishnamurthy highlighting that the company generated about $10 billion in free cash flow and returned over $6 billion to shareholders, while cross-platform users are driving 3x higher gross bookings and profits with penetration still at 20%, showing significant room for expansion.

The company also pointed to improving efficiency in autonomous deployments, including 30% higher utilization and 25% faster ETAs in select markets, supporting the long-term margin story, with Krishnamurthy noting, “we think our stock is dislocated right now, and we are being aggressive.”

Recent analyst and institutional activity reinforced the mixed outlook. While the Street target price remains around $104, there have been no major upward revisions recently to re-accelerate sentiment. Institutional positioning also showed balanced flows, with HWG Holdings LP cutting its stake by 77.6% and Nordea Investment Management AB trimming its holdings by 4.6%, alongside reductions from Assenagon Asset Management and Wealth Enhancement Advisory Services LLC.

At the same time, buying activity came from Overbrook Management Corp, which increased its stake by 37.4%, and Sarasin & Partners, which raised its position by 38.4%, while Czech National Bank also added modestly.

Institutional ownership remains high at about 80%, suggesting continued interest, but the balanced flows reflect a market still waiting for clearer catalysts.

Value Uber Technologies instantly (Free with TIKR) >>>

Is UBER Undervalued?

Under valuation assumptions, the stock is modeled using:

- Revenue Growth (CAGR): 13.1%

- Operating Margins: 16.3%

- Exit P/E Multiple: 20.9x

Uber’s revenue growth is stabilizing into a more durable low-teens range, reflecting its transition from a high-growth disruptor into a scaled platform business across mobility (ride-hailing) and delivery (Uber Eats), both of which generate increasing monetization opportunities.

See analysts’ growth forecasts and price targets for Uber Technologies (It’s free) >>>

Profitability is now the key driver, with margins expected to expand as the company benefits from reduced driver incentives, improved pricing algorithms, and higher utilization across its network, allowing more revenue to convert into earnings as the business matures.

A key advantage relative to competitors like Lyft and DoorDash is Uber’s multi-product ecosystem, where cross-platform users generate significantly higher engagement and spend, creating a structural edge in customer lifetime value compared to Lyft’s single-product focus and DoorDash’s delivery-heavy model.

Additional upside comes from newer monetization levers, including Uber One (its subscription program that improves user retention and frequency) and in-app advertising, which add high-margin revenue streams without requiring proportional increases in costs.

Based on these inputs, the model estimates a target price of $122, implying about 77% total upside, suggesting the stock appears undervalued, with future performance driven by margin expansion, ecosystem monetization, and sustained free cash flow growth.

How Much Upside Does UBER Stock Have From Here?

Investors can estimate Uber Technologies’ potential share price, or what any stock could be worth, in under a minute using TIKR’s New Valuation Model tool.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

Value Uber Technologies in under 60 seconds with TIKR (It’s free) >>>