Key Stats for Arcosa Stock

- Past-Week Performance: +2.2%

- 52-Week Range: $68.1 to $131

- Current Price: $102.9

What Happened?

Arcosa (ACA) traded at $102.85 after the infrastructure products manufacturer announced a $450 million cash sale of its barge business on February 24, reshaping its portfolio entirely around construction materials and engineered structures with record adjusted EBITDA of $583 million in FY 2025.

On February 26, Arcosa reported Q4 adjusted EPS of $1.15 against an IBES estimate of $0.92, a 25-cent beat, while Q4 adjusted EBITDA of $145 million topped the $141.2 million consensus as the Engineered Structures segment, which manufactures utility poles and wind towers for power grid infrastructure, posted 22% EBITDA growth.

Utility structures, the segment’s higher-margin business supplying steel poles that connect power generation to the grid, drove 20% revenue growth in Q4 with double-digit volume gains and high single-digit pricing, while FY 2025 adjusted EBITDA margin expanded 280 basis points to a record 20.2%.

Antonio Carrillo, President and CEO, stated on the Q4 2025 earnings call that “the barge transaction further reduces portfolio complexity and cyclicality, raises our overall margin profile and enhances the long-term resiliency of the company,” directly preceding the company’s announcement that it would convert its Tulsa, Oklahoma wind tower facility to utility pole production alongside an already-underway Illinois plant conversion.

Arcosa enters 2026 with $915 million in liquidity, a FY 2026 adjusted EBITDA guidance midpoint of $615 million, utility structures backlog at $435 million, and an active M&A pipeline targeting bolt-on aggregates acquisitions, positioning the now-simpler two-segment company to compound margin gains through infrastructure spending tailwinds the company’s own third-party study projects accelerating through at least 2030.

Wall Street’s Take on ACA Stock

The $450 million barge divestiture announced February 24 removes Arcosa’s most cyclical revenue stream and directly unlocks a cleaner margin profile, with TIKR estimating FY 2026 adjusted EBITDA expanding to $610 million at a 20.5% margin from a record 20.2% in FY 2025.

Normalized EPS grew 48% to $4.47 in FY 2025 and TIKR estimates a further climb to $4.91 in FY 2026 and $5.37 in FY 2027, supported by utility structures pricing up high single digits, volume up double digits, and the removal of the barge segment’s lower-margin revenue from the consolidated earnings base.

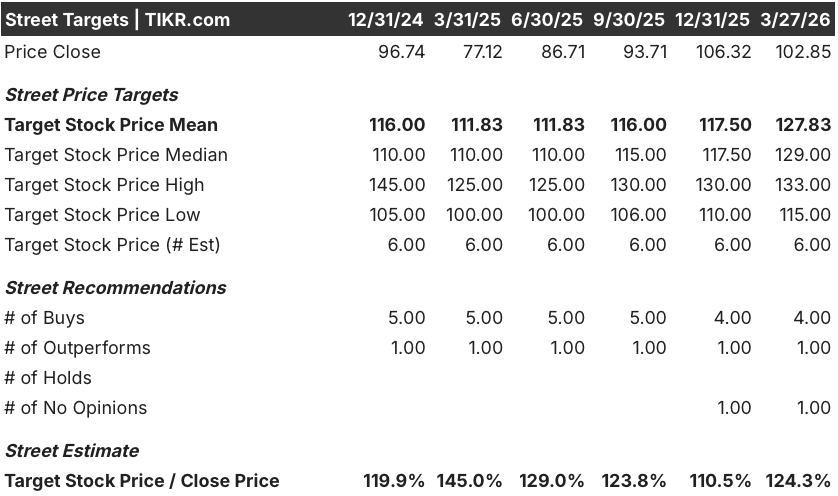

Still, five analysts carry buy or outperform ratings on ACA with zero holds and zero sells, a mean price target of $127.83 against the current $102.85, implying 24.3% upside as the Street prices in the structural shift toward power grid infrastructure.

The target range runs from $115 on the low end to $133 on the high end: the low anchors to near-term wind tower revenue declining roughly 25% in 2026, while the high requires utility structures to fully absorb that shortfall and sustain double-digit EBITDA growth as Arcosa’s Illinois plant conversion comes online in H2 2026.

What Does the Valuation Model Say?

The TIKR mid-case model prices ACA at $137.23 by December 2031, assuming a 6.5% revenue CAGR and net income margins expanding to 8.3%, directly supported by the utility structures backlog sitting at $435 million and growing demand for large steel poles connecting new power generation to the grid.

The market prices ACA at $102.85 while the company just posted record EBITDA margins and guided for further expansion, a disconnect the $450 million barge sale makes increasingly difficult to justify.

Utility structures backlog grew 5% in 2025 and customer reservations not yet in backlog remain strong, the operational evidence directly underpinning TIKR’s 6.5% revenue CAGR and $137.23 target.

Moreover, management’s decision to convert the Tulsa wind tower facility to utility pole production confirms this is a deliberate structural repositioning, not a cyclical margin bump.

A 25% wind tower revenue decline in 2026 breaks the flat-segment-margin assumption for Engineered Structures if utility structures volume or pricing disappoints, compressing blended EBITDA margin below the 20.5% TIKR estimate.

The Q2 2026 barge divestiture close is the near-term event to watch: the $450 million in proceeds deployed into bolt-on aggregates acquisitions determines whether FCF, estimated by TIKR at $230 million for FY 2026, translates into earnings-accretive growth or simply debt reduction.

Should You Invest in Arcosa, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up ACA stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Arcosa, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze ACA stock on TIKR for Free →