Key Stats for Motorola Stock

- Past-Week Performance: -3.1%

- 52-Week Range: $359.4 to $492.2

- Current Price: $438.3

What Happened?

Motorola Solutions (MSI), a public safety technology company whose integrated platform of radios, cameras, and command software serves governments and agencies worldwide, closed Q4 with a record $15.7 billion backlog and a stock trading at $438.32, after the company delivered its first-ever 30%-plus annual operating margin and raised its 2026 revenue outlook to $12.7 billion.

Last month, the company reported Q4 non-GAAP EPS of $4.59, beating the IBES estimate of $4.35 by 5.5%, while Q4 revenue of $3.38 billion topped consensus, driven by 12% top-line growth and a record non-GAAP operating margin of 32.1%, up 170 basis points year over year.

Underpinning the beat, the Software and Services segment, which houses recurring-revenue businesses including command center software, video analytics, and cybersecurity, grew 13% for the full year to $4.4 billion and expanded operating margins to 32.5%, while product orders surged 26% in Q4 to a record $2.4 billion, the third consecutive quarter of double-digit order growth.

On the acquisitions front, Motorola closed the purchase of Exacom on March 12, adding cloud-native 911 voice recording and logging capabilities that integrate directly into its existing Assist Suites and Digital Evidence Management platform, deepening the company’s end-to-end command center ecosystem just weeks after it signed a CAD $675 million deal on March 27 to acquire Bell Canada’s land mobile radio network services business.

Chairman and CEO Gregory Brown stated on the Q4 2025 earnings call that “our record ending backlog position, strong demand environment, and expanding product and services portfolio are all informing our expectations for another strong year of revenue earnings and cash flow growth,” anchoring guidance for $12.7 billion in 2026 revenue and non-GAAP EPS of $16.70 to $16.85, both above Wall Street consensus.

Motorola’s competitive position over the next three to five years rests on three compounding drivers: Silvus, its mobile ad hoc networking unit serving drone and defense customers, is now targeting $675 million in 2026 revenue against a $3 billion TAM management expects to roughly double, the Assist Suites at $99 per user per month expand the Command Center TAM by roughly $2 billion while targeting growth from an APX NEXT subscriber base of 300,000 by year-end, and approximately $3 billion in projected 2026 operating cash flow gives the company sustained firepower for M&A and buybacks within its 60-30-10 capital allocation framework.

Wall Street’s Take on MSI Stock

The record $15.7 billion backlog and the February 11 earnings beat confirm that MSI’s integrated public safety platform, combining mission-critical radio networks, video security, and command center software, is compounding earnings reliably, with as TIKR estimates, normalized EPS reaching $16.78 in 2026 on the back of sustained revenue growth and expanding EBITDA margins.

FY2025 normalized EPS of $15.38 marked the fifth consecutive year of double-digit growth, and as TIKR estimates, EBITDA margins expand from 31.9% to 33.9% in 2026, a trajectory supported by the Software and Services segment growing 13% last year and commanding 32.5% operating margins.

Twelve analysts covering MSI carry 7 buys and 5 outperforms against just 2 holds and zero sells, with a mean price target of $502.00 implying 14.5% upside from the current $438.32, a consensus anchored to sustained Command Center growth of 15% and continued APX NEXT subscriber expansion toward 300,000 users by year-end.

The spread between the street’s low target of $470.00 and high of $525.00 is relatively tight, suggesting the debate is not about whether MSI grows but about how much the Silvus defense unit, targeted at $675 million in 2026 revenue inside a $3 billion TAM, accelerates the upside case.

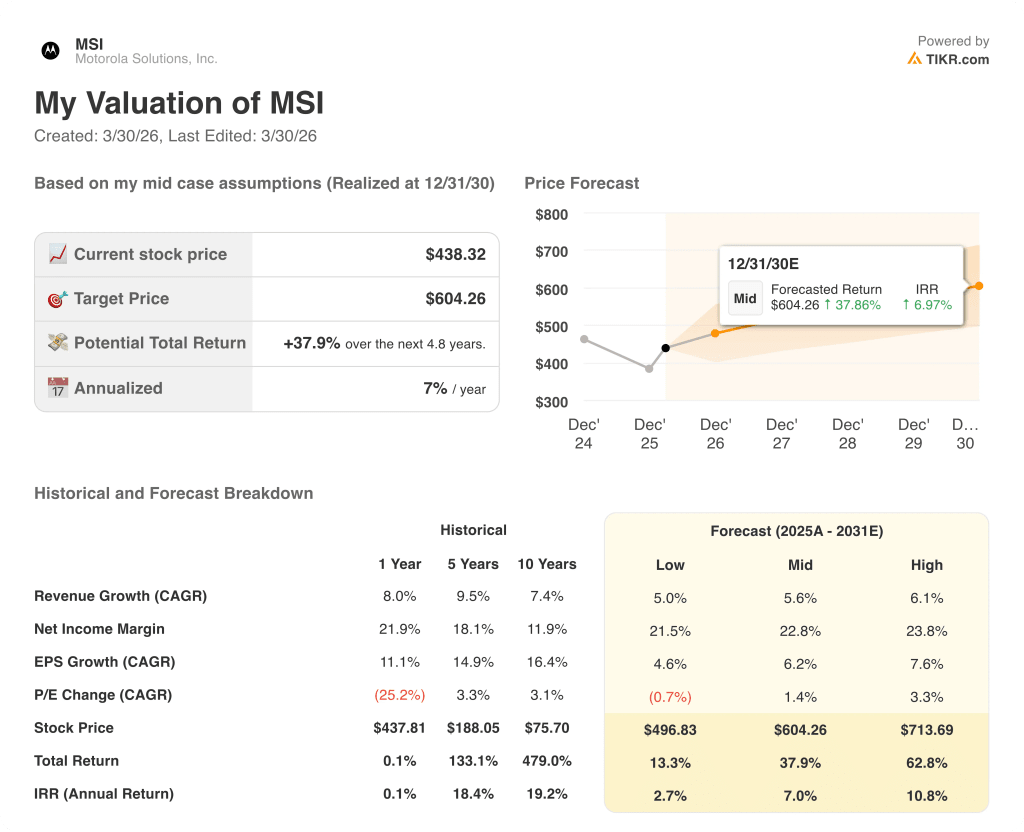

What Does the Valuation Model Say?

The TIKR mid-case model prices MSI at $604.26 by December 2030, implying a 7.0% annualized return from current levels, built on a 5.6% revenue CAGR and a net income margin of 22.8%, assumptions grounded in the company’s first-ever 30%-plus annual operating margin and $2.79 billion in projected 2026 free cash flow.

The market is pricing MSI as a mid-single-digit grower, but five consecutive years of double-digit normalized EPS growth and a record 32.1% Q4 operating margin challenge that framing directly.

The $15.7 billion backlog, of which nearly $12 billion sits in high-margin Software and Services, provides multi-year revenue visibility that directly underpins the TIKR model’s $604.26 target.

Management’s double-digit product order guidance for every quarter of 2026 signals that demand is structural, not cyclical, the single most important confirmation that the EPS compounding thesis is intact.

If Silvus revenue, targeted at $675 million in 2026, disappoints materially due to a Ukraine ceasefire or defense budget cuts, the TIKR model’s 5.6% revenue CAGR assumption faces its most direct stress test.

Q1 2026 earnings, where management guided revenue growth of 6% to 7% and non-GAAP EPS of $3.20 to $3.25, will confirm whether the Software and Services margin expansion and double-digit order momentum are holding on schedule.

Should You Invest in Motorola Solutions, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up MSI stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Motorola Solutions, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze MSI stock on TIKR for Free →