Key Stats for Snap Stock

- Current Price: $3.93

- Target Price (Base Case): $3.06

- Street Target: $7.97

- Potential Total Return: (22.1%)

- Annualized IRR: (8.60%) / year

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

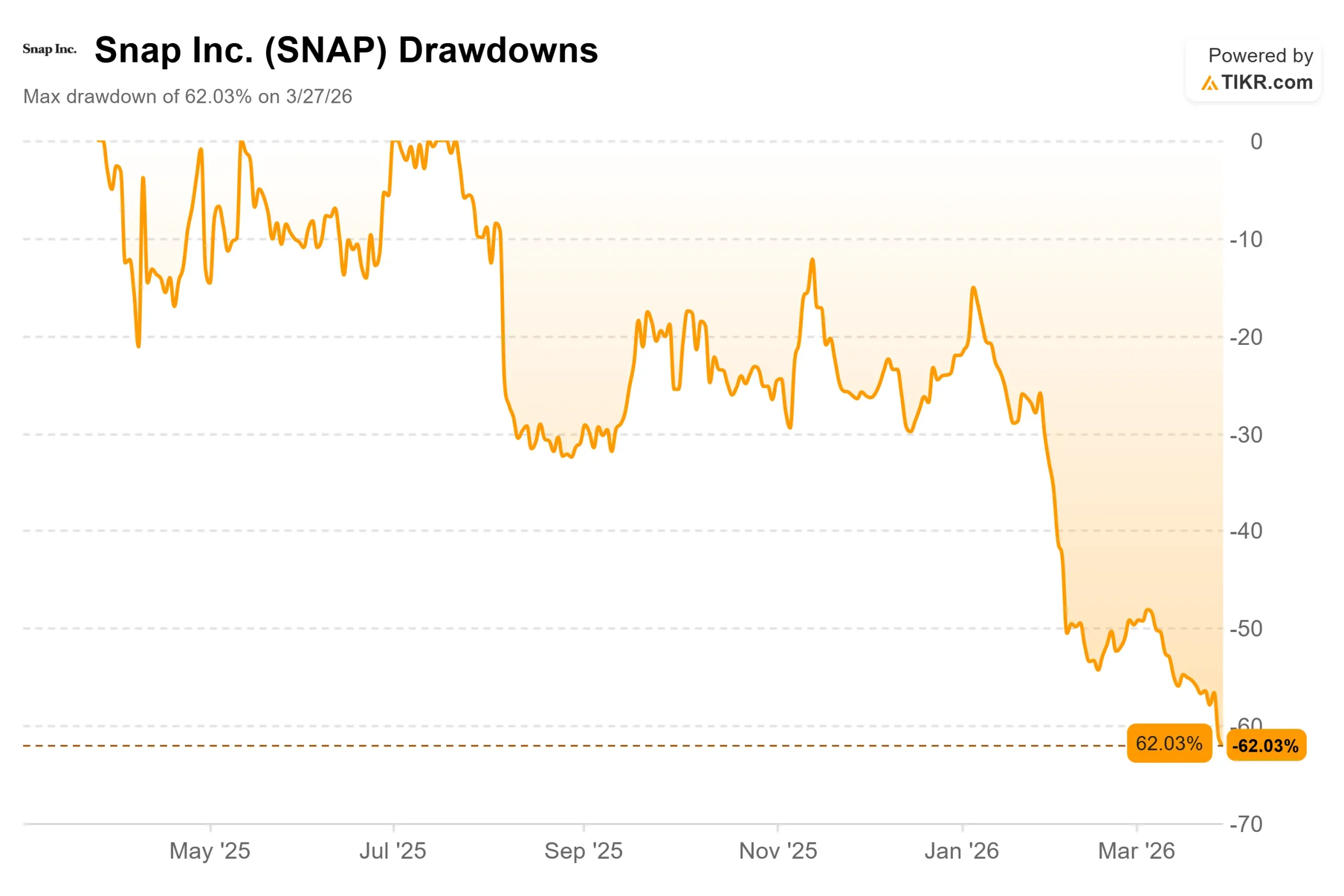

Snap (SNAP) stock has shed more than 51% year to date and closed at an all-time low on March 26, 2026, after a week that concentrated every risk investors had been tracking.

Bulls point to a growing subscription business and a genuine path to profitability. Bears argue that Snap’s advertising model is structurally fragile, and the regulatory pressure forming around Snapchat is not a temporary overhang.

The single question the market is asking right now is whether $3.93 reflects a rational reset or a massive overshoot.

The European Commission opened a formal investigation into Snap on March 26 under the Digital Services Act, sending the stock down 10.69% on the day. The DSA (the EU’s framework requiring large platforms to protect users from harmful content) allows fines of up to 6% of global annual revenue for non-compliance.

At Snap’s 2025 revenue base of $5.93 billion, that represents a calculated fine ceiling of approximately $356 million, significant for a company that has not yet reached sustained GAAP profitability.

The inquiry will examine Snapchat’s age verification system, its handling of grooming and criminal recruitment of minors, and its removal of content promoting illegal goods.

The EU investigation did not arrive in a vacuum.

On February 4, Snap reported Q4 2025 revenue of $1.72 billion, beating the $1.70 billion consensus, and authorized a $500 million share repurchase program.

But global daily active users of 474 million missed the 478 million Wall Street expected, North American DAUs of 94 million fell short of the 97 million projected, and Q1 2026 revenue guidance of $1.50 to $1.53 billion landed below the $1.55 billion estimate. The stock fell 13.37% that day and has not recovered.

CEO Evan Spiegel, Co-Founder and Chief Executive Officer of Snap Inc., addressed the regulatory environment directly on the earnings call. Spiegel said revenue from users under 18 is “not material” and that Snap is “not overly concerned about the changing regulatory environment” when assessing the company’s revenue-generating potential.

The EU opened its formal probe three weeks later.

See historical and forward estimates for Snap stock (It’s free!) >>>

Is Snap Undervalued Today?

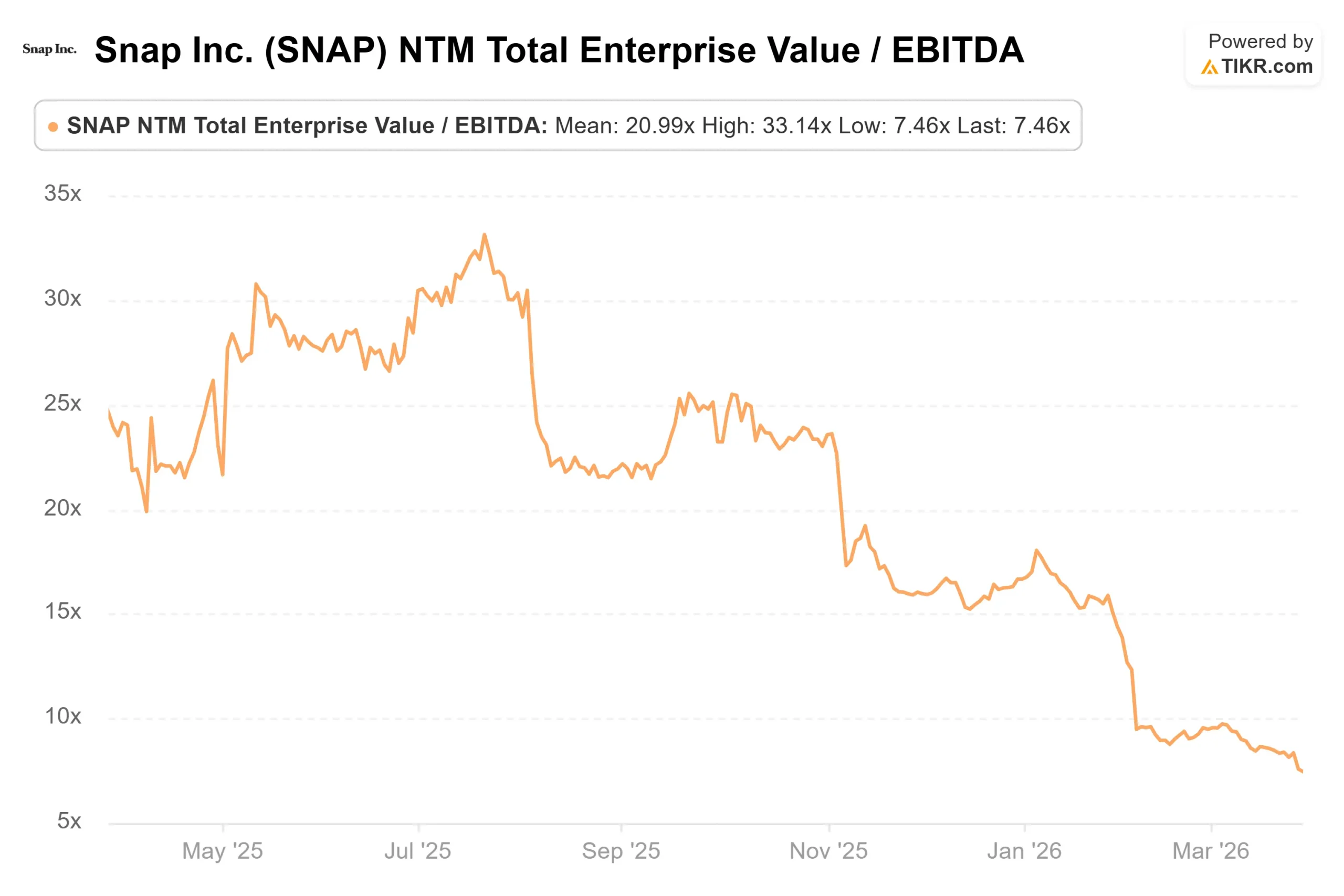

At $3.93, Snap trades at 1.17x NTM EV/Revenue and 7.46x NTM EV/EBITDA (NTM means next twelve months, the forward-looking consensus).

The Street’s mean price target of $7.97 implies roughly 103% upside from here, with 7 Buys, 3 Outperforms, 31 Holds, 2 Underperforms, and 1 Sell across 44 analysts. Those targets have been cut steadily all year without the stock ever closing the gap.

The subscription business is the most concrete positive in the Snap story. Snap announced in February that its direct revenue category, including Snapchat+, Lens+, Snapchat Platinum, and Memories Storage Plans, has exceeded a $1 billion annualized run rate, anchored by a global subscriber community of more than 25 million.

That revenue stream carries higher margins than advertising and grows independently of ad market cycles. On the ad side, active advertisers grew 28% year-over-year in Q4, driven by the small and medium-sized business segment.

The advertising picture is harder to be optimistic about.

Morgan Stanley cut its Snap price target from $9.50 to $6.50 in March, noting the core business is performing better than expected but flagging uncertainty around a reported $400 million high-margin revenue opportunity from Snap’s Perplexity AI partnership, a deal that, based on analyst commentary, has been pushed to later in 2026.

The competitor context is worth noting.

Among Snap’s peers in interactive media, Pinterest trades at 1.92x NTM EV/Revenue and 6.60x NTM EV/EBITDA, while Baidu trades at 1.93x NTM EV/Revenue and 10.65x NTM EV/EBITDA. Snap’s 1.17x NTM EV/Revenue looks like a discount on the surface.

Both Pinterest and Baidu are operationally profitable on a GAAP basis and carry lower regulatory risk today. The discount may be warranted, not cheap.

A California jury recently found Meta and YouTube liable for designing their platforms to exploit young users. Snap had been included in the same litigation but settled before the verdict for an undisclosed amount.

The broader legal environment around platforms with young user bases is tightening, and Snapchat’s audience skews younger than almost any of its major competitors.

See how Snap performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $3.93

- Target Price (Base Case): $3.06

- Potential Total Return: (22.1%)

- Annualized IRR: (8.60%) / year

See analysts’ growth forecasts and price targets for Snap stock (It’s free!) >>>

The TIKR base-case model targets $3.06 by December 31, 2028, implying a negative 22.1% total return. The model assumes a 10.2% revenue CAGR, driven by continued subscription growth and a gradual recovery in advertiser demand as the SMB segment scales. The margin driver is gross margin expansion toward 60%, consistent with CFO Derek Andersen’s Q4 commentary. Even so, the model projects a negative 2.4% operating margin through 2028, reflecting continued investment in Specs (Snap’s AR glasses, scheduled for consumer launch in 2026), AI infrastructure, and sales force expansion.

The upside case: the Perplexity partnership revenue arrives on schedule, Specs finds a consumer audience, and the EU investigation resolves without material fines. The downside case: DSA penalties approach the 6% ceiling, the Perplexity deal disappoints, and under-18 regulations tighten further across Europe. The TIKR model says the stock is not cheap at $3.93. That is the honest read.

Conclusion: Watch the advertising revenue line at Snap’s Q1 2026 earnings on May 6, 2026. Advertising revenue grew just 5% year-over-year in Q4. If that rate decelerates while subscriptions offset it, the margin story holds, but the core ad platform thesis weakens further. If advertising reaccelerates and Perplexity revenue is confirmed for Q3, the narrative changes quickly. That single line will determine whether this stock stabilizes or makes new lows.

Snap has 946 million monthly active users, a subscription business crossing a $1 billion annualized run rate, and a hardware bet on the horizon, trading at a price not seen since before its 2017 IPO. The TIKR model says it is still not cheap enough to own.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Snap?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Snap, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Snap alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!