Key Stats for Navitas Semiconductor Stock

- 52-Week Range: $5.44 to $34.17

- Current Price: $12.78

- Street Mean Target: ~$14.46

- Market Cap: ~$3 billion

- Q1 2026 Revenue: $8.6 million (up 18% sequentially)

- Q1 2026 Net Loss: ($33.8 million)

- Cash and Equivalents: $221 million as of March 31, 2026

- Q2 2026 Revenue Guidance: $10.0 million

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

From $32 to $13: What Happened After the NVIDIA Rally Faded

Navitas Semiconductor (NVTS) had one of the more dramatic runs of 2026. Coming into the year, the stock was trading quietly around $10, largely ignored while bigger semiconductor names grabbed the headlines.

Then, in April, a combination of NVIDIA GTC conference buzz, growing attention on AI power infrastructure, and anticipation around earnings sent the stock into a frenzy, briefly touching $32 before Q1 results arrived in May.

The earnings beat expectations on revenue, the company guided Q2 above consensus, and the stock still fell. By July, it had given back nearly everything, sitting at a drawdown of nearly 60% from that peak.

The drawdowns chart captures how punishing this ride has been for anyone who bought at the wrong moment.

The stock has essentially spent the past year oscillating between deep losses and brief recoveries, with each recovery aggressively sold. What the chart does not show is why the volatility exists in the first place, and that story is actually more interesting than the price action suggests.

Navitas makes gallium nitride, or GaN, and silicon carbide, or SiC, power semiconductors. These are chips that control how electricity flows through a system, and investors got excited because GaN and SiC are meaningfully more efficient than older silicon-based alternatives.

In an AI data center, where power density and efficiency are increasingly the binding constraints on how many GPUs you can pack into a rack, that efficiency advantage translates directly into competitive value.

CEO Chris Allexandre has been explicit about the pivot, describing a “Navitas 2.0” strategy that is deliberately shedding the company’s legacy mobile and consumer business to focus entirely on AI data centers, energy infrastructure, and industrial electrification. The AI infrastructure segment grew 50% quarter over quarter in Q1 alone.

See analysts’ growth forecasts and price targets for NVTS stock (It’s free!) >>>

The Path to Profitability Is Visible, but It Is Still Years Away

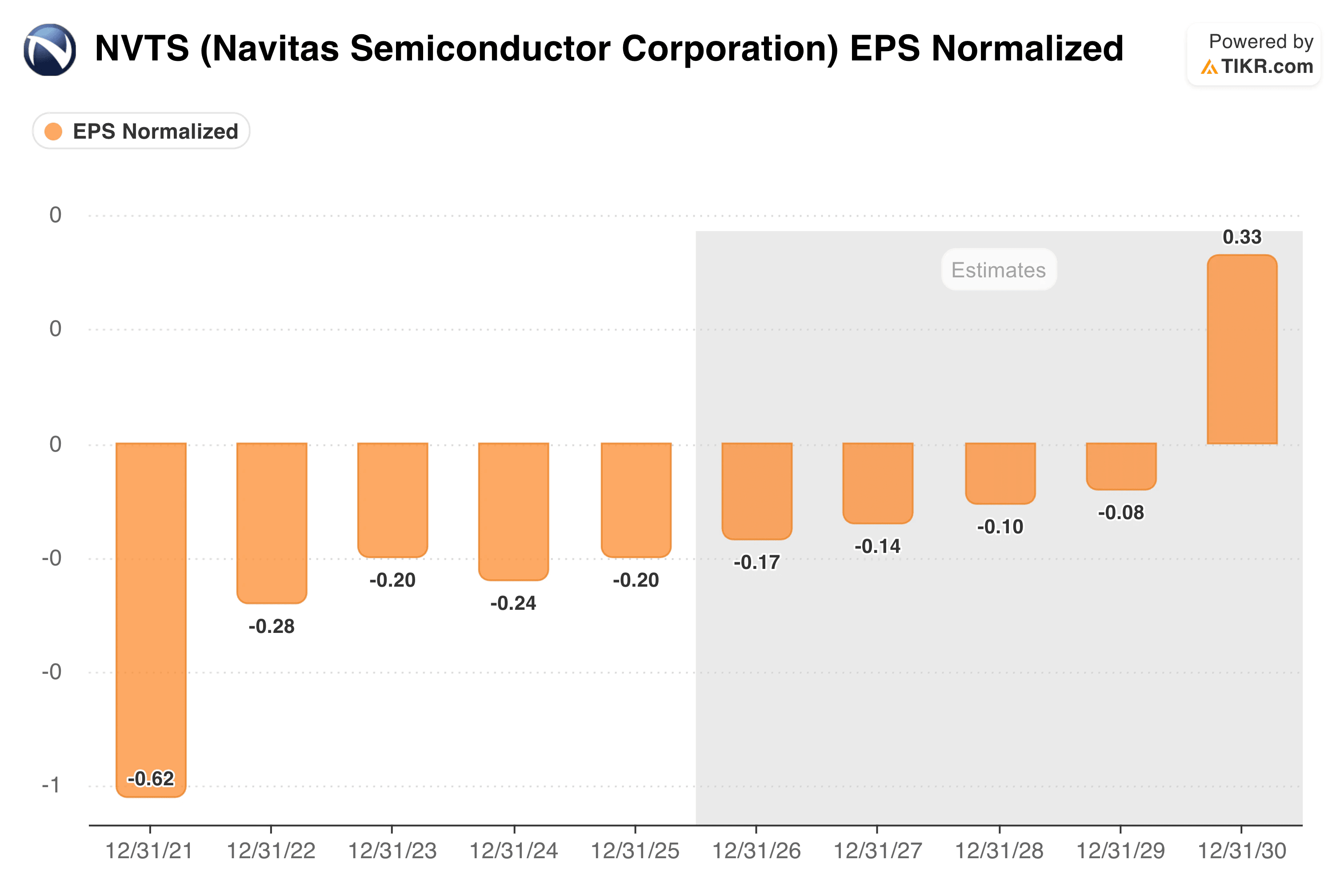

The EPS chart here is worth sitting with, because it tells the honest version of the Navitas story. The company has been losing money every year since going public, and those losses are not shrinking quickly.

Normalized EPS came in at around -$0.20 in 2025, and consensus estimates have it still negative through 2029, narrowing gradually from -$0.17 this year to around -$0.08 by 2029 before finally flipping positive in 2030.

The reason the losses persist even as the strategic pivot gains traction is straightforward. Navitas is a small company doing around $8 to $10 million in quarterly revenue while running operating expenses of roughly $15 million per quarter.

Management has said the business reaches profitability somewhere in the “high 30s” of millions in quarterly revenue, which, at the current growth rate, is still a few years out. The good news is that the balance sheet gives it time to get there. Cash stood at $221 million at the end of Q1 with no debt, which, at the current burn rate of around $16 million per quarter, provides a meaningful runway.

The gross margin picture is also quietly improving, with non-GAAP gross margin reaching 39% in Q1 and guided slightly higher for Q2, as the mix shifts away from low-margin mobile revenue toward higher-value power products.

The NVIDIA collaboration is worth noting specifically, as Navitas has been working with NVIDIA on an 800V direct-current power architecture for AI infrastructure, which is essentially a new approach to delivering power in data centers that significantly reduces energy waste.

If that architecture gains broad adoption among hyperscalers, Navitas’s addressable market grows substantially.

Estimate a company’s fair value instantly (Free with TIKR) >>>

What the TIKR Model Says, and What It Requires You to Believe

The TIKR valuation model for Navitas projects a mid-case target price of around $22 over the next 4.5 years, implying an annualized return of roughly 12% per year from current levels.

The longer-range mid-case, out to December 2034, reaches $81, but that figure assumes nearly 45% annual revenue growth sustained for a decade on a business currently doing around $35 million in annual revenue. Net income margins stay negative throughout the forecast period, even in the optimistic case.

Investors need to be clear-eyed about what those numbers require. The 12% annualized return over 4.5 years is a more grounded figure to anchor to, and even that assumes the high-power pivot succeeds, that GaN adoption in AI data centers accelerates as expected, and that Navitas captures meaningful share against larger, better-resourced semiconductor companies.

The bull-case IRR of around 31% through December 2034 is the kind of number that attracts speculative interest, but it rests on a very long chain of execution assumptions for a company that has not yet demonstrated consistent revenue growth.

The range between the low and high-case stock prices in 2030 is around $50 to nearly $130, which shows how wide the uncertainty band really is.

Should You Invest in Navitas Semiconductor?

Navitas is a genuinely interesting company with a real technology advantage in a market that matters, but it is also pre-profitability, highly volatile, and trading at a valuation that already prices in significant growth.

The GaN and SiC opportunity in AI infrastructure is real, and if the Navitas 2.0 pivot plays out as management describes, the stock has meaningful upside from here. Patience and a high tolerance for drawdowns are prerequisites.

Analyze Navitas Semiconductor stock on TIKR Free→

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!