Key Stats for Joby Aviation Stock

- 52-Week Range: $7.43 to $20.95

- Current Price: $7.76

- Street Mean Target: $11.01

- Market Cap: $7.6 billion

- Q1 2026 Revenue: $24.2 million

- Q1 2026 Net Loss: ($110.0 million)

- Adjusted EBITDA: ($178.5 million)

- Cash and Short-Term Investments: $2.5 billion as of March 31, 2026

Value your favorite stocks like JOBY with 5 years of analysts’ forecasts using TIKR’s new Valuation Model (It’s free) >>>

The Milestone Machine That the Market Keeps Selling

There is a strange disconnect running through Joby Aviation (JOBY) right now. The company has spent 2026 checking off one milestone after another. First-ever point-to-point eVTOL flights in New York City’s history.

A demonstration over the Golden Gate Bridge. Selection into the White House-backed eIPP program covering 11 states. A Toyota manufacturing joint venture. The first flight of its FAA-conforming aircraft.

By any operational measure, Joby is further along than it has ever been. The stock just hit a 54% drawdown from its 52-week high.

The chart tells that story clearly. Shares fell sharply in early 2026, managed a partial recovery to around 25% below peak by late May, then rolled back over hard into July, reaching a new low just days ago.

The market is not really questioning whether the technology works. What it is questioning is how long the wait will be before any of these shows up in the financials. Patience is running thin.

See analysts’ growth forecasts and price targets for Joby Aviation stock (It’s free) >>>

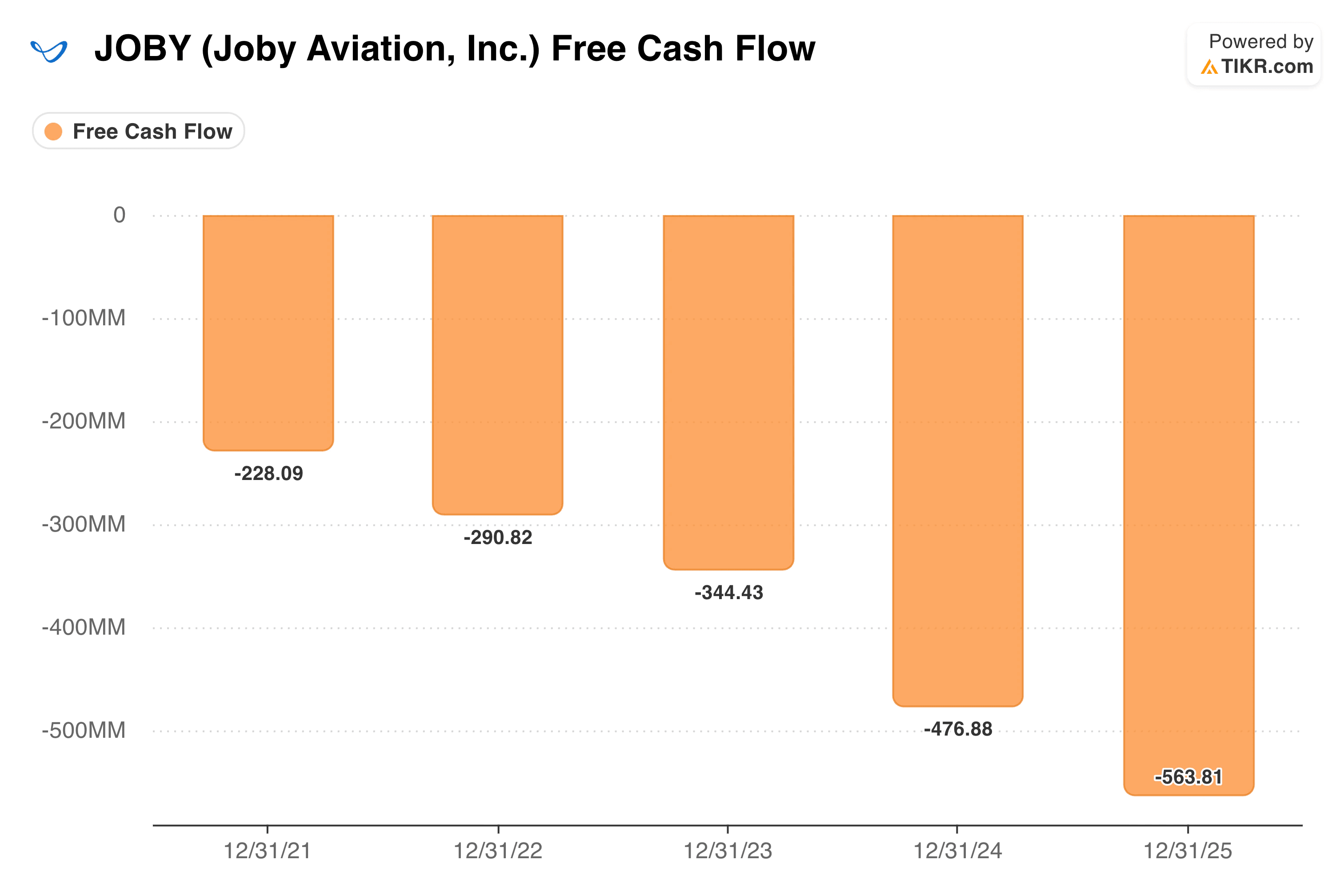

The Cash Burn Is Real, but So Is the Runway

Joby has burned more cash every single year since going public. Around $228 million in 2021, and nearly $564 million in 2025. The spending has grown each year as the company pushes deeper into FAA certification testing, manufacturing scale-up, and building the infrastructure needed to actually operate a commercial service.

What matters here is not the burn rate in isolation. It is the cash sitting behind it. Joby ended Q1 2026 with $2.5 billion in liquidity, supported by a $600 million equity offering and a $690 million convertible note issuance earlier in the year. At current spend levels, that is a meaningful runway well into 2028.

CEO JoeBen Bevirt noted in the Q1 shareholder letter that composites production is already running at more than 2.5 times the volume from a year ago.

The Toyota joint venture, announced in June, brings a manufacturing partner with the scale to support a genuine commercial ramp. None of this turns into revenue overnight. But Joby is spending its capital on real progress.

Estimate a company’s fair value instantly (Free with TIKR) >>>

What Wall Street Thinks About JOBY Stock

Nine analysts cover Joby. Two rate it a Buy, five a Hold, and two a Sell. The mean price target sits around $11, implying roughly 40% upside from where the stock trades today.

The target-to-price ratio has stretched to nearly 142%. Not because analysts have turned bullish, but because the stock has fallen faster than anyone has cut their numbers.

Goldman Sachs carries a Sell, citing valuation and execution concerns. Morgan Stanley and Canaccord have trimmed targets but stayed at Hold. The closest peer is Archer Aviation, which is also pursuing FAA certification but trails Joby on overall progress.

A Jefferies consumer survey from June found that riders were willing to pay around $90 for a 15-minute flight that saved 45 minutes of travel time. The demand thesis has real legs, even if commercialization is still a few years out.

Should You Invest in Joby Aviation?

Joby is a long-duration bet on a mode of transportation that does not yet exist at a commercial scale. Investors need to be clear-eyed about that going in. The cash position is solid, the FAA progress is real, and the operational milestones this year have been genuinely impressive.

The risks are real, too: ongoing cash burn, timeline uncertainty, and a path to profitability that is still years away. This is a stock for patient investors with a long time horizon and a high tolerance for volatility.

See how JOBY performs against its peers in TIKR (It’s free!) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!