Key Stats for Marathon Petroleum Stock

- Past-Week Performance: +11.6%

- 52-Week Range: $115.1 to $228.6

- Current Price: $215.2

What Happened?

What started as a refining margin recovery story has become a structural cash generation thesis, as Marathon Petroleum (MPC), the largest US refiner by capacity at 3 million barrels per day — printed Q4 adjusted EPS of $4.07 against a $2.88 estimate while trading at $215.23.

On February 3, CEO Maryann Mannen disclosed that refining margin, the per-barrel profit spread between crude input costs and refined product prices, surged 44% to $18.65 in Q4, with throughput records at the 606,000-bpd Garyville and 253,000-bpd Robinson refineries driving R&M segment EBITDA to $2 billion.

MPC’s 114% capture rate, a metric measuring how much of the available market margin the refiner actually converts to profit, outpaced the Q4 industry rebound that lifted peers Valero and PBF Energy, with MPC’s fully integrated logistics network across 13 refineries enabling optimization no single-region competitor can replicate.

Meanwhile, CFO Maria Khoury stated on the Q4 earnings call that “cash flow from operations, excluding working capital changes, was $2.7 billion for the quarter and $8.7 billion for the year,” the strongest quarterly result in two years, underpinned by the company’s sour crude advantage as Venezuelan and Canadian differentials widened simultaneously.

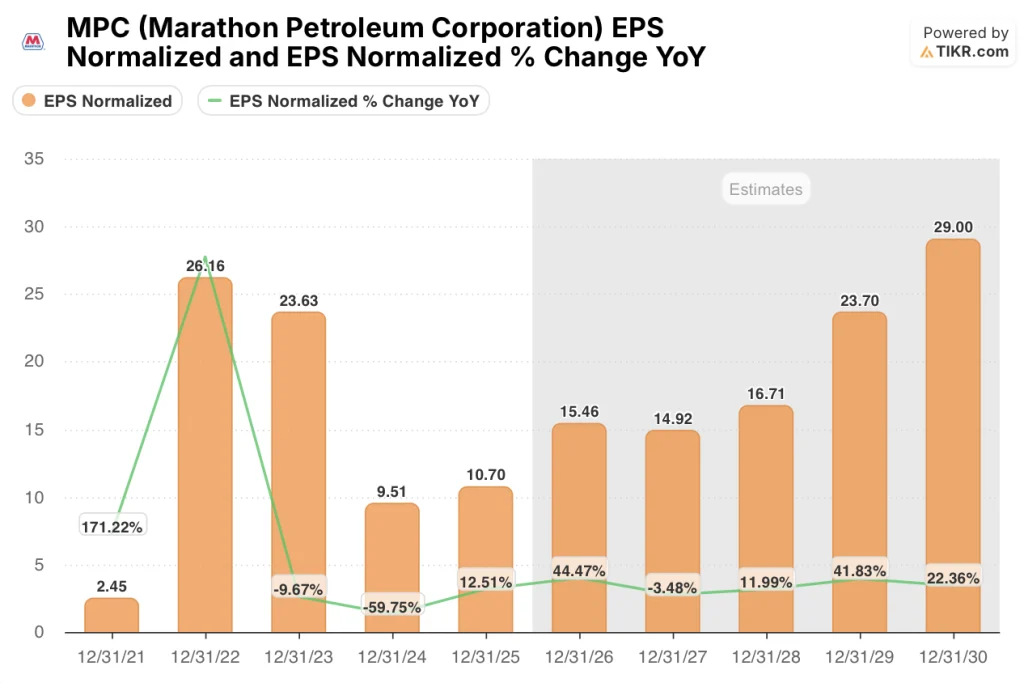

With MPLX, MPC’s midstream partnership handling 10% of all US natural gas production, targeting $3.5 billion in annual distributions to MPC while refining capex falls 20% in 2026, the company is positioned to return capital at 2025’s $4.5 billion pace or better while the 2026 normalized EPS estimate of $15.46 implies 44.5% earnings growth the current price has not absorbed.

Wall Street’s Take on MPC Stock

The 44% surge in refining margins that drove MPC’s Q4 beat — from $12.96 per barrel a year ago to $18.65 — directly repositions the company’s 2026 earnings trajectory, with the street now modeling $15.46 in normalized EPS against a 2025 actual of $10.70, a 44.5% forward jump that the current price does not reflect.

That inflection rests on two reinforcing pillars: refining utilization running at 95% with throughput records at Garyville and Robinson in Q4, and a crude slate tilting heavier as Venezuelan and Canadian sour differentials widen, with every $1 move in sour spreads worth $500 million annually to MPC’s bottom line.

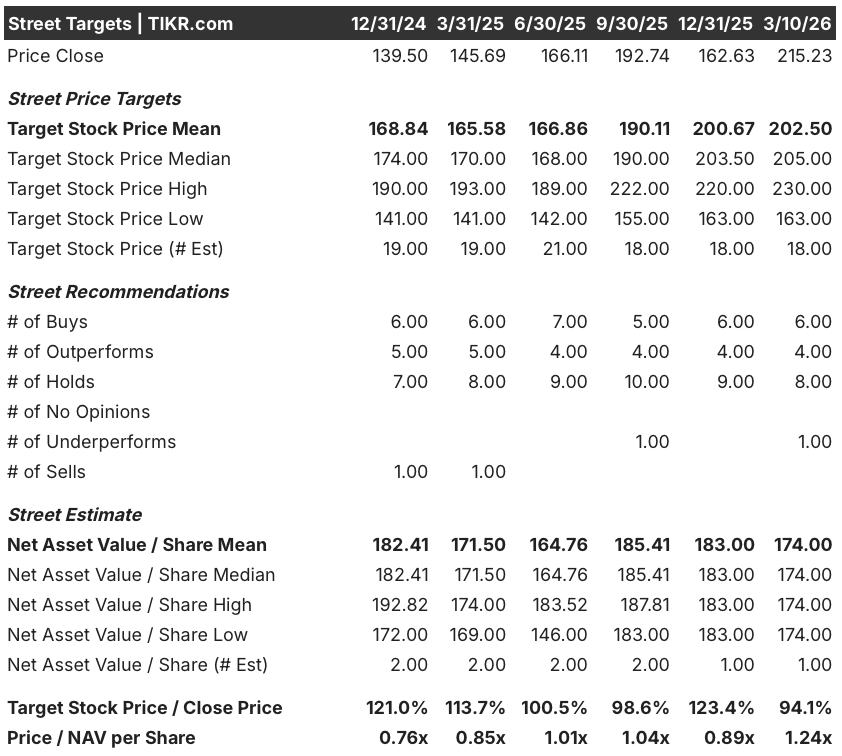

Fourteen analysts currently cover MPC, with 6 buys, 4 outperforms, 8 holds, and 1 underperform; their mean price target of $202.50 sits 5.9% below the current price of $215.23, a rare configuration where the stock has already outrun consensus despite the forward earnings case remaining largely unpriced.

The spread between the street’s low target of $163.00 and high of $230.00 captures the precise binary the story presents: the low reflects a margin mean-reversion scenario where crack spreads retreat as they did in 2024, while the high tracks the structural tightening thesis Mannen articulated: regional refinery closures, limited new capacity, and Venezuelan crude unlocking a wider sour differential permanently.

What Does the Valuation Model Say?

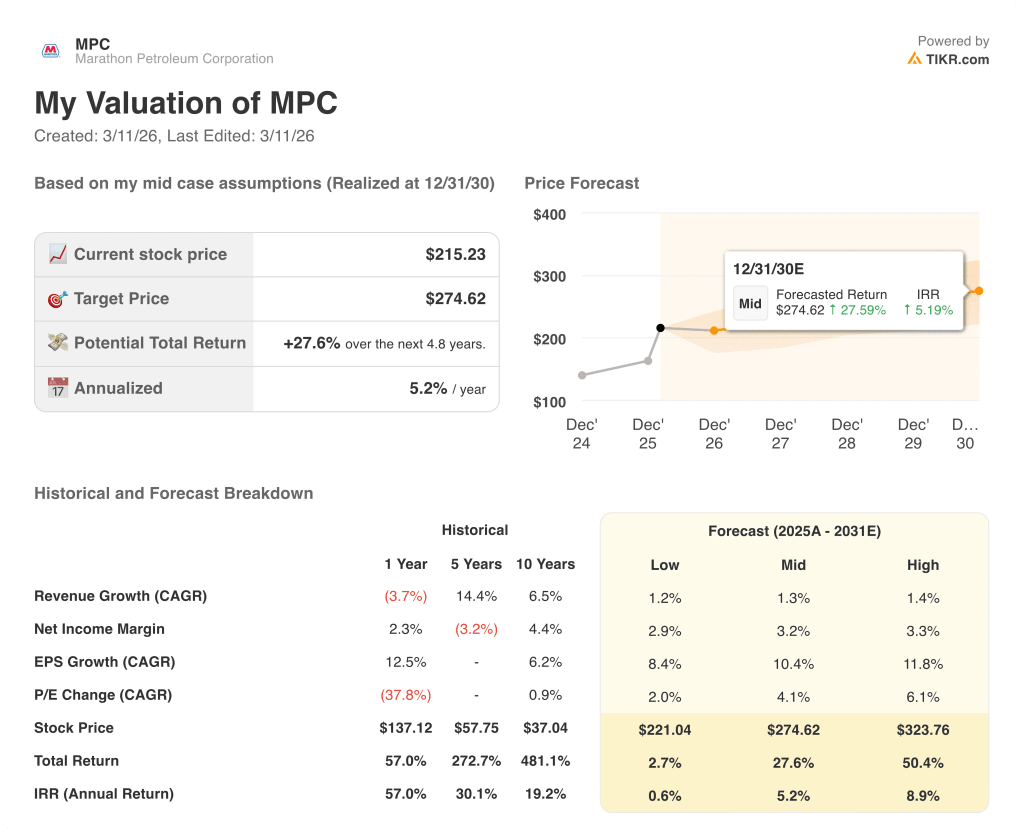

The TIKR mid-case model prices MPC at $274.62 by December 31, 2030, implying 27.6% total return at a 5.2% IRR, anchored to a 10.4% EPS CAGR assumption that the 2026 estimate of $15.46 is already tracking ahead of on a single-year basis.

The market is pricing MPC as a mean-reversion refiner, but the $8.3 billion in 2025 operating cash flow — generated in a year management itself called back-end loaded — suggests the normalized earnings floor is materially higher than the multiple implies.

MPC’s 95% Q4 utilization, throughput records at two flagship refineries, and 114% capture rate confirm the operational platform behind the TIKR model’s mid-teens EPS CAGR is already in place and performing above plan.

CEO Mannen’s direct statement that 2026 capital returns should match or exceed 2025’s $4.5 billion, while MPLX distributions alone are projected to exceed $3.5 billion annually which signals that this is a capital return story the market is misreading as a commodity trade.

The risk is crack spread compression: the 2026 EBITDA margin assumption of 10.5% — up from 8.8% in 2025 — collapses if the refining margin environment reverts toward 2024 lows, which would pressure the $15.46 EPS estimate and invalidate the TIKR model’s core input.

Q1 2026 results are the confirmation event: watch refining margin per barrel against the Q4 2025 print of $18.65 and utilization against the guided 85%, since any narrowing of sour differentials or utilization miss would signal the 44.5% EPS growth assumption is front-loaded rather than structural.

Should You Invest in Marathon Petroleum Corporation?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up MPC stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Marathon Petroleum Corporation alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze MPC stock on TIKR for Free →