Key Stats for Archer-Daniels-Midland Stock

- This Week Performance: 2.9%

- 52-Week Range: $40.1 to $70.5

- Current Price: $69.4

What Happened?

Archer-Daniels-Midland (ADM), the global grain merchant and agricultural processor, stands at a potential earnings inflection point as biofuel policy clarity approaches, with shares recovering to $69.39 after crashing to a 52-week low of $40.98.

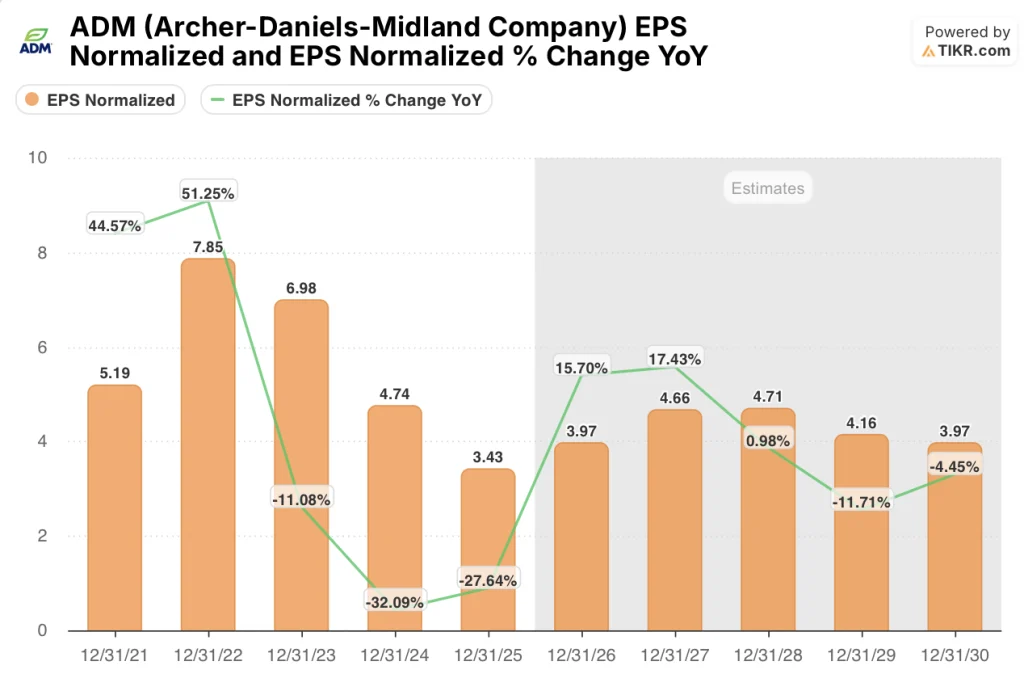

On February 3, ADM reported Q4 2025 adjusted EPS of $0.87, beating the LSEG consensus estimate of $0.80, even as full-year adjusted EPS of $3.43 reflected a bruising year of compressed soybean crush margins and muted North American export volumes.

The sharpest damage came from the Crushing subsegment, where operating profit collapsed 81% for full-year 2025 as weak soybean oil demand tied to unresolved U.S. biofuel blending quotas, known as Renewable Volume Obligations (RVOs), gutted margins across both North and South America, a deterioration that also pressured rival Bunge.

CEO Juan Luciano stated on the Q4 2025 earnings call that “recent progress with China trade relations, combined with the expectation of pending U.S. biofuel policy clarity, should support an increasingly constructive market environment throughout this year, particularly for our AS&O business.”

ADM’s 2026 adjusted EPS guidance of $3.60 to $4.25, underpinned by a $500 million to $750 million multi-year cost savings program, an estimated $100 million tailwind from the 45Z clean fuel production tax credit, and resumed Chinese soybean purchases, positions the company to reaccelerate earnings once Washington finalizes the biofuel mandates that have kept crush margins depressed since 2024.

Wall Street’s Take on ADM Stock

The RVO resolution that crushed ADM’s soybean processing margins through 2025 is now the same catalyst that makes the 2026 earnings recovery thesis compelling, with biofuel policy clarity directly unlocking crush margin normalization.

Normalized EPS bottomed at $3.43 in 2025 after falling 27.6% year-over-year, but the TIKR model projects a 15.7% recovery to $3.97 in 2026 and a further 17.4% jump to $4.66 in 2027 as crush margins and Chinese soybean volumes normalize.

Wall Street remains unconvinced: 11 analysts covering ADM carry a mean price target of $60.73, implying 12.5% downside from the current $69.39, with just 1 buy against 7 holds and 3 underperforms, reflecting deep skepticism about the timing of the biofuel policy catalyst.

The spread between the $50.00 low target and the $70.00 high target tells the whole story: bears see continued RVO delay and compressed crush margins, while bulls see the policy resolution ADM’s CEO described as “increasingly constructive” arriving in time to move the second half of 2026.

What Does the Valuation Model Say?

The TIKR mid-case model targets $73.07, implying a modest 5.3% total return over roughly 4.8 years at a 1.1% annualized IRR. The model prices in 4.1% revenue CAGR and EBIT margin recovery from 1.8% in 2025 to 2.3% in 2026, driven by the same RVO clarity and China trade normalization already outlined by management.

The market prices ADM as though trough margins are permanent, but EBIT collapsed 31.3% in 2025 specifically because biofuel policy was unresolved, not because the underlying crush infrastructure deteriorated.

ADM’s Crushing subsegment set Q4 2025 record global crush volumes even as margins were depressed, proving the operational capacity to capture upside the moment cash margins normalize.

CEO Juan Luciano’s confirmation on February 25 at the BofA conference that China has already satisfied its initial 12 million ton purchase commitment signals that the trade flow normalization underpinning the 2026 EPS recovery is already in motion.

The risk is straightforward: if the Trump administration delays RVO finalization beyond mid-2026, ADM’s own guidance flags the consequence directly, with the company projecting flat crush margins at the low end of its $3.60 to $4.25 adjusted EPS range.

The single number to watch is Q1 2026 crush margin, which management already disclosed will mirror the depressed Q4 2025 level, making Q2 guidance the first real confirmation of whether the RVO catalyst is actually flowing through to cash margins.

Should You Invest in Archer-Daniels-Midland Company?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up ADM stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Archer-Daniels-Midland Company alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze ADM stock on TIKR for Free →