Key Takeaways:

- With a 6.7% dividend yield, Altria ranks as one of the top-paying large-cap dividend stocks in the market right now.

- Even with analysts forecasting low-single-digits annual earnings and dividend growth, Altria could still be a good stock today for dividend investors.

- Some analysts think the stock has as much as 20% upside from here.

- Get accurate financial data on over 100,000 global stocks for free on TIKR >>>

Altria stock is up 30% this year, but even after the climb in its share price, it could be a good stock for dividend investors to buy and hold today.

With a 6.7% dividend and a 50+ year track record of dividend increases, the stock still makes a strong case.

Why Is Altria‘s Stock Up 30% This Year?

Altria has been on a tear recently due to strong business developments, and an overall market preference for safe stocks amidst uncertainty:

- Growth in Smoke-Free Product Segments: In Q1 2025, Altria reported an 18% year-over-year increase in shipment volume for its oral nicotine pouch brand, on!, which now holds an 8.8% share of the U.S. oral tobacco category. This growth in smoke-free products has helped offset declines in traditional cigarette sales.

- Strong Return of Capital to Shareholders: In Q1 2025, Altria paid out $1.7 billion in dividends and repurchased $326 million worth of shares. This consistent return of capital underscores Altria’s commitment to shareholder value.

- Resilience Amid Regulatory Challenges: Despite facing regulatory headwinds, including an $873 million non-cash impairment charge related to its e-cigarette business, NJOY, Altria’s core operations have demonstrated resilience. Adjusted earnings per share (EPS) rose 6% year-over-year to $1.23 in Q1 2025, which is strong growth for a mature business like Altria.

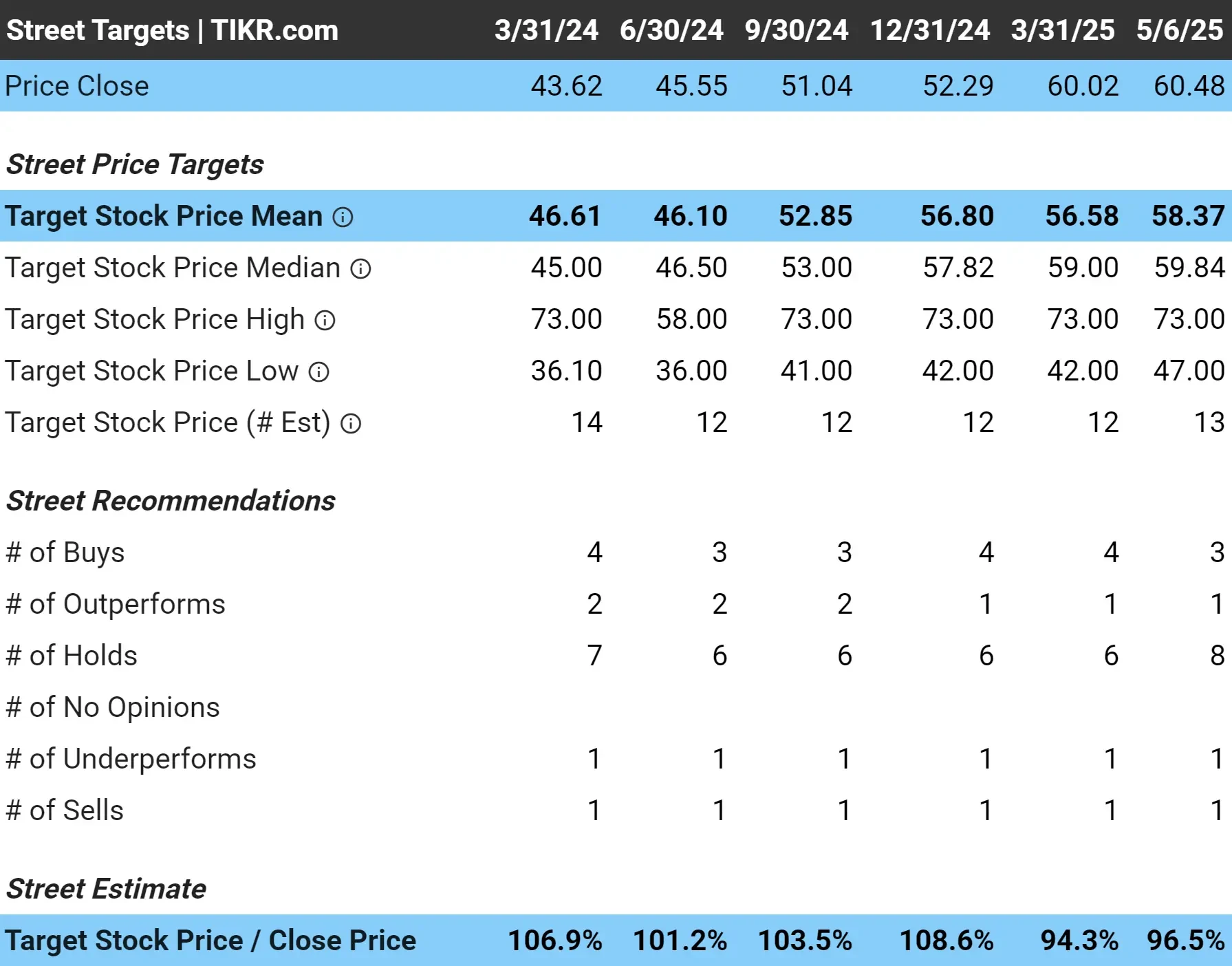

Analysts Think the Stock is Fairly Valued Today

The average analyst price target for Altria is $58/share today.

With Altria trading at $60/share today, it’s likely that the stock is just about fairly valued.

However, the high-end price target estimate sits at $73/share, which means that the stock could have 20% upside today if it could reach $73/share.

Altria’s 6.7% dividend alone offers meaningful returns, and if investor sentiment shifts or fundamentals improve, the stock could still deliver a surprise on the upside.

See why Altria looks fairly valued today with TIKR (It’s free) >>>

1: Dividend Yield

Altria’s dividend yield hit a recent low of 6.7%, which means there isn’t the same kind of opportunity for the stock today as there used to be.

That’s a noticeable dip from its historical average of around 7.9% over the past five years, with a high of 9.7%.

Even at this lower level, Altria’s dividend yield still stands well above the market average, making it an attractive large-cap dividend stock.

Find high-quality dividend stocks that look even better than Altria today. (It’s free) >>>

2: Dividend Safety

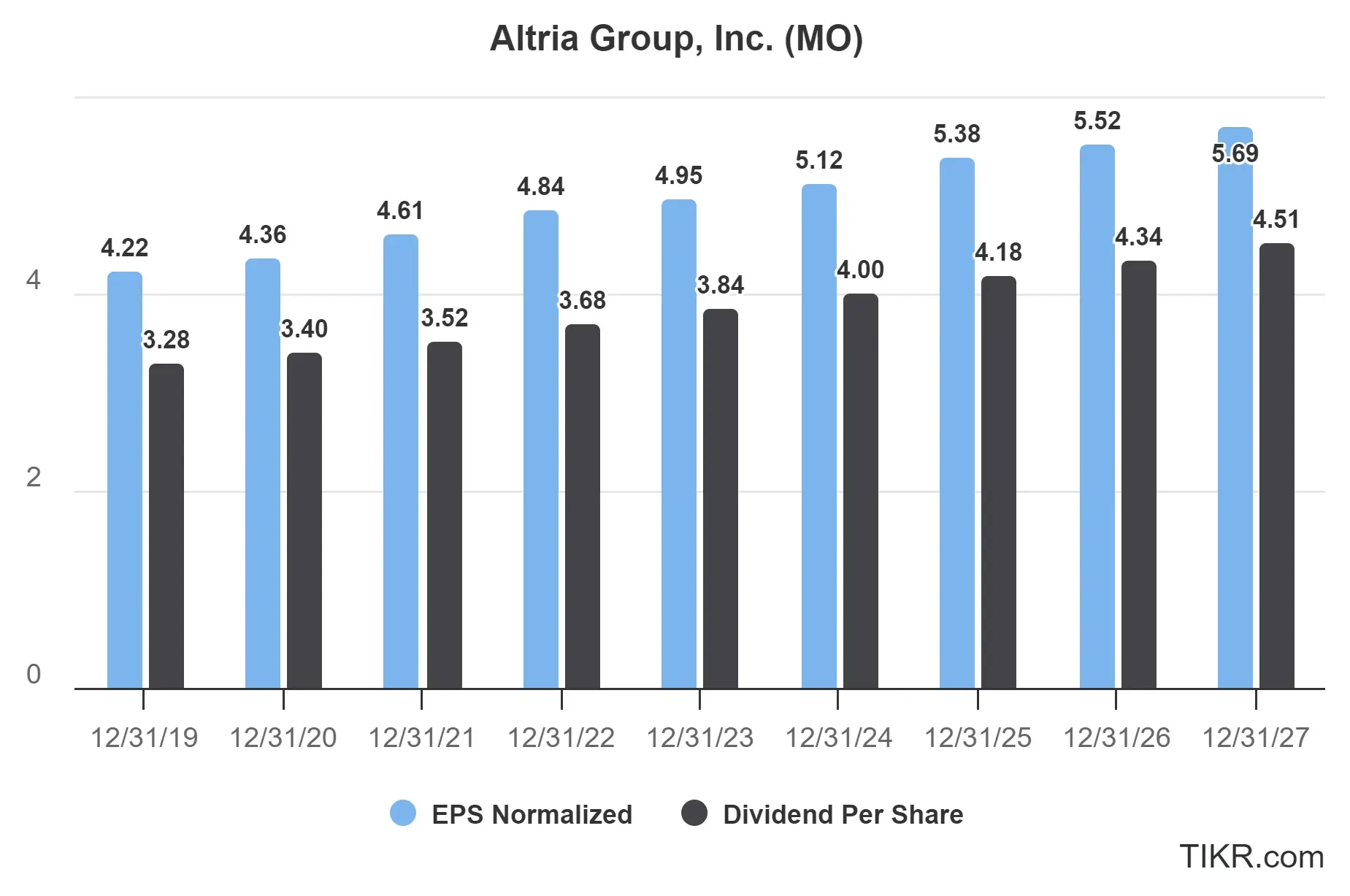

In 2025, Altria is expected to earn $5.38 in EPS and pay out $4.18 in dividends. That works out to a payout ratio of about 78%.

We like to see companies with a payout ratio below 70%, so Altria’s payout ratio is on the higher end of what you’d want to see. However, with the business’s consistent earnings and cash flow, it isn’t a red flag for investors. This is a business that prioritizes sending cash back to shareholders, and it’s still doing that comfortably.

Earnings and dividends are both expected to grow slowly over the next few years. The payout ratio might creep up a little, but for now, there’s still enough of a cushion to keep the dividend going strong.

See Altria’s full growth forecast and analyst estimates. (It’s free) >>>

3: Dividend Growth Potential

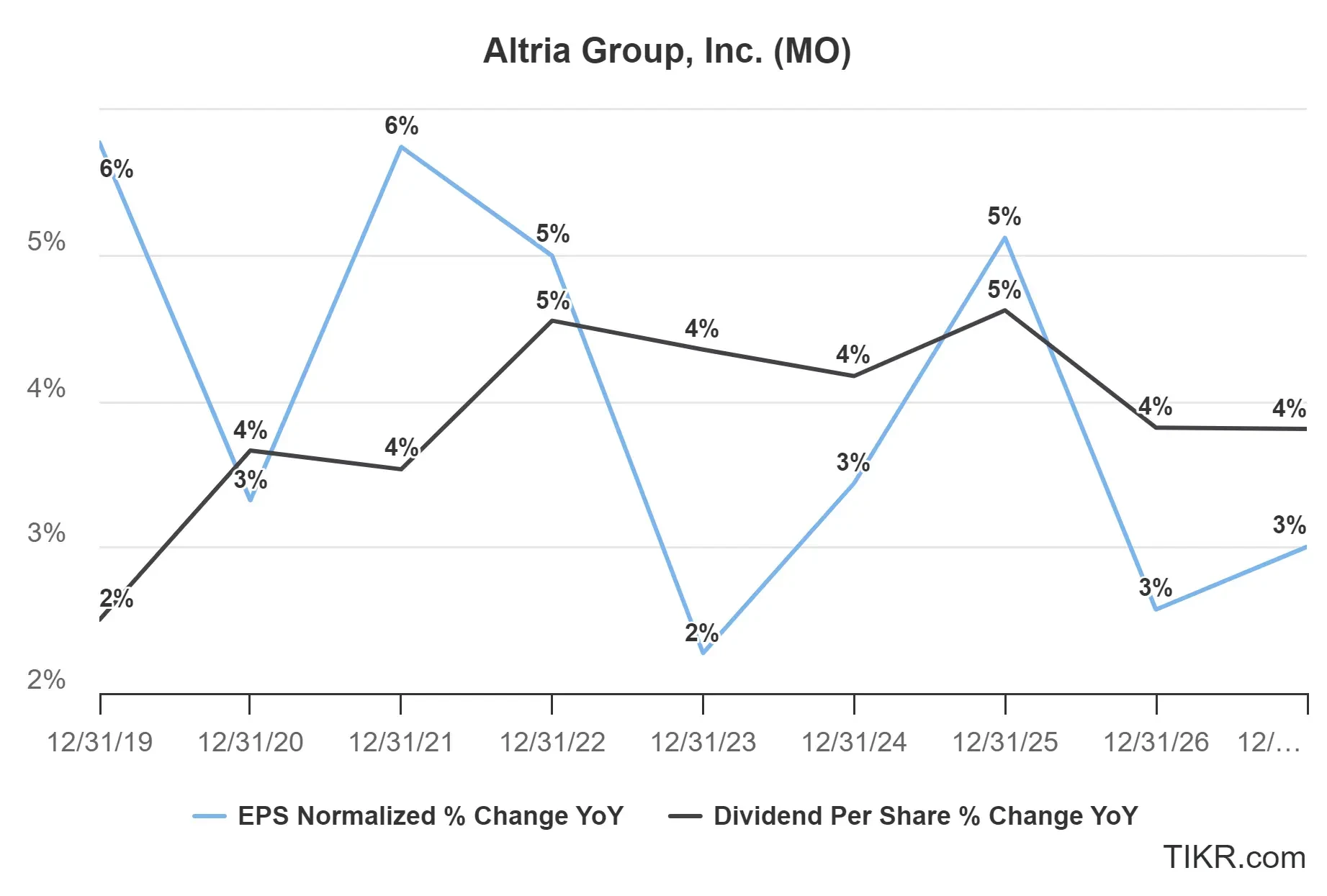

Altria is expected to grow both earnings and dividends in the low to mid-single digits over the next 3 years.

This is pretty much in line with how earnings and dividends have grown over the last 5 years. This slow and steady approach is great for long-term dividend investors, or any investors looking for stability with a recession-proof stock.

TIKR Takeaway

Altria looks to be fairly valued today, but it still offers a 6.7% dividend yield and is repurchasing shares.

Analysts don’t expect explosive upside, but with earnings and dividends growing in sync and some seeing as much as 20% potential upside, there’s still a solid total return story over the long-term for Altria.

The TIKR Terminal offers industry-leading financial data on over 100,000 stocks and was built for investors who think of buying stocks as buying a piece of a business.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!