Key Takeaways:

- J&J has raised its dividend for 62 straight years, with a projected 2027 payout ratio of 46%, showing it has plenty of room to keep growing its payout.

- The stock’s 3.04% yield is near the low end of the past year, but still offers solid income for a company with this level of consistency and strength.

- Earnings are expected to grow 6.5% annually through 2027, driven by pharma and MedTech, giving long-term investors a path to steady returns.

Johnson & Johnson is one of the largest and most diversified healthcare companies in the world, with operations across pharmaceuticals, medical devices, and ongoing value from its retained equity stake in its consumer health spin-off, Kenvue.

The stock has underperformed in recent years due to legal headwinds and the distraction of the spin-off. But underneath that, J&J has continued doing what it does best: growing earnings steadily and raising its dividend like clockwork.

Today, the stock isn’t trading at fire-sale levels, and the dividend yield has come down as the price has climbed. But it still offers a rare combination of stability, balance sheet strength, and consistent long-term performance.

For investors who value predictability over hype, J&J remains a reliable name to own.

Analysts Think the Stock is Undervalued Today

Johnson & Johnson currently trades around $168/share, but based on analysts’ consensus estimates used in our guided valuation model, the stock could rise to about $208/share by the end of 2027.

That implies total returns of 23.4%, or about 9% per year, if the business delivers 4.5% annual revenue growth and maintains strong operating margins above 33%.

This assumes a reasonable valuation ratio of about 15 times forward earnings, which is below J&J’s typical historical P/E range. Combined with a strong dividend and reliable cash flow, analysts think the current price may represent a long-term opportunity.

Value any stock in less than 60 seconds with TIKR (It’s free) >>>

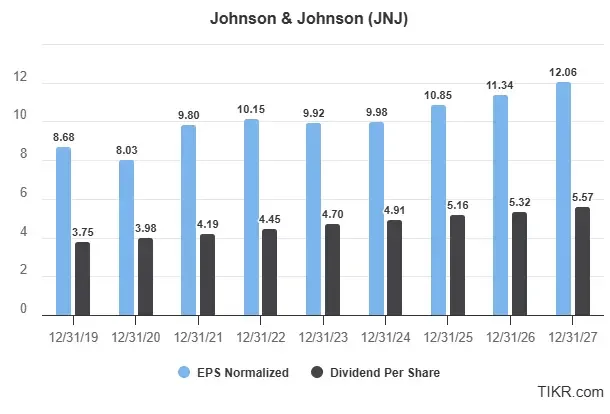

A 62-Year Dividend Growth Streak With Plenty of Gas Left in the Tank

Johnson & Johnson is expected to earn $12.06 per share and pay out $5.57 in dividends by 2027, putting the payout ratio at just 46%. That’s a healthy cushion for continued dividend growth.

The company has now raised its dividend for 62 consecutive years, placing it firmly in Dividend King territory. This kind of consistency reflects a strong commitment to rewarding shareholders.

From 2024 to 2027, normalized EPS is expected to grow at a compound annual growth rate (CAGR) of about 6.5%, while dividends per share are forecast to rise at a 4.3% CAGR. That positive spread between earnings and dividend growth suggests that the company will continue to have room for dividend increases, even as J&J funds innovation and potential acquisitions.

Importantly, this isn’t just a mature company milking legacy products. J&J’s next leg of growth will likely come from high-margin, IP-protected drugs in immunology and neuroscience, which are two of the most promising areas in pharma, as well as its expanding MedTech segment, which includes surgical robotics and digital surgery platforms.

Also worth noting: J&J maintains one of the strongest balance sheets in the Healthcare sector, with an AAA credit rating, low net debt, and over $20 billion in operating cash flow annually. That financial strength gives it the ability to invest aggressively while still returning capital to shareholders.

See Johnson & Johnson’s full growth forecast and analyst estimates. (It’s free) >>>

JNJ’s Dividend Yield Has Pulled Back, But Still a Reliable 3%

Johnson & Johnson’s forward dividend yield is currently 3.04%. That’s slightly above its 5-year average of 2.87%, but it is nearly the lowest dividend yield the company has offered in the past year. This recent drop in the dividend yield is due to the stock price appreciating, which has lowered the yield.

Even after the recent rally, the stock still trades well below its all-time highs. The market seems to be slowly warming back up to J&J as legal risks ease and growth in its MedTech segment picks up.

It’s not a bargain, but it’s still a solid price for a company with this kind of stability, cash flow, and long-term earnings power.

Wall Street Analysts Are Bullish on These 5 Undervalued Compounders With Market-Beating Potential

TIKR just released a new free report on 5 compounders that appear undervalued, have beaten the market in the past, and could continue to outperform on a 1-5 year timeline based on analysts’ estimates.

Inside, you’ll get a breakdown of 5 high-quality businesses with:

- Strong revenue growth and durable competitive advantages

- Attractive valuations based on forward earnings and expected earnings growth

- Long-term upside potential backed by analyst forecasts and TIKR’s valuation models

These are the kinds of stocks that can deliver massive long-term returns, especially if you catch them while they’re still trading at a discount.

Whether you’re a long-term investor or just looking for great businesses trading below fair value, this report will help you zero in on high-upside opportunities.

Click here to sign up for TIKR and get our full report on 5 undervalued compounders completely free.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!