WiseTech Global (WTC) is a global software company focused on logistics execution and supply chain management. Its flagship platform, CargoWise, is used by freight forwarders, customs brokers, and logistics providers to manage complex international trade workflows, from booking and customs clearance to compliance and billing. The company serves many of the world’s largest logistics operators, embedding itself deeply into mission-critical processes where switching costs are high and operational reliability matters.

Find out what a stock’s really worth in under 60 seconds with TIKR’s new Valuation Model (It’s free)>>>

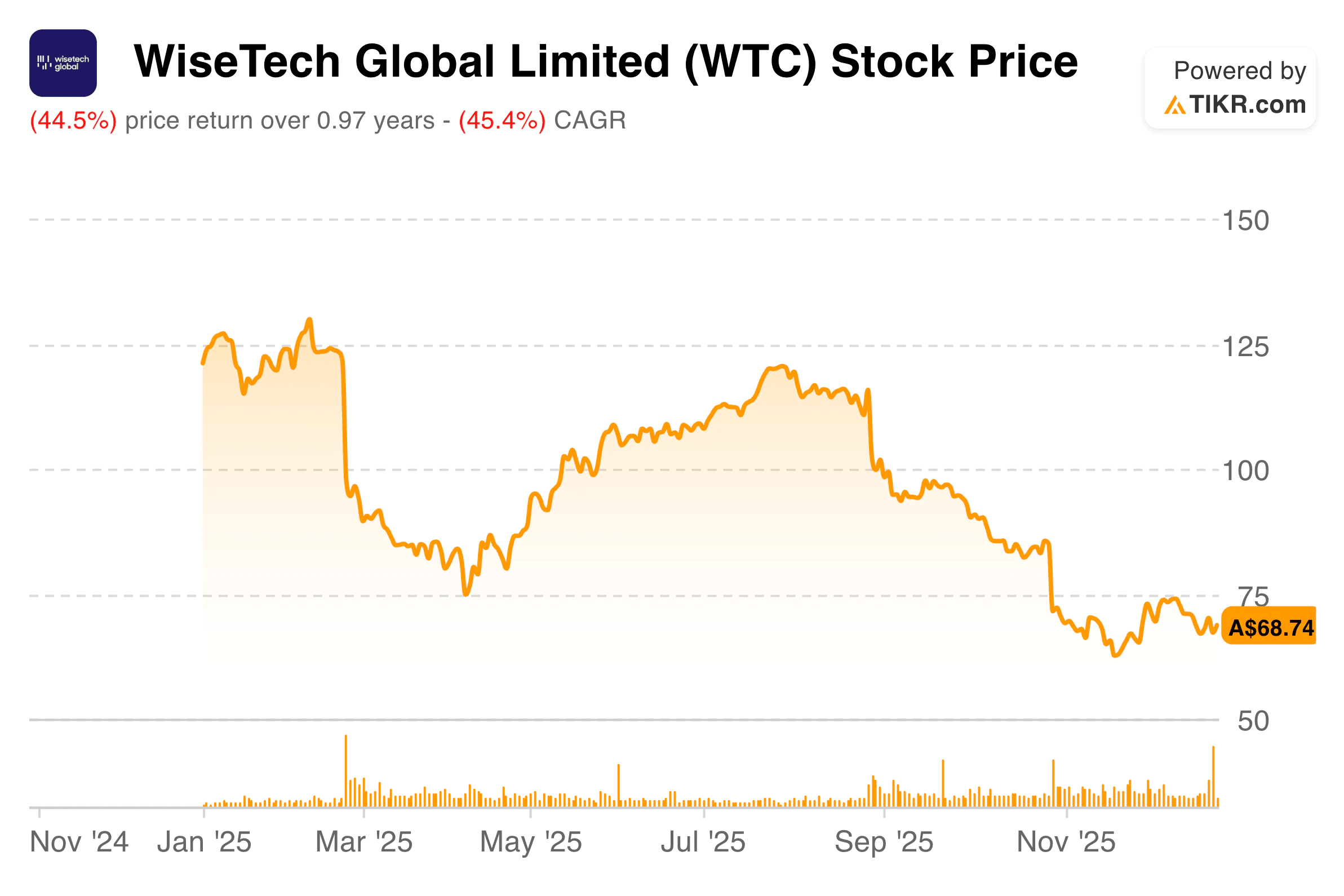

Over the past year, WiseTech’s stock has struggled, falling sharply after a period of strong outperformance. Investor sentiment cooled as concerns around valuation, acquisition integration, and growth sustainability came to the forefront. Despite continued revenue growth and solid margins, the market has reassessed how much future growth it is willing to pay for, especially amid broader volatility in high-multiple software stocks.

Heading into the next fiscal year, WiseTech is in an interesting position. The stock price reflects a reset in expectations, while the underlying business continues to grow at a healthy pace. Analysts are now focused less on headline growth and more on execution, margin durability, and whether WiseTech can continue compounding earnings as its acquisition strategy matures.

Quickly value any stock with TIKR’s powerful new Valuation Model (It’s free!) >>>

Financial Story

WiseTech’s financial performance remains solid despite the stock’s recent drawdown. Over the past year, revenue has grown by approximately 11%. Longer-term growth remains strong, with a five-year revenue CAGR above 20%. The company continues to benefit from recurring revenue tied to CargoWise usage, as customers expand volumes and functionality over time.

| Metric | FY 2025 |

|---|---|

| Revenue Growth (1Y CAGR) | 10.9% |

| Revenue Growth (5Y CAGR) | 20.2% |

| Net Income Margin | ~27% |

| EPS Growth (5Y CAGR) | ~38% |

| Current Share Price | $46.05 |

| Mid-Case Target Price | $139.99 |

| Potential Total Return | ~204% |

| Annualized Return (Mid-Case) | ~28% |

Profitability remains a key strength. Net income margins have historically been in the high-20% range, reflecting the scalability of the software model and disciplined cost control. Even as WiseTech continues to invest in product development and acquisitions, margins have remained resilient, underscoring the operating leverage built into the platform.

Earnings growth has been robust, with EPS compounding at more than 20% annually over multi-year periods. While near-term P/E compression has weighed on returns, analysts expect earnings growth to remain strong as revenue scales and integration costs normalize. Cash generation continues to support reinvestment, acquisitions, and balance sheet flexibility.

Look up WiseTech Global’s full financial results & estimates (It’s free)>>>

Broader Market Context

The logistics software market continues to benefit from long-term structural trends. Global trade remains complex, regulatory requirements are increasing, and logistics providers are under pressure to digitize workflows and improve efficiency. These trends favor integrated platforms like CargoWise, which can replace fragmented legacy systems with a single source of truth.

At the same time, the software sector has entered a more selective phase. Investors are placing greater emphasis on profitability, free cash flow, and execution rather than pure growth. For WiseTech, this environment raises the bar and underscores the durability of its business model relative to less entrenched SaaS peers.

1. CargoWise and Switching Costs

CargoWise sits at the center of customers’ daily operations, handling high-stakes logistics workflows where errors are costly. Once implemented, the platform becomes deeply embedded, making switching disruptive and expensive. This creates strong customer retention and a steady base of recurring revenue.

As customers grow volumes or expand services, WiseTech captures incremental revenue without proportional cost increases. That dynamic supports margin expansion over time and reinforces the platform’s competitive moat, especially among large global freight forwarders.

2. Acquisition Strategy and Scale

WiseTech has historically grown through a mix of organic expansion and targeted acquisitions. These acquisitions extend CargoWise’s functionality, geographic reach, and regulatory coverage, strengthening the platform’s global footprint. While integration risk is real, management has demonstrated the ability to integrate acquisitions into the core product over time.

The recent stock pullback reflects investor caution about the pace of acquisitions and execution. However, if integrations continue to enhance the platform rather than dilute focus, WiseTech’s scale advantage could widen further as competitors struggle to match its breadth.

Value stocks like WiseTech Global in less than 60 seconds with TIKR (It’s free) >>>

3. Valuation Reset and Earnings Leverage

The valuation reset has shifted the investment conversation. With shares trading well below prior highs, future returns are now more dependent on earnings growth than multiple expansion. Under mid-case assumptions, analysts see the potential for over 200% total upside by 2030, driven by revenue growth near the mid-20% range and sustained margins.

That outlook assumes WiseTech maintains discipline, integrates acquisitions effectively, and continues to expand among existing customers. If those pieces fall into place, earnings growth could remain the dominant driver of shareholder returns over the next several years.

The TIKR Takeaway

WiseTech Global appears to be a business whose fundamentals remain intact despite shifting market sentiment. The company continues to grow revenue, generate strong margins, and compound earnings, while the stock price now reflects more conservative expectations. For investors focused on long-term cash generation and platform durability, the current setup highlights the gap between operational performance and market perception.

Should You Buy, Sell, or Hold WiseTech Global Stock in 2025?

From here, investors are likely to focus on execution rather than narratives. Key areas to watch include organic growth trends, integration of acquisitions, margin stability, and free cash flow conversion. How WiseTech balances reinvestment with discipline will shape whether the company can convert its strong business model into sustained shareholder returns in a more demanding market environment.

How Much Upside Does WiseTech Global Stock Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

Find out what your favorite stocks are really worth (Free with TIKR) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!