Evolution Mining Limited (EVN) is a mid-tier mining company focused primarily on gold, with growing exposure to copper and silver. The company operates a diversified portfolio of assets across Australia and Canada, including six gold mines and two copper operations. Evolution’s strategy is straightforward as it prioritizes long-life assets, disciplined capital allocation, and steady cash generation over aggressive production growth. That approach has helped the company build a resilient operating base across multiple commodity cycles.

Find out what a stock’s really worth in under 60 seconds with TIKR’s new Valuation Model (It’s free)>>>

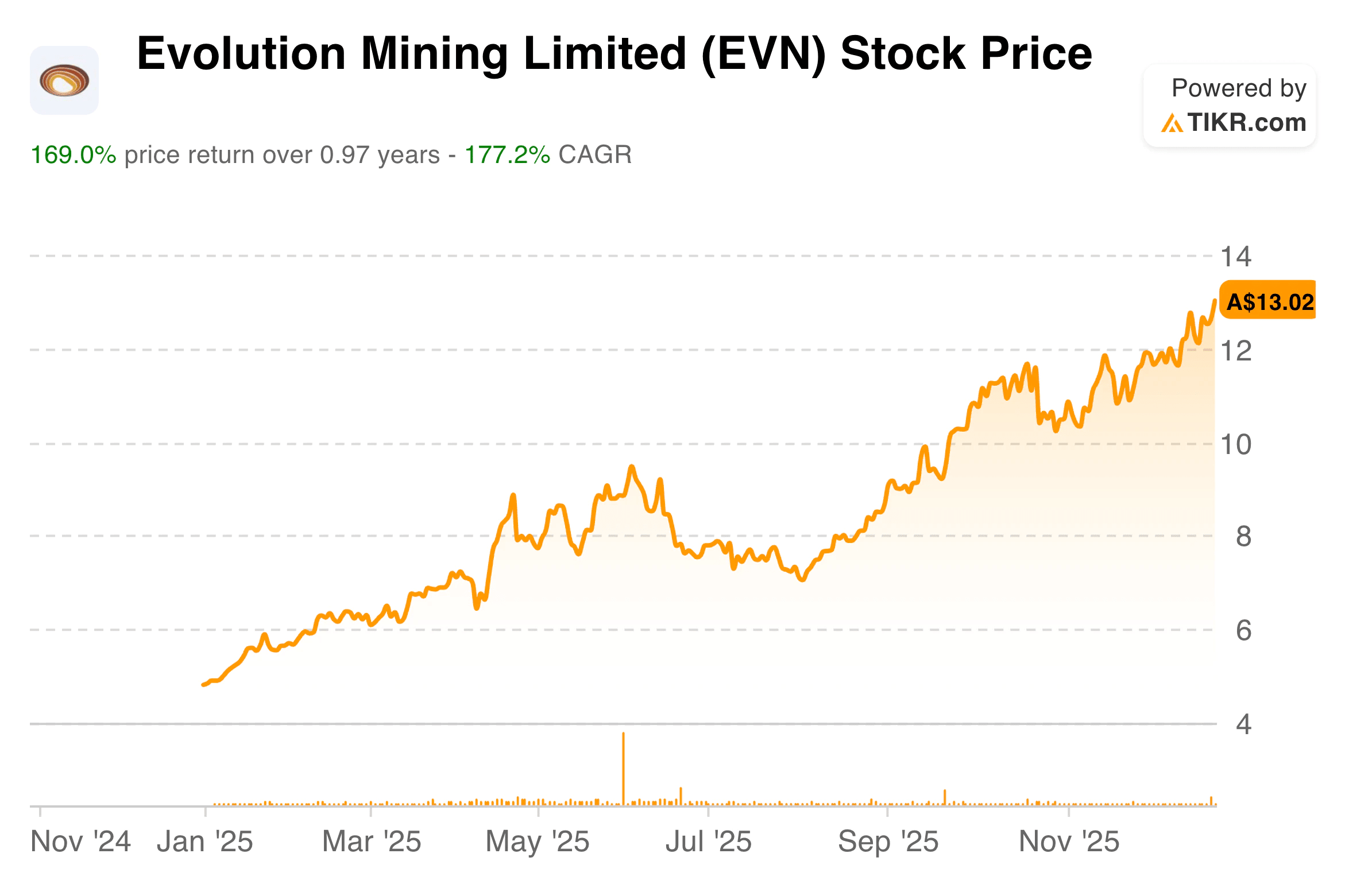

Investor sentiment around Evolution has improved meaningfully over the past year. The stock has delivered a sharp rally, reflecting both stronger commodity pricing and clearer evidence that operational execution is translating into real earnings power. After years of being viewed as a cyclical producer with uneven profitability, Evolution is increasingly seen as a business that can deliver consistent margins and cash flow without chasing production growth at all costs.

Heading into the new fiscal year, the setup is more balanced than it has been in some time. The stock is no longer deeply discounted, but expectations have also reset to a more realistic level. Evolution enters this period with higher margins, a cleaner earnings profile, and a production base that supports stability rather than volatility. That combination puts greater emphasis on execution, cost discipline, and capital returns rather than headline growth.

Quickly value any stock with TIKR’s powerful new Valuation Model (It’s free!) >>>

Financial Story

Evolution’s most recent financial results marked a clear step change in profitability. Revenue reached AU$4.35 billion, up 35% year over year, driven by a combination of stronger realized prices and steady production volumes across its asset base. This top-line growth provided the foundation for significantly improved operating leverage throughout the business.

| Metric | FY 2025 |

|---|---|

| Revenue | AU$4.35B |

| Revenue Growth (YoY) | 35% |

| Net Income | AU$926.2M |

| Net Income Growth (YoY) | 119% |

| Profit Margin | 21% |

| EPS | AU$0.47 |

| Gold Production | 750.5 koz |

| Copper Production | 76,261 t |

| Silver Production | 827.0 koz |

| Revenue vs. Estimates | +1.1% |

| EPS vs. Estimates | +4.8% |

That leverage was evident in earnings. Net income rose to AU$926.2 million, representing a 119% increase from the prior year. Profit margins expanded to 21%, up from 13%, reflecting improved cost absorption and a more favorable revenue mix. Earnings per share climbed to AU$0.47, more than doubling from AU$0.22 in FY24. These results were not just strong in absolute terms, they also exceeded analyst expectations, with revenue beating estimates by 1.1% and EPS coming in 4.8% ahead.

From a cost perspective, Evolution remains a relatively efficient operator, though not without areas to watch. Cost of sales accounted for roughly 64% of revenue, while non-operating costs totaled AU$506 million, highlighting that a meaningful portion of expenses still sit outside core mining activities. Looking ahead, revenue is forecast to grow around 2.0% annually over the next three years, below the broader Australian mining industry’s 4.8% expectation. That slower growth puts even greater importance on margin discipline and capital allocation.

Look up Evolution Mining’s full financial results & estimates (It’s free)>>>

Broader Market Context

The gold market has been supportive over the past year, benefiting from persistent inflation concerns, geopolitical uncertainty, and steady central bank demand. While price volatility remains a feature of the sector, gold continues to serve as a stabilizing asset in diversified portfolios. For producers like Evolution, this environment favors margin preservation over aggressive expansion.

Copper adds another layer to the story. Long-term demand tied to electrification, energy transition infrastructure, and data center buildouts continues to support constructive expectations for copper pricing. While short-term fluctuations are inevitable, Evolution’s exposure to copper provides diversification and optionality that many pure-play gold miners lack.

These macro forces shape Evolution’s near-term outlook in essential ways. With a limited production growth forecast, returns will be driven more by pricing discipline, cost control, and capital efficiency than volume expansion. In that context, Evolution’s diversified asset base and improving margin profile become more relevant than headline growth rates.

1. Production and Asset Mix

Evolution’s production profile remains steady and diversified. Gold production reached approximately 750.5 thousand ounces, up modestly from the prior year, supported by consistent output across its six gold operations. This stability reduces reliance on any single asset and helps smooth operational risk over time.

Copper production increased to 76,261 tonnes, up from 67,862 tonnes, reinforcing copper’s growing contribution to the business. Silver production also edged higher to 827 thousand ounces. While these metals are not the core drivers of earnings today, they add resilience to cash flows and reduce dependence on a single commodity price.

Importantly, Evolution has not pursued aggressive production growth for its own sake. Instead, the company has focused on optimizing existing assets, extending mine lives, and improving recoveries. That approach supports margin expansion and lowers execution risk, especially in a sector where cost overruns and capital misallocation can quickly erode shareholder value.

2. Cost Structure and Operating Leverage

The most notable shift at Evolution has been the improvement in operating leverage. As revenue expanded, costs grew more slowly, allowing margins to widen meaningfully. This dynamic reflects both favorable pricing and improved internal cost management.

That said, the expense structure still warrants attention. Non-operating costs remain a meaningful component of total expenses, suggesting there is room for further efficiency gains. As revenue growth moderates, maintaining discipline on these costs will be critical to sustaining current margin levels.

The upside is clear. With margins now firmly above historical levels, incremental revenue can translate more directly into earnings and free cash flow. That operating leverage becomes especially valuable if commodity prices remain supportive, even without significant production growth.

Value stocks like Evolution Mining in less than 60 seconds with TIKR (It’s free) >>>

3. Growth Outlook and Capital Discipline

Looking forward, Evolution’s growth profile is expected to be modest. Revenue growth of approximately 2% annually indicates a shift from expansion to optimization. This places capital allocation at the center of the investment case.

Management’s focus on balance sheet strength, disciplined reinvestment, and shareholder returns becomes more critical in this phase of the cycle. Rather than chasing new projects, Evolution appears positioned to prioritize sustaining capital, selective optimization investments, and cash flow generation.

In this context, Evolution begins to resemble a yield-oriented mining business rather than a high-growth producer. That shift may not appeal to all investors, but it aligns well with a market environment that increasingly rewards predictability, margins, and cash discipline.

The TIKR Takeaway

Evolution Mining has entered a different phase of its lifecycle. The company has moved beyond recovery mode and into a period where margins, cash flow, and capital discipline matter more than headline growth. While future returns may be more measured than during the recent rally, the business now operates on a firmer financial foundation and has clearer visibility into earnings power.

Should You Buy, Sell, or Hold Evolution Mining Stock in 2025?

For investors evaluating Evolution today, the focus is less on whether the turnaround is real and more on how durable current margins and cash flows will be through the next commodity cycle. Future performance will likely hinge on cost control, capital allocation decisions, and commodity pricing rather than production growth alone. How Evolution balances those factors will shape its long-term role within a diversified portfolio.

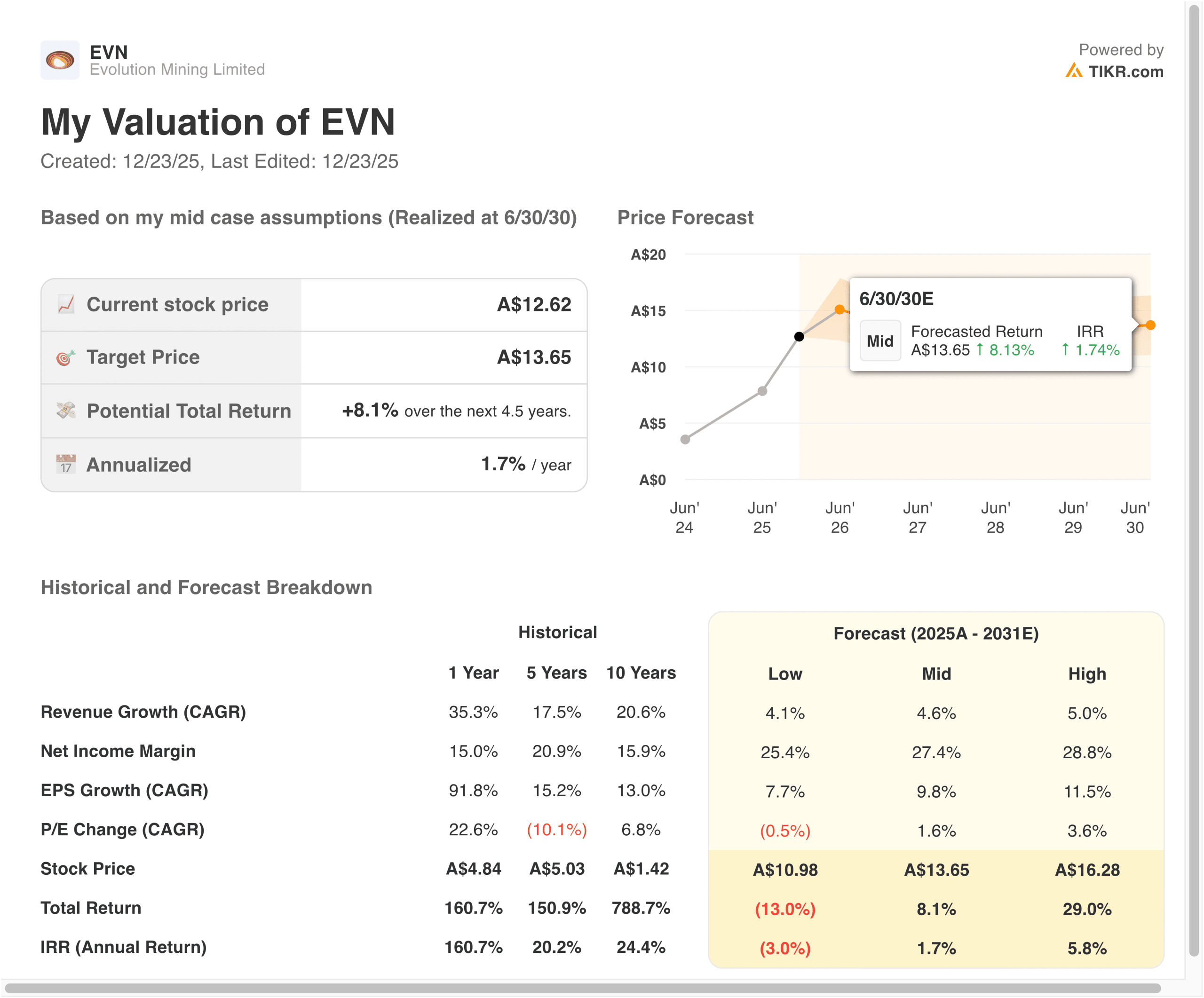

How Much Upside Does Evolution Mining Holdings Stock Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

Find out what your favorite stocks are really worth (Free with TIKR) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!