Harvey Norman Holdings (HVN) Limited is one of Australia’s most recognizable retail brands, operating across consumer electronics, furniture, bedding, and home appliances. What makes Harvey Norman different from most retailers is its hybrid model. The company combines a large franchised retail network with company-owned international stores and a substantial portfolio of owned commercial real estate. This structure allows Harvey Norman to generate revenue not only from retail sales but also from franchise fees, rent, and property appreciation.

Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

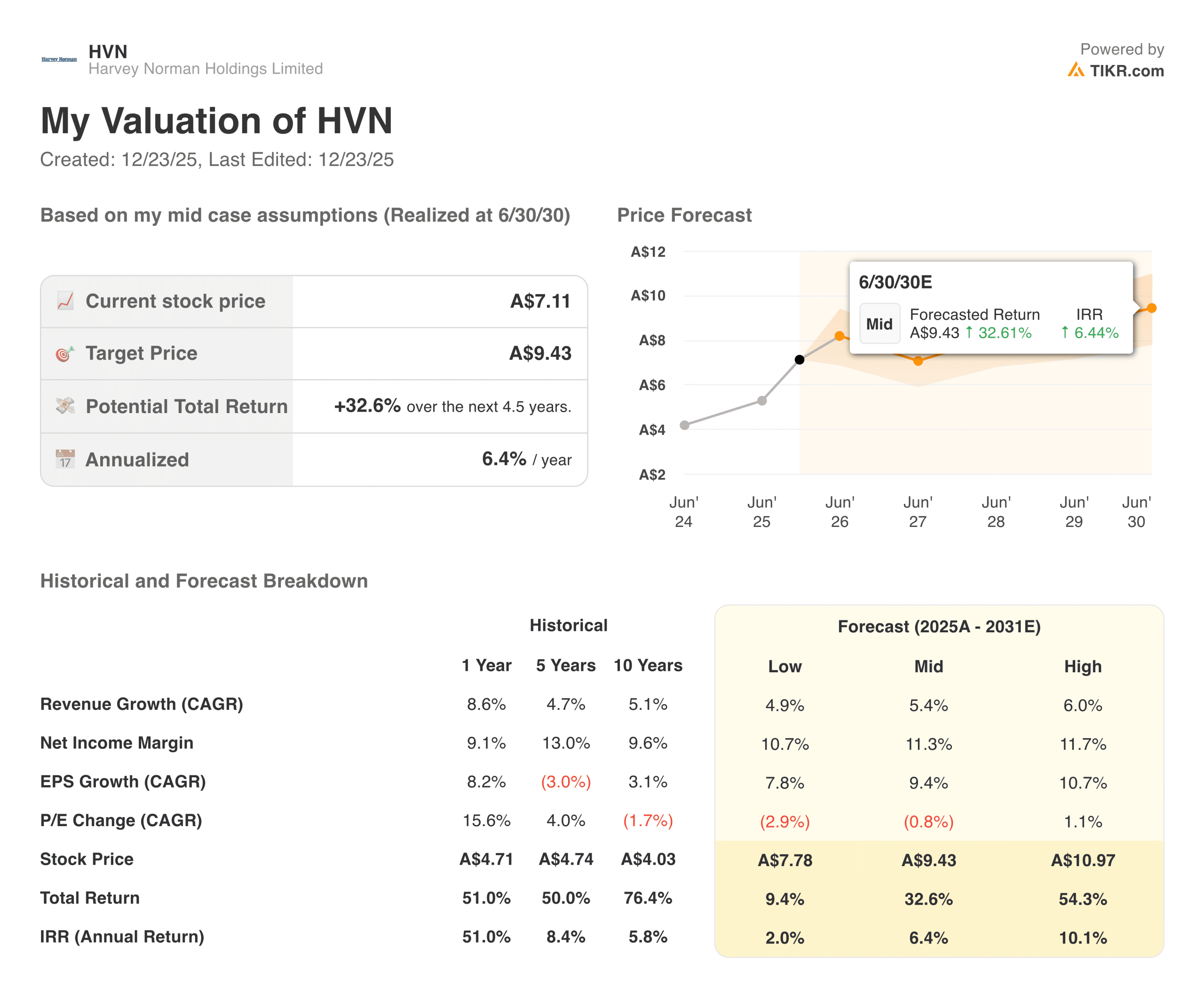

The stock has had a strong run over the past year, rising just over 50 percent as investor sentiment improved. After a difficult post-pandemic reset that weighed on discretionary retailers, Harvey Norman has benefited from stabilizing consumer demand and improving housing-related activity. The recent share price strength reflects renewed confidence that the company can navigate cyclical retail swings while continuing to generate cash from its property and franchising operations.

Heading into the new fiscal year, Harvey Norman’s setup is relatively straightforward. The business is no longer being priced for aggressive growth, but it is also not being treated as a structurally declining retailer. Instead, the market appears to be valuing it as a steady cash generator with optional upside if consumer demand continues to normalize and international operations improve. Valuation expectations remain modest, placing execution, rather than optimism, at the center of the investment case.

Quickly value any stock with TIKR’s powerful new Valuation Model (It’s free!) >>>

Financial Story

FY 2025 was a solid year for Harvey Norman from a financial standpoint. Total system sales reached approximately A$9.35 billion, while consolidated revenue rose to about A$4.47 billion, representing year-over-year growth of roughly 8.6 percent. That growth was supported by stronger franchisee sales, improved trading conditions in Australia, and steady contributions from overseas operations.

| Metric | FY 2025 |

|---|---|

| Total System Sales | A$9.35B |

| Consolidated Revenue | A$4.47B |

| EBITDA | A$1.13B |

| Net Income | A$518.0M |

| Operating Cash Flow | A$694.3M |

| EPS | 41.6 cents |

| Net Debt to Equity | 13.4% |

| Dividend Per Share | 26.5 cents |

Profitability also moved meaningfully higher. EBITDA came in at approximately A$1.13 billion, reflecting improved operating leverage and disciplined cost control. Profit after tax reached A$518 million, up sharply from the prior year as retail margins recovered and property income remained stable. Earnings per share increased to 41.6 cents, supporting a fully franked dividend of 26.5 cents for the year.

Cash flow remained one of the most important parts of the story. Operating cash flow totaled about A$694 million, with cash conversion near 95 percent. Net debt remained conservative, with net debt-to-equity at roughly 13 percent. This balance sheet strength continues to give Harvey Norman flexibility to invest in stores, maintain dividends, and absorb periods of weaker consumer demand without financial strain.

Look up Harvey Norman Holding’s full financial results & estimates (It’s free)>>>

Broader Market Context

The broader retail environment has become more supportive compared to the past two years. Inflation has moderated, interest rates appear closer to their peak, and housing activity is showing early signs of stabilization. These trends matter for Harvey Norman, as big-ticket purchases like furniture and appliances tend to track housing turnover and renovation cycles rather than everyday consumption.

That said, competition remains intense. Online retailers continue to pressure pricing, while global brands are investing more heavily in direct-to-consumer channels. Harvey Norman’s advantage is that it is not solely dependent on retail margins. Its franchising income and property portfolio help smooth earnings and reduce reliance on short-term consumer spending trends.

1. The Franchise and Property Flywheel

The Australian franchising business remains the backbone of Harvey Norman. Aggregated franchisee sales increased by just over 6 percent in FY 2025, while franchising segment profit before tax rose meaningfully faster. Because franchisees bear most store-level costs, incremental sales tend to flow through efficiently to the parent company as fees and rent.

The property portfolio reinforces this flywheel. Harvey Norman owns a large portion of the large-format retail sites its franchisees operate from. As a result, the company benefits from stable rental income and long-term appreciation in property values. This dual exposure to retail and real estate provides earnings stability that is uncommon in discretionary retail.

2. International Operations and Execution Risk

International retail operations remain a mixed but improving part of the story. Markets such as Ireland and Malaysia delivered solid sales growth, while the UK and some European regions remain in investment mode. Losses in early-stage markets weighed on near-term profits, but management has emphasized measured expansion rather than aggressive store rollouts.

Over time, international exposure provides diversification benefits. Consumer cycles do not always move in sync across regions, and overseas growth gives Harvey Norman optional upside beyond Australia. Execution will be key here, as profitability rather than footprint expansion will ultimately determine whether international operations create shareholder value.

Value stocks like Harvey Norman Holdings in less than 60 seconds with TIKR (It’s free) >>>

3. Capital Discipline and Shareholder Returns

Capital discipline continues to define Harvey Norman’s strategy. The company has historically avoided excessive leverage and remains conservative in its approach to acquisitions and expansion. That mindset limited upside during boom periods but has consistently protected the balance sheet during downturns.

In FY 2025, strong cash flow supported dividends, store investments, and balance sheet strength. Net assets increased to approximately A$4.84 billion, and gearing remained low. For long-term investors, this approach prioritizes durability and income over rapid growth, which aligns well with the company’s brand and operating model.

The TIKR Takeaway

Harvey Norman is best understood as a hybrid between a retailer, a franchisor, and a property owner. That combination creates a business with steady cash generation, downside protection, and modest upside tied to consumer recovery and housing trends. At the same time, it is unlikely to deliver high-growth returns, its structure and balance sheet position it as a durable compounder in a sector known for volatility.

Should You Buy, Sell, or Hold Harvey Norman Holdings Stock in 2025?

Investors will likely focus on franchisee sales trends, international profitability, and ongoing cash flow strength. The pace of housing recovery and consumer confidence will shape near-term results, while long-term returns will depend on management’s continued discipline around capital allocation and property ownership.

How Much Upside Does Harvey Norman Holdings Stock Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!