Domino’s Pizza Enterprises Limited (DMP) operates one of the largest master franchise pizza networks in the world, spanning Australia, New Zealand, Europe, and parts of Asia. The company does not run a simple restaurant model. Instead, it earns revenue through a mix of franchise fees, supply chain operations, and digital ordering infrastructure that supports thousands of stores. That asset-light structure is designed to scale efficiently when store economics are healthy, and franchisee confidence is high.

Find out what a stock’s really worth in under 60 seconds with TIKR’s new Valuation Model (It’s free)>>>

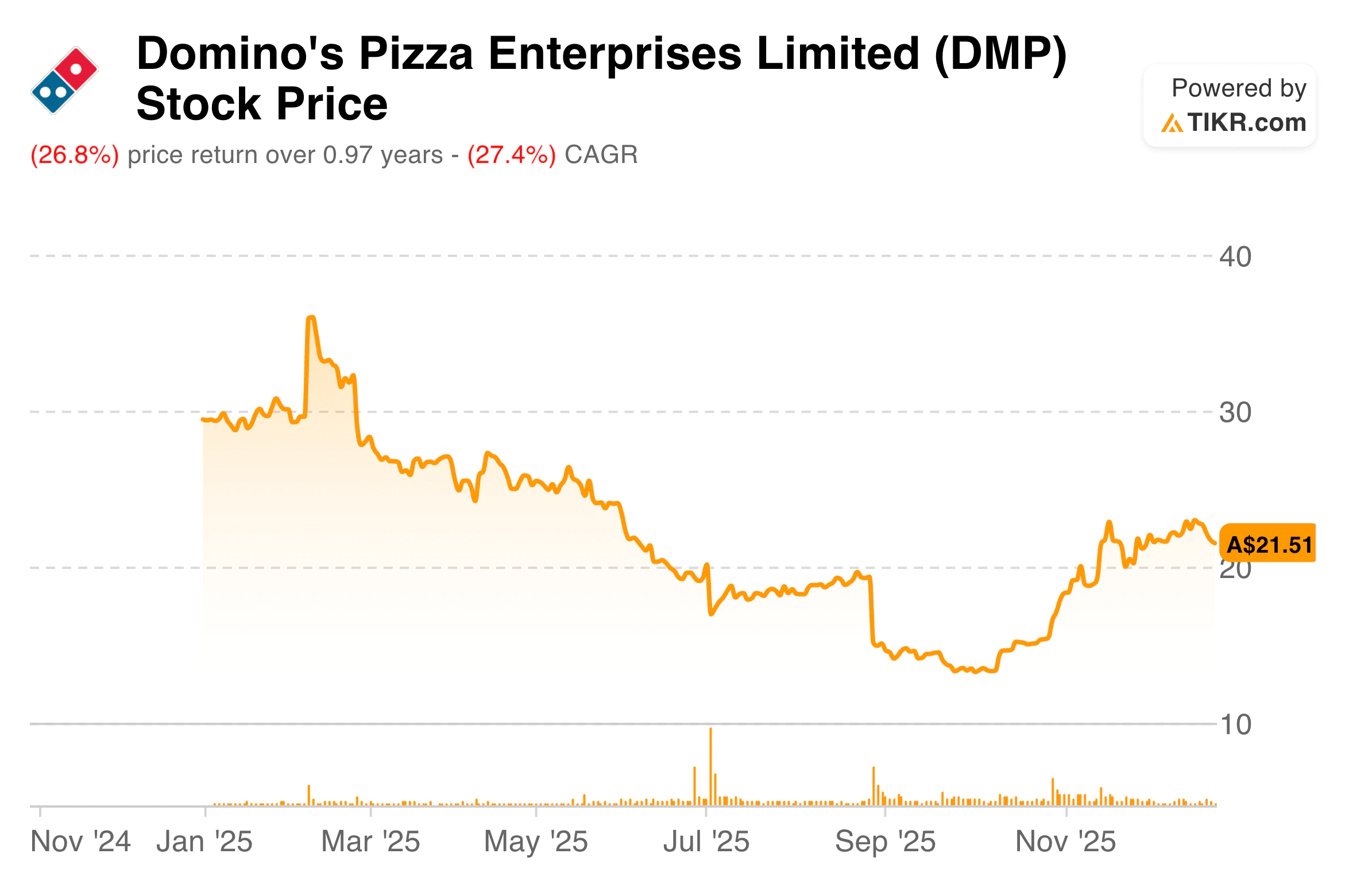

The stock has had a rough stretch over the past year, falling sharply as investors reassessed growth assumptions and execution risk. Concerns about store closures, rising costs, and uneven regional performance weighed heavily on sentiment. Japan and France, in particular, became focal points as profitability lagged and deeper operational resets were required. The result was a meaningful reset in valuation expectations and investor confidence.

Heading into the new fiscal year, the setup looks more balanced. Management has completed a broad strategic review, simplified operations, and taken visible steps to stabilize franchise economics. The narrative is shifting away from aggressive expansion and toward disciplined execution, margin repair, and cash generation. That transition matters because Domino’s valuation now reflects far lower expectations than it did during the growth-at-all-costs phase.

Quickly value any stock with TIKR’s powerful new Valuation Model (It’s free!) >>>

Financial Story

For FY25, Domino’s reported network sales of approximately A$4.15 billion, with revenue of A$3.23 billion. Underlying EBIT came in at A$198.1 million, down modestly year over year as higher global overheads and weaker Asian performance offset strength in ANZ and parts of Europe. Underlying net profit after tax totaled A$116.9 million, excluding A$162.3 million in non-recurring restructuring and store optimization costs.

Margins are an important part of the story, and underlying EBIT declined by about 4.6 percent year over year, while statutory results were heavily distorted by one-time charges associated with store closures and operational streamlining. Free cash flow was A$47.4 million on a reported basis, but adjusted free cash flow, excluding non-recurring cash costs, was A$105.5 million. That distinction is critical to understanding the company’s future earnings power.

From a balance sheet perspective, Domino’s ended FY25 with net debt of roughly A$724.8 million and net leverage of 2.57x EBITDA. While leverage remains above management’s long-term target, interest coverage improved meaningfully, and organic net debt fell by A$51 million before foreign exchange impacts. Capital allocation has clearly shifted toward deleveraging and operational reinvestment rather than rapid store growth.

Look up Domino’s Pizza Enterprises full financial results & estimates (It’s free)>>>

Broader Market Context

Globally, the quick-service restaurant sector remains resilient, but consumer behavior has changed. Value sensitivity is higher, discount-led traffic has become less reliable, and operators are under pressure to simplify menus and pricing. At the same time, delivery economics and aggregator platforms have forced restaurants to rethink promotions and margin structures.

For Domino’s Pizza Enterprises, those trends reinforce the importance of pricing discipline, digital efficiency, and franchisee profitability. Markets that execute well on everyday value rather than heavy discounting are showing better same-store sales momentum. Lagging regions are now receiving more tailored, locally driven strategies rather than one-size-fits-all global playbooks.

1. Franchise Economics and Store Network Reset

A central theme in Domino’s turnaround is restoring franchisee economics. Management has acknowledged that post-COVID cost structures have eroded unit profitability in several markets, particularly in Japan. In response, the company closed more than 300 loss-making stores during FY25, including 233 in Japan. While painful in the short term, those actions are intended to reset the earnings base and remove structurally unprofitable locations.

Franchise partner EBITDA remained broadly stable year over year, and in ANZ, franchisee profitability reached its strongest level in three years. That improvement came from menu simplification, operational discipline, and better pricing execution. The goal is not rapid growth in store count, but sustainable unit economics that can support gradual expansion as conditions improve.

2. Digital Investment and Cost Discipline

Domino’s Pizza Enterprises continues to invest heavily in digital infrastructure, spending A$44.8 million on digital capex in FY25. These investments focus on the stability of online ordering, pricing algorithms, and customer experience improvements. Management has indicated that digital spending should moderate in FY26 as major transformation projects near completion.

At the same time, the company has targeted permanent SG&A reductions rather than short-term cost cuts. Shared services optimization, procurement discipline, and simpler operations are expected to reduce the fixed-cost base over time. Importantly, some of those savings are being redirected toward working media and customer acquisition, which management views as higher-return uses of capital.

Value stocks like Domino’s Pizza Enterprises in less than 60 seconds with TIKR (It’s free) >>>

3. Regional Execution and Management Changes

Regional performance remains uneven, but trends are becoming clearer. ANZ and BENELUX continue to deliver steady EBIT growth, supported by strong in-store execution and marketing efficiency. Germany is showing improving momentum as value-focused campaigns gain traction. France and Japan remain turnaround stories, but leadership changes and localized strategies are now in place.

New management appointments across several regions reflect a shift toward local accountability. Rather than centralized global control, Domino’s is empowering in-country teams to make faster decisions tied to customer behavior. The company believes this structure will improve responsiveness and execution quality, even if financial results do not fully reflect those changes for some time.

The TIKR Takeaway

Domino’s Pizza Enterprises is no longer priced as a high-growth franchising machine. The valuation now reflects execution risk, regional complexity, and a slower growth outlook. For investors, the key question is whether simplified operations, stronger franchise economics, and disciplined capital allocation can stabilize earnings and restore confidence over time.

Should You Buy, Sell, or Hold Domino’s Pizza Enterprises Stock in 2025?

Looking ahead, investors are likely to focus on same-store sales trends, free cash flow conversion, and progress in Japan and France. Improving the balance sheet and franchisee profitability will matter more than headline revenue growth. The next phase for Domino’s is about consistency and credibility rather than expansion, and the stock’s performance will likely follow evidence that those foundations are firmly in place.

How Much Upside Does Domino’s Pizza Enterprises Stock Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

Find out what your favorite stocks are really worth (Free with TIKR) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!